You pinch yourself but the mem'ries are all you feel

Can you break away from your alibis

Can you make a play will you meet me in the dark…

Billy Squire — in The Dark

The NAr and lenders both want to convince potential buyers no problem exists with shadow inventory. They want to keep both this inventory and buyers in the dark.

by CHRISTINE RICCIARDI — Monday, March 21st, 2011, 5:08 pm

Foreclosure time lines and an abundance of distressed home sales are causing wide fluctuations in shadow inventory across the country.

The National Association of Realtors released state-by-state data on shadow inventory Monday, calculating the data in relation to distressed property sales. On the whole, Capital Economics estimates there are 5.3 million homes in limbo between foreclosure and the sales market. Standard & Poor's states it could take up to 49 months to clear the shadow inventory books. However, the NAR numbers indicate which states are in better shape to unload these properties based on the respective proportion of distressed sales.

Florida holds the largest shadow inventory across the U.S., with more than 441,000 residential properties caught between foreclosure and the sales market, according to NAR. California is a far second with almost 228,000 residential properties constituting the shadow inventory. Shadow inventory properties are sold as distressed sales.

NAR attributed growing shadow inventories to the ramifications of recent disruptions to foreclosure time lines. Some states are having more trouble than others in moving these properties into foreclosure. For example, a mortgage in Florida is delinquent 638 days on average, the second longest time line in the country. The only state that tops that is New York where the average loan is delinquent 644 days before its cleared through the foreclosure process. New York currently holds the fourth largest shadow inventory of 107,500, according to NAR.

NAR reported that the length of the foreclosure process in Florida and California jumped 156% and 157%, respectively, since 2008.

Still, two states commonly seen as poster children for the foreclosure and housing crisis are faring much better in terms of clearing out shadow inventory. Nevada and Arizona both rank in the top 26 states with the largest shadow inventory. However, among those 26 states, they rank 11th (Arizona) and 16th (Nevada) for their level of shadow inventory, behind many states that are supposed to be in recovery, including Texas.

I am not surprised Nevada is not in the top 10 for shadow inventory. Lenders are processing foreclosures there. Wherever they decided to allow people to squat — like California — shadow inventory dominates the landscape.

“This is largely due to their shadow inventory moving somewhat faster through the pipelines and comprising larger share of existing sales,” NAR said. Distressed sales comprised 69% of existing home sales in Nevada in the fourth quarter of 2010 and 55% in Arizona. (Full national stats available by clicking chart below.)

NAR reported early Monday that distressed sales nationwide increased to 39% of all existing purchase transactions in February. The median sale price is hurt by this type of sale, as well as the number of cash transactions that took during the month. The median sale fell 5.2% compared to one year ago to $156,000, NAR said.

Notice the NAr buries that little tidbit at the end of their press release. Perhaps they figured people wouldn't notice prices are falling again.

NAR determined it will take 29 months to clear shadow inventory in Florida, 11 months to clear in California, 34 months to clear in New York, seven months to clear in Nevada and nine months to clear in Arizona.

In Wyoming, the state with the smallest shadow inventory, it will take 13 months to clear the 1,837 homes in limbo. Nevada ties Mississippi for the shortest time frame to clear the shadow inventory at seven months. New Jersey has the longest time line at 51 months, according to NAR.

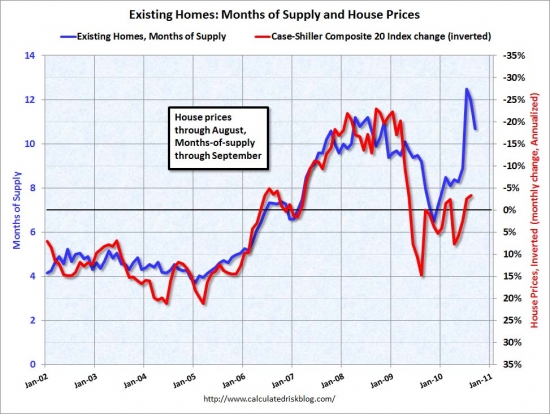

When the NAr calculates the months of inventory, they divide total inventory by the monthly sales rate to compute the number of months it would take to clear the existing inventory if no new properties were added. They use the same methodology to measure the months of inventory of shadow inventory. This measure is supposed to say something about how long the shadow inventory problem will be with us, but in typical NAr style, they rely on this measure to downplay the real seriousness of the problem.

In the real world, there are only so many buyers, and even if lenders put every distressed property on the market at once, prices could not be lowered enough to absorb that much supply. Lenders must slowly release this inventory or prices crash. Further, in the real world, when the composition of sales is more than 40% distressed properties, prices also fall. Therefore, lenders must manage the flow of properties to be no more than 40% of sales to keep prices stable.

When the total market inventory is around six months, lenders cannot add to total inventory without prices going down. The distressed properties become an additional 40% which pushes months of inventory to double digits where it is now. It has remained elevated for the last four years.

Realistically, shadow inventory can only be liquidated at 40% of the monthly sales rate. If you take the NAr estimate of 11 months of shadow inventory in California — which is a joke — and divide it by 40%, and the months of inventory balloons to 27.5.

The NAr measure of shadow inventory months of supply understates reality by 150%. The Standard and Poor's estimate of 49 months nationally is far more realistic. Four years from now, we will begin liquidating the long tail of distress that will follow this crisis into the later half of this decade.

Bankers allow each other to squat

One of the most infuriating facts about shadow inventory is its epicenter: the New York MSA. Boneheads in New York think their market is immune as it is one of the few where properties still routinely trade at peak prices. Little do they know that this price stability is an illusion created by shadow inventory.

by JACOB GAFFNEY — Wednesday, February 2nd, 2011, 3:57 pm

“The shadow inventory in the New York MSA will take the longest to clear — 130 months as of fourth-quarter 2010. That is at least twice as long as it will take in any of the other top 20 MSAs and 2.7 times the average time to clear for the U.S. as a whole,” the S&P report states. “This is primarily due to very low liquidation rates in New York.”

What the hell is this? Very low liquidation rates? Why is that? Could it be that bankers don't want to hurt their own property values? What other reason could there be? Assholes.

The previous Ponzis

Many Ponzis from the housing bubble left their cash cows to the bagholder to pay off. The previous owners of this property got the better end of the deal.

