One of the biggest drags on the economy at every scale is unemployment among real estate agents, mortgage brokers, appraisers, home builders, engineers, architects, and a number of related fields.

Irvine Home Address … 6 BUTTERFLY Irvine, CA 92604

Resale Home Price …… $470,000

I'm tellin' you it's got to be the end,

Don't bring me down,no no no no no,

I'll tell you once more before I get off the floor

Don't bring me down.

Electric Light Orchestra — Don't Bring Me Down

Our current economic woes were caused by the real estate sector. Lenders emboldened by sophisticated risk-shifting and securitization pumped trillions of dollars into real estate loans — loans that ultimately went bad because incomes were not sufficient to support them.

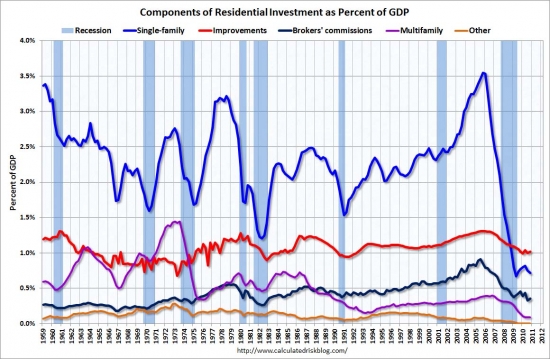

The resulting collapse in real estate prices has caused residential investment to fall to record lows.

That plunging blue line is just another statistical measure. The human toll in suffering among everyone involved in the real estate industrial complex can't be captured by a graph.

Mortgage industry workforce plunges by more than 50% in five years

April 11, 2011 — E. Scott Reckard, Los Angeles Times

Here are some hard numbers for the downturn in mortgage employment I wrote about last week — and they show a reduction of more than 50% in home-lending jobs since the peak of the housing and commercial real estate bubble.

The news peg for the story was mortgage goliath Wells Fargo & Co. saying it had eliminated 1,900 home-lending jobs, mostly workers hired temporarily to deal with last year's mini-boom in refinancings.

But that's nothing compared with the industry's overall decline from more than 500,000 employees in late 2005 and early 2006 to 248,000 in February, according to Bureau of Labor Statistics data compiled by the Mortgage Bankers Assn.

The latest numbers are the lowest for the industry since August 1997, according to the mortgage bankers group. The data, which arrived too late to be included in last week's story, showed that employment peaked at 505,000 in February 2006.

The numbers probably overstate mortgage employment slightly, because the trade group combined the BLS categories “real estate credit” and “mortgage and nonmortgage loan brokers.” But the lion's share of the jobs are related to mortgages and the downturn is dramatic.

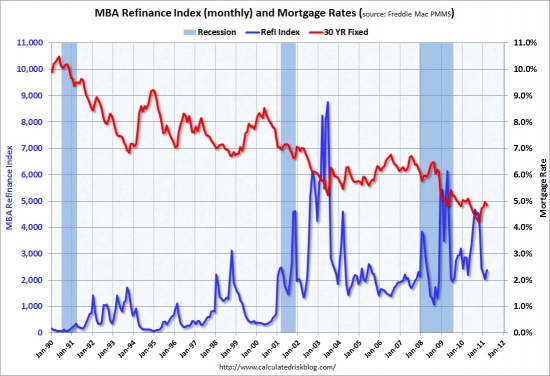

Following up on the story, Calculated Risk posted an interesting chart showing the correlation between 30-year fixed mortgage rates and refinancings. One notable detail is how round numbers catch the attention of homeowners. Check out the giant spike in refis when the rate dipped below 6% in 2003 and the also pronounced but smaller spike when it fell below 5% in 2009.

Mortgage employment also may have been affected by new licensing requirements for employees of nonbank lenders, adopted as part of regulations cleaning up the mess from the financial crisis. The licensing has made it more expensive for these independent brokers and mortgage bankers to maintain their payrolls, people in the industry say.

Chicago Bancorp, a large mortgage-banking firm, completed its purchase of Generations Bank, a Kansas City, Kan., savings and loan, last week to gain access to a nationwide lending market without the added licensing costs, Chicago Bancorp founder Stephen Calk told the Kansas City Star.

A spark from the outside

The economy will not fully recover until the real estate sector is put back to work. No, it doesn't have to attain the unsustainable heights of the housing bubble. A return to historic norms will feel like a boom compared to the last 4 years.

Real estate employment is an economic amplifier. Once people go back to work, new households begin to form, and demand for housing picks up, then and only then will residential investment pick up. Once residential investment improves, people working in real estate will add to demand for its own product, and the economy will gain a synergy from the real estate sector going back to work.

Unfortunately, it will require an outside economic stimulus to begin the chain reaction. In 2009, the federal reserve tried to prop up the housing market in hopes it would stimulate the economy and put the real estate sector back to work. Unfortunately, the policy was unsuccessful because the underlying problems with toxic mortgages was simply too big to be papered over by our central bank.

Until some other sector of the economy grows enough to put people back to work, the household formation necessary to stimulate real estate demand isn't going to happen. In the meantime, most of the real estate sector is unemployed, and the entire economy suffers along with it.

Severe HELOC abuse or mortgage fraud?

The owner of today's featured property weren't content to merely strip every penny from the walls the moment it appeared, she managed to process concurrent refinances at two different banks at the top of the real estate bubble. The timing certainly looks like mortgage fraud.

- Today's featured property was purchased on 3/30/1999 for $235,000. The owner used a $187,920 first mortgage and a $47,080 down payment. She waited four years before going Ponzi.