The bought the property on 4/16/1999 for 265,500. The used a $212,200 first mortgage and a $53,300 down payment.

On 3/21/2001 they obtained a stand-alone second for $100,000. I hope they didn't spend it all in one place.

On 3/20/2002 they went in for their annual cash infusion. The refinanced the first mortgage for $285,000 and added a stand-alone second for $57,000.

On 6/3/2003 the refinanced with a $300,000 first mortgage and a $80,000 HELOC.

On 3/19/2004 they refinanced the $300,000 first mortgage.

On 7/29/2004 they refinanced with a $333,700 first mortgage.

On 3/4/2005 they refinanced with a $380,000 first mortgage. Then it gets weird.

On 6/8/2005 they refinanced with a $380,000 first mortgage.

On 7/13/2005 they refinanced with a $380,000 first mortgage.

On 10/20/2005 they refinanced with a $380,000 first mortgage.

On 2/16/2006 they refinanced with a $380,000 first mortgage. I wonder if one of the owners was a mortgage broker churning their own mortgage for fees? I have never seen four refinances for the same amount before.

Total mortgage equity withdrawal was $167,800.

After riding the equity wave for six years, they sell to the current dreamers for $525,000 on 12/18/2007.

The current dreamers

With aggregate prices in Irvine below $330/SF and falling, how do these owners realistically expect to get $397/SF for a corner lot at a busy intersection?

Based on when these people bought — the market dropped more than 10% in 2008 — they will be lucky to get near their asking price.

Perhaps that special buyer will come along who appreciates the unique attributes of this tract home and offers more than its asking price. ~~ giggles ~~

UPGRADED Detached 3 bedrooms and 2.5 bathrooms home that is strategically located close to award-winning Myford Elementary & Pioneer Middle School. Cul-De-Sac location. Designer upgrades include elegant hardwood, tile flooring, custom carpet, and recess lightings. Cozy & warm living/family room with a fireplace. Spacious kitchen features 5-burner cooktop range, stainless steel appliances, oak cabinetry, reverse osmosis, instant hot water and granite countertop. A huge master suite with walk-in closet that is big enough to be a bedroom, dual vanities and a shower in the master bathroom. Powder room with pedestal sink, and convenient upstairs laundry. Hardscaped backyard, great for entertaining families & friends. NEW insulated garage door, NEW faucets, NEW mirrors in the upstairs bathrooms. A/C & heating unit were recently serviced. NO HOA & LOW Mello Roos (approx. $1,500/ yr)

The deflating housing bubble has done little to curb American's enthusiasm for owning real estate. However, the collapse has provided people sound reasons for not buying a house.

The need for shelter is basic as is the desire for community. In the United States, this translates into a desire to take on a very large mortgage to buy real estate. These basic human emotions drive much of the activity in real estate markets.

Most people buy because it is the right time for them. Their career, age, family circumstances all come together to push people toward ownership at different times. Some are fortunate and buy at the bottom of the real estate cycle. Some are not so fortunate and buy at the peak.

The most damaging aspect of our current system is the price volatility. It capriciously rewards some and destroys others. Home price volatility creates a culture of Ponzi borrowing and dependency. The goal of government policy should be price stability, but lately it seems their goal is price maximization.

Seven Reasons We're Buying and Four Reasons We're Not

By Julia Edwards and Edmund L. Andrews

Wednesday, March 23, 2011 — 12:28 p.m.

Although the housing bubble and bust may have shattered notions that home prices have nowhere to go but up, Americans haven’t lost their love for owning a home. In the latest Allstate/National JournalHeartland Monitor poll, homeownership ranked second, just behind raising a family, in people’s definition of the American Dream. Despite new home sales' drop to a record low, about four-fifths of respondents said that owning a home is still a better financial decision than renting, and nearly nine in 10 homeowners say would buy their home again.

Those results also underscore the extent to which Americans see buying a home as a deeply personal decision. It seems the decision to buy a home is made from the heart, while the decision to rent comes from the wallet.

That is a great way to look at the situation. Most people want to buy and own. Those who look rationally at the costs often chose to rent, not because it's the most emotionally pleasing choice, but because it's the most financially sound decision. Those who chose to rent recognize that being house poor is its own form of unhappiness that so takes away from the joy of ownership as to make it undesirable.

We reveal the top seven reasons why Americans are still drawn to owning a home, and the four reasons that make them hesitant to buy, according to the Heartland Monitor poll.

Reason to Buy No. 7: Getting a tax deduction

Only 2 percent said they considered the tax deduction for homeowner’s a reason to buy a home. That number may come as a shock to members of the Obama administration, who designed the first-time homebuyer tax credit, now expired, as an incentive to bring more buyers to market.

That is a surprisingly low number. Nationally, only about a third of home owning taxpayers take the home mortgage interest deduction, but the proportion in Irvine will be much higher. For high wage earners borrowing upwards of a million dollars, the tax deduction is very motivating.

Reason to Buy No. 6: Following in your parents’ footsteps

Following the path of mom and dad tied with a tax deduction among participants. Only 2 percent said they considered it important to own a home because they had grown up in a house.

I suspect this number is so low because people are unaware of their true motivations. So much of our behavior is subconscious, and the familiarity of house and home provides a psychological anchoring to real estate that runs very deep.

Reason to Buy No. 5: Being part of a neighborhood and community

Putting down roots in a community was a reason to buy a home among 6 percent of participants.

This is another area where Irvine is a special subset of buyers. Many people chose master planned communities like Irvine because they want neighborhood involvement. The number may only represent 6% of America, but it is much higher among readers of this blog.

Reason to Buy No. 4: Acquiring an asset you can pass along

The security that used to come with owning a tangible property may have faded, but 9 percent of participants said they still consider it a reason to buy a home.

Our society has become so mobile that people have come to recognize the impermanence of all living arrangements. We no longer buy family homes and stay there through our passing.

Personally, I plan to acquire several investment homes to pass on to my son. I guess I am one of the 9 percent.

Reason to Buy No. 3: Making a good, long-term investment

Although foreclosure rates may tell us otherwise, 13 percent still believed that owning a home is a good, long-term investment.

The question is a bit vague and misleading. All the terms are up for interpretation: What is good? What is long-term? And what is investment? I believe a good long-term investment is an income property with an 8% cap rate in today's market. Some believe a good long-term investment is a speculative flip in the North Korea towers. Over the very long term, real estate values rise in nominal dollars along with inflation. Is that good?

Reason to Buy No. 2: Building equity rather than paying rent

Building equity was the strongest of all financial reasons to own a home. Twenty-six percent of participants said they would own a home to build credit through a mortgage payment rather than earning less credit through paying rent.

The reason people want to own the home is to obtain appreciation. This nonsense about paying down a mortgage is not what people really think. No California Ponzi believes they have to reduce the balance of their mortgage. Mortgages are made to get larger.

realtors like to spin this as “throwing money away on rent.” Of course, they ignore the fact that they are throwing away much more money renting the bank's money, but the tax deduction makes it all okay, right?

Reason to Buy No. 1: Having a place to raise a family

An overwhelming 40 percent said that raising a family in a place of their own was the ultimate factor in their decision to buy. The housing market may rise and fall, but the value of the home to the American family seems set in stone.

People have come to equate ownership with stability. Unfortunately, our concept of ownership has been perverted into money rentership. Ownership with a huge mortgage is tenuous compared to renting. Capricious landlords evicting good tenants are much less common than robo-signing lenders evicting delinquent borrowers.

The timeless and the new

The reasons listed above are timeless. No matter when an article like this is written, the above reasons will be on it, and they will be just as compelling to buyers. The new are the reasons not to buy. These are a direct response to the collapsing housing bubble.

Reason Not to Buy No. 4: Entering into many years of debt

The bursting of the bubble and the horror stories that followed made 13 percent of respondents hesitant to agree to pay the high price of a home.

Five years ago, nobody cared about debt levels.

Reason Not to Buy No. 3: Losing the flexibility to move if you need to find a new job

In our mobile society and fickle job market, 21 percent said they would be hesitant to lock into a place that they may not be able to sell should they have to move to take a job.

Five years ago, everyone assumed you would simply sell your house for a huge profit if you needed to move.

Reason Not to Buy No. 2: Risking you home losing value if real-estate prices drop

“Price Reduced” signs cropping up in the yards of neighbors desperate to sell led 21 percent to back away from buying a home that could sell for less than the price they paid for it.

Five years ago, with exception of a few of us crazy bloggers, very few people believed prices could go down.

Reason Not to Buy No. 1: Monthly mortgage payments are too high

As opposed to the familial emotions that made 40 percent lean toward homeownership, the harsh realities of high monthly mortgage payments was the ultimate reason that 40 percent of participants said they would not buy a home.

The last reason is why house prices still need to come down. Despite the low interest rates, the cost of ownership is still too high in many markets.

What's it like to be immobile?

Today's featured property is an example of reasons number 3 above. People who buy now, or who bought since 2009, are facing the problem of a flat or declining market. When prices don't go up, people have to pay the sales commissions out of their down payment. That was their money rather than the market's. When free money from the appreciation fairies doesn't materialize, owners generally price their properties to accomplish three things:

Provide negotiating room to lower price,

Pay the realtor, and

Get their down payment money back.

Hence, we see properties priced just over breakeven like today's.

I want every buyer looking today and over the next two or three years to be forewarned that they could find themselves in this situation. And reinforcing risk #2 — dropping prices — it could even be worse.

Location, Location! One block from the Lake. .. 4 bedrooms, 2.5 bath single family detached home in premium 'inside the loop' location. Walk to award winning elementary and middle school or perhaps stroll to the lake and enjoy the view or activities at the South Lake Beach Club/Lagoon. Rarely on the market, this spacious Wildflower model has an open floor plan, cathedral ceilings, newer Low E dual paned vinyl windows throughout, newer roof. Separate living room with charming inglenook seating area with own fireplace, large slider window and door invites the entertainer's backyard into the room. Kitchen has updated stainless steel appliances, countertop, tile flooring and recessed lighting – separate family room flows from the kitchen with built in shelving. Bathrooms have updated glass shower doors and lighting fixtures. Closet organizers in all bedroom closets. Great location, great house, come see and make it your home.

We've got a new Exclusive Access Property. It is a 2bd/1.25ba 1,000 square foot condo (single level, first floor entry, 1 car attached garage) in Mission Viejo priced at $249,900. If you are considering purchasing this to rent it out, the seller is interested in leasing the home back for a year. This home is not yet on MLS but will be in 7 days.

If you want to learn more about this property, please contact us:

realtors take advantage of their status as trusted experts to manipulate buyers, and they feel no responsibility when their statements are exposed as lies.

There are some things that never made sense to me. I remember when I first read about prejudice, slavery, and segregation in grade school. I didn't understand how people could treat each other that way. It still doesn't make much sense to me.

Realtors are liars. We all know that, yet we tolerate and even encourage the behavior. Why would anyone want to hear bullshit? Apparently some people do. That doesn't make much sense to me either.

Since Dr. White's paper is so long — and so good — I am reprinting it with some edits for brevity with limited commentary. I am not indenting and italicizing the quoted text to make it easier for you to read. What follows is not my original writing.

Brent T. White The University of Arizona James E. Rogers College of Law

March 2011

Abstract: Real estate agents benefit from the trust associated with portraying themselves as real estate experts, yet are generally not legally responsible for the advice that they give. This lack of legal responsibility is at odds with psychological propensity of individuals to trust perceived experts. It also creates a genuine moral hazard, fueled the housing market bubble and contributed to the suffering of homeowners whose real estate agents encouraged them to buy as the market began to burst. In response to this problem, this article proposes a new regulatory regime requiring real estate agents to choose between two paths: (1) accept legal liability when they negligently, recklessly or intentionally make inaccurate or misleading pronouncements about a home’s value or investment potential; or (2) embrace their role as “salespersons” and refrain from offering advice or opinions about the real estate market to their customers.

TRUST, EXPERT ADVICE, AND REALTOR RESPONSIBILITY

Introduction

As the housing crisis enters its fourth year, national home prices are down over 30%, more than 11 million homeowners are underwater on their mortgages, and over 6.5 million homeowners have already lost or given up their homes to foreclosure. Over 4 million more homes are in the pre-foreclosure process – and most economists predict that the crisis has yet to run its course.