- On 3/18/2003 she refinanced with a $180,700 first mortgage and a $100,000 HELOC. At this point, she had been paying off his mortgage for four years, but the $100,000 HELOC was too tempting to resist.

- On 7/29/2003 she refinanced with a $273,000 first mortgage and a $78,000 stand-alone second.

- On 5/24/2004 she obtained a $154,000 HELOC.

-

On 8/18/2005 she obtained a $238,000 HELOC.

This is where the mortgage activity looks like mortgage fraud. Ordinarily, people only process one loan at a time because each lender will want to be in first position. Lenders check the property records before funding a loan, but if a borrower can time the funding at both banks to happen within a few days of one another, the recording of the first loan will not show up before the second one funds. The lender on the second loan believes they are in first position because the other loan, the one that funded a few days earlier, has not shown up in the property records. It's only after a week or two that the lender who funded the second loan realizes they were ripped off.

- On 2/23/2006 they refinanced their first mortgage with Bank of America for $540,000. They recorded first, so they are in first position.

- On 2/28/2006 they obtained two loans from Hanmi Bank. The first was a $270,000 mortgage, and the second was a $129,000 mortgage. Hanmi Bank recorded second, so they are totally screwed.

- Between the three loans recorded within days of one another, the total property debt is $939,000.

- Total mortgage equity withdrawal is $751,080.

There is no telling when she quit paying, but one of the lenders finally recorded a NOD in March.

Foreclosure Record

Recording Date: 03/23/2011

Document Type: Notice of Default

With over $900,000 in debt and a recovery closer to $450,000, someone is going to lose a lot of money. Hamni Bank will have to go after this deadbeat for theft via mortgage fraud. I doubt they have any assets for the bank to recover.

Irvine House Address … 6 BUTTERFLY Irvine, CA 92604 ![]()

Resale House Price …… $470,000

House Purchase Price … $235,000

House Purchase Date …. 3/30/1999

Net Gain (Loss) ………. $206,800

Percent Change ………. 88.0%

Annual Appreciation … 5.7%

Cost of House Ownership

————————————————-

$470,000 ………. Asking Price

$16,450 ………. 3.5% Down FHA Financing

4.87% …………… Mortgage Interest Rate

$453,550 ………. 30-Year Mortgage

$102,808 ………. Income Requirement

$2,399 ………. Monthly Mortgage Payment

$407 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$98 ………. Homeowners Insurance (@ 0.25%)

$522 ………. Private Mortgage Insurance

$215 ………. Homeowners Association Fees

============================================.jpg)

$3,641 ………. Monthly Cash Outlays

-$393 ………. Tax Savings (% of Interest and Property Tax)

-$558 ………. Equity Hidden in Payment (Amortization)

$31 ………. Lost Income to Down Payment (net of taxes)

$79 ………. Maintenance and Replacement Reserves

============================================

$2,799 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$4,700 ………. Furnishing and Move In @1%

$4,700 ………. Closing Costs @1%

$4,536 ………… Interest Points @1% of Loan

$16,450 ………. Down Payment

============================================

$30,386 ………. Total Cash Costs

$42,900 ………… Emergency Cash Reserves

============================================

$73,286 ………. Total Savings Needed

Property Details for 6 BUTTERFLY Irvine, CA 92604

——————————————————————————.png)

Beds: 3

Baths: 2

Sq. Ft.: 1950

$241/SF

Property Type: Residential, Single Family

Style: Two Level, Other

Year Built: 1977

Community: 0

County: Orange

MLS#: P776205

Source: SoCalMLS

Status: Active

On Redfin: 9 days

——————————————————————————

Beautiful hard wood floor with high ceiling, Granite counter top and Newer cabinet in Kitchen. Morrored Wardrobes, Custom added storage area in Master bedroom closet. Large lush backyard Backing to Greenbelt, Spacious and airy floorplan. Great location for shopping, park, and schools.

Are people wising up to the renter's subsidy? When real estate prices aren't rising, it's much cheaper to rent high-end real estate than it is to own it. Wise rich people will chose to rent and let someone else be an owner who is subsidising their housing, particularly when prices are falling.

Are people wising up to the renter's subsidy? When real estate prices aren't rising, it's much cheaper to rent high-end real estate than it is to own it. Wise rich people will chose to rent and let someone else be an owner who is subsidising their housing, particularly when prices are falling. We are seeing where the housing market really is. Sales are weak and prices are down. The market is falling again because a natural bottom was not allowed to form the first time. We delayed the bottom two years, perhaps raised the bottom 15% to 20% locally, but we prolonged our agony to adjust to the reality of the housing crash.

We are seeing where the housing market really is. Sales are weak and prices are down. The market is falling again because a natural bottom was not allowed to form the first time. We delayed the bottom two years, perhaps raised the bottom 15% to 20% locally, but we prolonged our agony to adjust to the reality of the housing crash.

.png)

Did the lender really obtain a greater recovery at short sale? If they had foreclosed in a timely manner months ago when the borrower first went delinquent, prices were higher, and the recovery would have been greater. Plus, the real estate commissions and other sales costs not paid at auction eat into recovery amounts. Further when you factor in the portfolio cost of lowering neighborhood values, and short sales aren't the magic elixir they are made out to be.

Did the lender really obtain a greater recovery at short sale? If they had foreclosed in a timely manner months ago when the borrower first went delinquent, prices were higher, and the recovery would have been greater. Plus, the real estate commissions and other sales costs not paid at auction eat into recovery amounts. Further when you factor in the portfolio cost of lowering neighborhood values, and short sales aren't the magic elixir they are made out to be.

.png)