Public discussions over the causes and responsibility for the housing crisis have focused primarily on homeowners, who are said to have bought homes that they could not afford; lenders, who are alleged to have been irresponsible in their lending practices; and the government, which is alternatively accused of meddling too much in the mortgage market or failing to regulate the market when it should have. Largely lost in this discussion has been the role of the real estate brokerage industry in both stoking the housing bubble and then delaying public recognition that the bubble had burst.

Moreover, while homeowners, lenders, and the government – and by extension taxpayers – have all taken significant losses due to the housing meltdown, those in the real estate brokerage industry have borne no financial responsibility for their role in creating the housing bubble and burst. This includes not only the National Association of Realtors (NAR), but also individual real estate agents. Indeed, even real estate agents who knowingly conveyed overly-optimistic forecasts for the housing market and intentionally gave misleading advice to their clients have escaped responsibility for the financial suffering caused by their actions in the wake of the housing collapse.While such real estate agents may be a minority, even the most unscrupulous agents escape responsibility – as courts generally treat real estate agents as mere salespersons, who are simply not responsible for their advice or opinions.

Courts’ treatment of real estate agents as mere salespersons is at odds with most agents’ self-description as professionals who have specialized expertise on the housing market and who owe a fiduciary duty to their clients. Court decisions are also detached from the concrete reality of real estate transactions in which buyers hire and trust real estate agents to guide them through the complex process of purchasing a home. Indeed, literature from the cognitive sciences suggests that, because homebuyers are generally novices making complex decisions on the basis of limited information, real estate transactions are exactly the type of transactions where individuals are most likely to hire and trust a perceived expert.

This discrepancy between homebuyers’ psychological propensity to trust perceived experts and the legal rule that a buyer may not reasonably rely upon his real estate agent’s advice, creates a genuine moral hazard in which real estate agents benefit from the trust associated with portraying themselves as real estate experts, yet avoid responsibility for the advice that they give. This discrepancy is made more problematic by the fact that many buyers are likely unaware that their real estate agents bear no legal responsibility for their advice and opinions, and buyers are thus likely to place undue reliance upon their agents’ recommendations.

In response to this problem, this article suggests two possible paths: (1) fully professionalizing the real estate agent’s role, including regulations subjecting agents to legal liability when they negligently, recklessly or intentionally make inaccurate or misleading pronouncements about a home’s value or investment potential; or (2) de-professionalizing the real estate agent’s role by requiring mandatory disclosures to buyers that real estate agents are “mere salespersons” and barring real estate agents from offering advice or opinions as to a home’s value or investment potential. But – as the housing meltdown has shown – the middle path, in which real estate agents may represent themselves as professional experts but are treated as mere salespersons when it comes to legal liability, is both untenable and unfair.

The Rhetoric of Homeowner Responsibility

Looking back to 2005 and 2006, when the United States was in the throes of the housing bubble, it seems remarkable – if not downright foolish – that so many people in overpriced markets were willing to pay hundreds of thousands more for average-sized homes than those same homes would have sold for just a few years before. Moreover, in order to do so, these home buyers were willing to take on mortgage payments that frequently required all of their disposable income and were two to three times more than they would have paid to rent a similar home. Now that home prices have come crashing down, many of these homeowners find themselves throwing all of their disposable income into homes worth much less than they owe.

Any sympathy for these homeowners aside, they made the decision to purchase their homes. Thus, the common view holds, they must bear the consequences of their actions. They should have known that paying three times more for a mortgage than they could have paid to rent the same house was simply unwise. They should have foreseen that hugely inflated home prices might decline. And they shouldn’t have been so careless in taking on the burden of a mortgage payment that required all or most of their disposable income. If they now find themselves in a terrible predicament, it’s one of their own making. They signed their mortgage knowing full well that they were taking on a huge financial responsibility – and, if they now regret that decision, they have no one to blame but themselves.

This argument has great emotional appeal, as it ties into the American ethos of personal responsibility and the angst in some quarters that Americans are increasing losing sight of this value. This American ethos holds that ultimate decision-making responsibility lies with self. Messages of personal responsibility are big winners when it comes to the public dialogue related to underwater homeowners.

Indeed, many underwater homeowners themselves believe that they should accept responsibility for their mistake in buying at the wrong time. They blame themselves for being foolish – for not seeing this coming. If they hadn’t been in such a rush to buy a home, if they had listened to that voice inside themselves telling them that housing prices seemed crazy, if they had done some more research about the state of the housing market before making such a big decision, if they had bought a more modest home and not put all their eggs in the homeownership basket, and – better yet – if they had just rented instead, they wouldn’t find themselves in this mess.

The “Buyers Agent”

Such self-recrimination aside, it’s not typically the case that homebuyers make their decisions in isolation. While the ultimate decision may be their call, potential homebuyers are subject to a variety of outside influences including family, friends, and – critically – real estate agents (aka, “realtors”). Indeed, over 79% of homebuyers work with an agent in purchasing a home. As self- described experts on the housing market, buyer’s agents serve a variety of functions including assisting buyers in finding a suitable property, preparing an offer, and negotiating with the seller. Agents also typically advise the buyer as to an appropriate price, and whether the property is a good investment.

… Buyers may worry, for example, about whether they are purchasing at the right time or making a good financial decision by investing in real estate. This was particularly likely to be the case when housing prices reached the stratosphere during the boom and a reasonable person might have questioned whether it really made sense to buy at those prices. Anxieties are also likely to be pronounced now in a declining market, when a buyer might reasonably worry that the market still has a ways to go to hit bottom. Buyers in both situations will typically turn to their real estate agents for advice and reassurance. Real estate agents not infrequently respond – both in booming and declining markets – by assuring their clients that it is a “great time to buy,” and that buying a home is a wise and safe investment. Real estate agents will also typically offer some rationale why this is the case.

Because most buyers lack the perceived knowledge or experience of their real estate agents, buyers frequently trust their agents’ opinions and representations on such matters. Indeed, the buyer has probably engaged the agent for their expertise. Many successful agents work hard to further cultivate this trust throughout the relationship, including the sense that the agent is not simply “a salesperson,” but rather “a reliable adviser who cares more about the customer than the transaction.” If the agent succeeds in engendering this trust, it can pay “back in spades” at decision time, when the buyer is called to trust the agent as the “expert.”

But while homebuyers are called to trust real estate agents as experts, real estate agents also sell houses for a living. This dual role as advisor and salesperson creates an inevitable conflict of interest for real estate agents. For example, if a real estate agent had told her clients in 2005 and early 2006 that some of the country’s most prominent economists believed that housing prices were unsustainable or, in late 2006, that these same economists were arguing that home prices were headed for significant declines, her clients might have decided not to buy. If too many of her clients made this decision, the realtor could not have earned a living. It’s not good business to tell prospective homebuyers that the housing market may crash.

While highly-conscientious real estate agents might have nevertheless issued such warnings, many undoubtedly did not. Such agents were not necessarily acting nefariously, as many agents may have truly thought that residential real estate was a great investment. Like most homebuyers, many real estate agents didn’t see the crash coming. One doesn’t have to look far to find real estate agents who lost their own shirts in the housing collapse. Many real estate agents, however, must have at least heard the warnings that the real estate market was headed for trouble – and, if they didn’t, they weren’t paying attention.

NAR Spin

While an average person, caught up in their own lives and deluged by information in the internet age, might not have been aware of this debate, a real estate expert should have been – at least in order to be worthy of the expert label. Indeed, these warnings so alarmed those in the real estate brokerage industry that the New York Times reported that in August of 2005 that Robert Shiller had already “become the bugaboo of the multibillion-dollar real-estate industry. Its executives, like many Wall Street economists, say that low interest rates and a growing population will keep house prices rising, even if future increases are smaller than recent ones.” In other words, at least some experts in the real estate brokerage industry were well aware of the housing bubble warnings – and actively dismissed them.

The NAR, in particular, tended to discount any concerns about the housing market in 2005, 2006, and even well into 2007. The persistent line of the NAR during the height of the housing bubble was that there was no bubble – and that buyers should jump before prices got even higher. Moreover, as the housing market began to weaken in 2006, the NAR’s chief economist, David Lereah, explained that the market would land on a “high plateau” in 2006, and that the market was just leveling out, “headed for a soft landing.” Lereah argued that home prices had never declined on a national level before, and that worries of a national bubble bursting were absurd:

I’m getting tired of all these doomsayers. We live in houses, and our houses are not going to crash. This isn’t the stock market…. Local economies are relatively healthy. There’s job creation – this isn’t a scenario where bubbles burst. Can there be one or two or three or several local markets where prices actually go down? Yes. But to generalize for 30 markets or the whole real estate marketplace – that’s absurd.

Once prices did start to decline on a national level and continued to do so into 2007, the NAR assured its members and prospective buyers each month – for months on end – that the housing market had hit bottom and prices would soon begin to rise again. As Mr. Lereah would famously declare in March of 2007: “It looks like we've bottomed out. . . . When it's all said and done, this contraction in housing is probably going to be the least severe contraction we've ever had, which is going to surprise a lot of people.” Prices continued to decline for over three years thereafter, declining an additional 23% by July 2010. …

… Given all the indications of trouble in the residential real estate market beginning in late 2005, the NAR has been criticized for repeatedly dismissing concerns of a bubble and for not warning buyers that it might, in fact, not be a good time to buy:

By being such dishonest brokers of information, the NAR has now made themselves look ridiculous. No one knows what the future will bring, but consistently absurd spin offered up by the Realtor group not only does a disservice to the public, but is now working against the interest of Realtors themselves.”

Indeed, after leaving the NAR, Mr. Lereah himself admitted that he had put a “positive spin” on the housing numbers:

I worked for an association promoting housing, and it was my job to represent their interests. If you look at my actual forecasts, the numbers were right in line with most forecasts. The difference was that I put a positive spin on it. It was easy to do during boom times, harder when times weren't good. I never thought the whole national real estate market would burst…. [Looking back] I would not have done anything different. But I was a public spokesman writing about housing having a good future. I was wrong. I have to take responsibility for that.

The Blind Leading the Blind

Mr. Lereah’s admission of having spun the numbers aside, one can understand why many individual real estate agents – most of whom have no training as economists or as investment advisors – might have believed what they were being told by the NAR’s chief economist. As such, an agent might have understandably decided that there was no need to mention to his clients in 2005 and 2006 that some economists were predicting a bursting of the bubble and huge price declines to follow – assuming of course that the agent was paying attention to these warnings.

While this may seem reprehensible in retrospect, individual real estate agents would have had a powerful psychological need to believe that there was no housing bubble – and later that prices would land softly. This need would have arisen from the fact that a real estate agent who did not believe these things, yet failed to advise her clients that buying a home in 2005, 2006 or 2007 was a risky proposition, could not have seen herself as ethical and honest individual. However, an agent who advised her clients that buying a home was risky would have likely driven many clients away.

In other words, a real estate agent’s built-in conflict of interests – and the psychological need to see herself as ethical and honest person – would have consciously and unconsciously motivated her to selectively perceive information that supported her belief that residential real estate was a good investment and to discount information that did not. Confirmation bias, disconfirmation bias, and the tendency of individuals to engage in motivated reasoning are well-documented in scientific literature – and it’s safe to assume that real estate agents suffer from the same psychological biases as all other human beings. [The OC Register Says California had no real estate bubble.]

Additionally, real estate agents as a class would have been susceptible to herding behavior, which refers to the tendency of individuals to go along with the crowd – often despite their own misgivings. A real estate agent who had his own doubts as to the sustainability of the housing market would have been confronted by the apparent fact that few of his fellow agents agreed. If most other real estate agents were bullish on the housing market, an agent might reasonably have concluded that he must be wrong about his doubts – especially to the extent that he was not sure about his own judgment in the first place. Few individuals will stand alone and reject the reasoning of their cohort. Ironically, however, the more individuals who cast their own judgments aside and go along with the crowd, the stronger the herding behavior becomes, even though many – or even the majority – of the real estate agents in the crowd may have heard the warnings about the overheated housing market and privately feared that the herd was about to run off a cliff.

Given these psychological biases, one can also understand those real estate agents who, once the housing market began to soften, told their clients that the market was just leveling out, and would not decline. Moreover, to the extent that real estate agents believed the “all real estate is local” mantra,80 they might have felt justified in keeping any concerns or negative information about the national housing market to themselves, so as long as the buyer was not paying more than local “market prices.” In short, it’s understandable that many realtors may have chosen in 2005 and early 2006 to “accentuate the positive” and to say nothing to their clients about signs of trouble brewing in the housing market. Some might also have genuinely felt certain that their clients were making a good investment. …

Walking Away Scot-Free

Unlike buyers, who have been stuck in underwater homes, and lenders, who have also taken significant losses, the NAR has walked away scot-free from its role in contributing to the housing crash and the losses that its inaccurate advice caused homebuyers. Moreover, real estate brokers and agents have kept the billions of dollars in commissions, including $100 billion in 2005 alone, generated, at least in part, from assurances to their clients that the prices they paid for their homes actually reflected the homes’ value and that buying a home was a good investment. Indeed, the NAR indicated to the New York Times that it is not aware of any case where a real estate agent has been held liable for inaccurate representation as to a home’s value or its investment potential. Westlaw and Lexis-Nexis searches similarly reveal no cases holding real estate agents liable for price or investment advice – and many that do not.

Real estate agents generally escape liability because courts treat them as mere salespeople, or connecters of sellers and buyers, who bear no legal liability for their pronouncements about the health of the housing market or their investment advice, including statements affirmatively guaranteeing a buyer a positive return on their investment. Courts also generally refuse to hold realtors responsible when they misrepresent a property’s fair market price – or mislead investors as to a property’s rental value. Instead, courts typically hold that matters of price are matters of opinion, not fact; that the buyer is assumed to have done their own research; and that the buyer is not entitled to rely upon their agent’s opinions. Courts generally find that, absent fraud or non-disclosure of a material“fact,” real estate agents are not responsible for their opinions, no matter how wrong or recklessly given. In short, courts echo the popular view that homebuyers have no one to blame but themselves for their decision to purchase their house.

… But one might question why, if a real estate agent negligently, recklessly or intentionally made inaccurate pronouncements about the housing market or gave misleading investment advice to his client, the agent should completely escape personal responsibility for his actions – either for the advice itself or for offering opinions as to matters outside his expertise. It is unclear why the ethos of personal responsibility does not extend to the agent. Moreover, absolving real estate agents of responsibility for their advice creates a genuine moral hazard in which agents profit from the buyer’s purchase of a home, but bear no risk if the advice that they gave to induce that purchase is wrong, or intentionally misleading. Real estate agents risk other people’s money – and get paid even if the agent knows that the risk is reckless, or downright foolish.

Treating real estate agents as mere salesmen also runs counter to their self-description as professionals and to their representations to their clients that they owe them a fiduciary duty to look out for their best interest – an obligation that a mere salesperson does not have. Nevertheless, courts seem to assume that homebuyers do or should understand that, despite their agent’s protest to the contrary, their agent is no different in principle than a car salesperson. Everyone knows not to trust a car salesperson to look out for their best interests. Puffery is to be expected and one should enter a car lot at their own risk. As far as most courts are concerned, the same apparently goes for hiring a real estate agent. …

Choosing a Path

At a basic level, courts’ descriptions of what individuals should do when making complex financial decisions about whether to purchase homes (i.e. – ignore the opinions of their agents) is at odds with what people actually do (which is to seek and trust expert advice). Moreover, most people likely hire a real estate agent without any knowledge, or reason to suspect, that their agent’s “false statements concerning the market are held to be matters of opinion, judgment, seller’s talk” – and that their agents are not legally accountable for the advice that they give.

This approach is not only detached from the concrete reality of real estate transactions, but also fundamentally unfair to buyers, who are doing exactly what an amateur who must make a complex decision typically will do: engage and trust an advisor that they believe to be a qualified expert to guide them through the process. In addition to leaving unsuspecting homeowners without redress, not holding real estate agents to account runs counter to notions of professionalism and the ethos of personal responsibility.

There are two basic ways to address the discrepancy between homebuyers’ psychological propensity to trust their real estate agents and the general legal rule that buyers may not reasonably rely upon their agents’ advice. The first path is to change the legal rule, fully professionalize the real estate agents’ relationships to their clients, and formalize their fiduciary duty. The second – and opposite – path is to bring the real estate agent’s role in line with the legal rule, which means de-professionalizing the realtor-client relationship and clearly delineating real estate agents “mere salespersons.”

The first path may find the most support with real estate agents, as there has been and continues to be a substantial movement among real estate agents to professionalize their vocation. Indeed, as previously discussed, the NAR markets “realtors” as professionals and many real estate agents tend to see themselves as professionals, rather than mere salespersons. But despite strides toward professionalization, the real estate brokerage industry has still resisted legal responsibility when real estate agents negligently or recklessly offer inaccurate advice, or even intentionally manipulate their clients into making poor decisions.

If real estate agents are to be treated as “professionals,” however, they should be subject to regulations similar to those to which other advisory professionals are subject. As an analogous profession, for example, investment advisors have an “affirmative obligation” under the Investment Advisors Act “of utmost good faith and full and fair disclosure of all material facts to their clients, as well as a duty to avoid misleading them.” Investment Advisers must also be competent, “have reasonable and objective basis for investment recommendations,” and must ensure that that “any investment recommendations are appropriate considering the client's financial objectives, needs and situation.” …

Regardless of a client’s ultimate decision, being a professional carries an obligation to be vigilant in fully advising clients of the risks associated with purchasing a home (particularly in an inflated or declining market). Professional advisors should not, as the NAR Realtor Magazine suggests, push their clients “off the fence” by misleadingly suggesting that renting costs 7 times more than owning, or by telling them that they can “pretty much count on” appreciation of inflation plus 2 percent. Professional advisors should not practice scripts that “accentuate the positive” or engage in any form of puffery. Rather, they should soberly caution clients about potential negatives and positives and help clients dispassionately weight benefits and risks. And they must put their clients’ interests ahead of their own at all times, even if it means losing the sale or the client. In other words, if professionalism is to be the chosen path, real estate agents must accept a fundamental change in their role in real estate transactions. They must also give up the benefits of being mere salespersons, including the benefit of being largely free from legal liability.

If professionalism comes at too great a cost, real estate agents could embrace their role as salespersons,171 not only when sued but also when representing themselves to clients. Indeed, given that real estate agents are unlikely to agree as to the best path, there could be two categories of agents: “real estate advisors” and “real estate brokers” – just as there are investment advisors and stock brokers. In this two-tiered system, real estate advisors would be free to represent themselves as professional real estate experts (provided that they could demonstrate sufficient knowledge of real estate valuation, real estate investment and housing market economics).Such advisors might be in high demand to buyers looking to make wise purchasing decisions. But in exchange for the trust of buyers, real estate advisors would be required to accept potential legal liability similar to that of investment advisors.

Real estate brokers, on the other hand, would bear no responsibility for customers’ unwise purchasing decisions – aside from being required to disclose known material facts and defects about the property itself. In exchange for this free pass, and to protect buyers, brokers under such a system would be barred from representing themselves real estate advisors, as “professionals,” or as “experts” possessing specialized knowledge in real estate. Rather, brokers would be limited to representing themselves simply as salespersons. As salespersons, brokers could still provide many helpful services, including helping their customers find a suitable home, analyze and select neighborhoods and schools, and navigate the closing process.

But brokers would be strictly prohibited from offering advice or opinions as to the appropriate purchase price for a particular property, the current state or direction of the real estate market, or whether purchasing real estate is a wise investment decision. Broker training would emphasize that brokers are not to volunteer such opinions, and must respond to questions seeking such opinions by telling their customers that they are not legally allowed to offer an opinion. Brokers who broke this rule should also be strictly liable if their advice or opinions turned out to be inaccurate. …

Conclusion

The above discussion is not intended to disparage the majority of real estate agents who work conscientiously and ethically for their clients. Rather, the proposals in this article are all forward-looking and borne of the recognition that real estate agents – like homebuyers, mortgage brokers and banks – played a significant, if unwitting, role in creating the housing bubble and burst. In others words, by drawing lessons from the past, the proposals are designed to prevent its reoccurrence. Moreover, the hope is to engage real estate agents in discussing these forward-looking proposals – and not to punish them for past mistakes.

That said, it must be recognized that many homeowners might not currently be stuck in underwater homes if more real estate agents had listened to that voice inside themselves telling them that the market was crazy, had sought to educate themselves about the dangers of an inflated market, and had advised their clients that they might want to sit it out. Additionally, much suffering could have been avoided if the NAR had been a more objective purveyor of information to the public and to its members – instead of a cheerleader for the housing market encouraging potential buyers to get in before the “window of opportunity” closed.

A genuine moral hazard underlies the current role of real estate agents and the NAR. This moral hazard fueled the housing market bubble and contributed to the suffering of many people that the NAR and its realtor members encouraged to buy homes as prices began to decline. Unfortunately, the legal system allows real estate agents to benefit from the trust associated with portraying themselves as professionals, yet to avoid the consequences of the advice that they give – no matter how reckless or objectively misleading that advice may be. Other than their reputation, real estate agents have no skin in the game. They profit if people buy, but suffer no loss if they buy in error. This state of affairs is unfair to unsuspecting buyers and runs counter the ethos of personal responsibility. It should continue no more.

Real estate agents should be required to choose between two paths: (1) fully professionalize their role, including accepting legal liability when they negligently, recklessly or intentionally make inaccurate or misleading pronouncements about a home’s value or investment potential; or (2) embrace their role as “salespersons” and refrain from offering advice or opinions about the real estate market to their customers.

[end of academic report]

I fought the urge to add to Dr. White's already lengthy report with my agreeing comments. He laid out the case for regulating realtors clearly and backed it up with rigorous research. I highly recommend reading the unabridged version.

I think they got it all

I've been trying to find other interesting stories in the property records, so I pass on a number of run-of-the-mill HELOC abuse properties. Today's featured property stood out because these owners managed to extract the maximum value out of their tenure in this house.

The property was purchased on 3/31/1998 for $263,500. The owners used a $255,500 first mortgage and a $ 8,000 down payment. They never owed this little again.

On 9/21/1998 they refinanced with a $261,000 first mortgage and withdrew most of their down payment.

On 11/12/1998 they obtained a stand-alone second for $50,000. These owners had lived in the house only 8 months before they got their first $50,000 in free money.

On 12/28/2000 they refinanced with a $284,000 first mortgage and a $71,000 stand-alone second.

On 1/8/2003 they refinanced with a $396,000 first mortgage.

On 1/23/2004 they refinanced with a $489,250 first mortgage.

On 5/3/2005 they obtained a $70,000 HELOC.

On 2/16/2006 they obtained a $576,000 first mortgage and a $72,000 HELOC.

On 3/7/2007 they made one last trip to the home ATM for a $572,000 first mortgage and a $143,000 stand-alone second.

Total property debt is $715,000.

Total mortgage equity withdrawal is $459,500.

Total squatting time is about two and a half years so far.

Foreclosure Record

Recording Date: 11/23/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 08/09/2010

Document Type: Notice of Default

Foreclosure Record

Recording Date: 12/04/2008

Document Type: Notice of Sale

This one is bad. Think about the unceremonious fall from entitlement this family is about to endure. This property has been supplementing this families income from the day they moved in. They created a mountain of Ponzi debt, defaulted the moment the ATM was shut off, and they have been allowed to squat ever since. It will come as a big shock to them when they have to start paying for their housing. They're accustomed to the house paying them.

-$392 ………. Tax Savings (% of Interest and Property Tax)

-$546 ………. Equity Hidden in Payment

$203 ………. Lost Income to Down Payment (net of taxes)

$92 ………. Maintenance and Replacement Reserves

============================================

$2,315 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$5,490 ………. Furnishing and Move In @1%

$5,490 ………. Closing Costs @1%

$4,392 ………… Interest Points @1% of Loan

$109,800 ………. Down Payment

============================================

$125,172 ………. Total Cash Costs

$35,400 ………… Emergency Cash Reserves

============================================

$160,572 ………. Total Savings Needed

Property Details for 7 THORNWOOD Irvine, CA 92604

——————————————————————————

Beds: 3

Baths: 2

Sq. Ft.: 1458

$377/SF

Lot Size: 4,416 Sq. Ft.

Property Type: Residential, Single Family

Style: One Level, Cottage

Year Built: 1978

Community: Woodbridge

County: Orange

MLS#: S652285

Source: SoCalMLS

Status: Active

On Redfin: 1 day

——————————————————————————

Single story home located in the Woodbridge Village of Irvine. Spacious open floor plan with a large living room and a cozy fireplace. Upgraded kitchen with granite counter tops and newer cabinetry. Upgraded bathrooms, crown moldings, custom paint. Two car garage with driveway.

In the cleanup phase of the Great Housing Bubble, the lucky ones are those profiting from recycling the dead carcasses from yesteryear. I have been sifting through the debris in Las Vegas for about six months now. For a variety of reasons, I have been mum on my activities, but today I am going to share some anecdotes and lessons learned from my new adventure.

The most important of these lessons relates to the topic of today's featured article. According to the US Census Bureau, there are 167,564 houses in Nevada. That's a lot of empty homes — which is good if you want to survive as a flipper. Occupied homes are troubles magnified. Buying them is harmful to your financial health.

The pros and cons of occupied properties

Buying occupied properties at auction is always riskier because you never know what will happen with the previous occupants. I purchased two occupied houses for investors who were able to enjoy positive cashflow from the first month of ownership, so there are potential advantages. Since occupied properties have more risk, they have appealingly large margins — at least they look like they have large margins. When you factor in the lost time and the potential for litigation or damage by the occupants, houses with people in them are something to be avoided.

Squatters on my dime

I have one property I purchased in November, and the former owners are still squatting there. The former owners pulled an interesting legal move. They had the wife file for bankruptcy in her maiden name a few days after the foreclosure auction, and they put the property into the estate. Well, our search didn't pick up the bankruptcy because it wasn't in the owner's name, so we began foreclosure proceedings. Late in the process, the bankruptcy attorney accuses us of harassment, and we had no idea what he was talking about.

Once we discovered the suit, we had to initiate our own suit to have the property removed from the bankruptcy proceedings. They didn't own the property when they filed, so they can't obtain protection from the bankruptcy court to stay there. If they had filed before the foreclosure, they would have had other rights, but if they had filed before the foreclosure, it would have shown up in a title search, and I wouldn't have bid on the property.

The cost of all this legal maneuvering is expensive. The time to properly evict these people has been costly in two ways. First, the declining market means my resale price is declining while i wait. in addition, I have opportunity cost on money tied up in a non-performing asset. I am not a bank. I can't amend, extend, and pretend I am making money. I either sell quickly for a profit or I don't profit.

Ye ol' crack house

By far the most bizarre story I have is a property I purchased in October.

Back in 2005, a recent Salvadoran immigrant obtains his citizenship. With his workman's salary and a penchant for liar loans, he puts together an empire of 8 properties in Las Vegas from 2005 to 2007. The last of these properties was his crown jewel — the property I bought.

The property is in a older Las Vegas neighborhood called Spring Valley. The neighborhood is dominated by ranch style houses ranging from 1,400 SF to 1,800 SF. It has seen better days, but this is not a bad neighborhood. It is mostly median income middle-class families trying to get by.

My property is the large 5 bedroom home at the end of a cul-de-sac. It is the only one in the area with a large pie shaped lot with an outbuilding and RV parking. Back in 2007 when Vicente the Fox, our recent immigrant, bought this property with his liar loan, it was the finest property on the street.

Vicente the Fox began using his large property as a salvage yard. He put individual locks on all the bedroom doors and leased out the rooms to boarders and skimmed their rent. He tried to convince them to keep paying him even after I bought the house.

The boarders were united by their love for crystal meth. There is no evidence this place was used as a meth lab — thankfully — but when the constables came by to evict the last boarders, they confiscated a cigar box full of used pipes and other paraphernalia. In the two weeks after we took possession, the house was broken into three times.

The amount of junk on this lot is staggering. There are eight automobiles on this property, and none of those are in the garage because the garage was full of stuff. All eight cars are in the back and side yards. There were 4 working refrigerators on the property, a dirt bike, an air conditioner, anything and everything you can imagine, and lots of it.

I call our former owner Vicente the Fox because he carefully avoided us whenever we tried to serve him formal eviction papers. He didn't live at this house, and his former address is an apartment where he skipped out on the rent. However, since I was unable to serve him, I could not fully divest him from the property and the junk sitting on it.

He teams with a local attorney bandito to shake me down for wrongful foreclosure, stealing his property, and so on. Since I couldn't get him served, his weak case was strong enough to tie me up in court for a while. I settled.

Surprisingly enough, it turned out in my favor because when I let him back on the property to get his stuff, he cleared out much of the garbage along with the stuff of value. My worst fear was him picking over the good stuff and leaving me with a $5,000 mess to clean. He took a number of paint cans and other items that would have required me to bring in special disposal teams.

There is no good resolution for this property. I will lose money on the deal, and Vicente the Fox will have a roving pile of garbage scattered at friends and acquaintances houses all over town.

Eventually, this property will get sold. Hopefully, it will be to a good family that restores it as the jewel of the neighborhood. That's the outcome I want.

Flippers are maligned for bringing down the quality of life in neighborhoods. The reality is that the delinquent former owners are the ones who brought down the neighborhood. Flippers like me are the ones taking back the crack houses from rent-skimming former owners and putting families back into them.

After those two experiences, it's easy to see why dealing with vacant properties is much preferred. I'll focus on the empty ones. There are plenty to choose from.

LAS VEGAS (AP) — The promise of palm tree groves and low-priced real estate lured Alan and Katherine Ackerly across the Rocky Mountains from Denver to Nevada in 2004, where thousands of new houses beckoned brightly as any neon sign.

They came to buy their retirement home. But the real estate bust took its toll, with a flood of short sales and foreclosures in the market, and last month the Ackerly's dream home was foreclosed on, too.

“I pretty much gave it back to them,” said Alan Ackerly, a 57-year-old electrician who stopped paying his mortgage because he owed more than the house was worth.

The Ackerly's home is now among a swelling number of abandoned houses in Nevada. There were 167,564 empty houses in the state last year, according to newly released U.S. Census data, more than double the number in 2000. The number of vacant homes represents about one out of every seven houses across Nevada.

I haven't looked into the Census Bureau's methodology, but that number sounds a bit too big, doesn't it? There are unquestionably a large number of vacant homes, but that many?

The figures are another striking example of how the housing crisis has pummeled Nevada, casting a new light on the severely weakened market after years of boom.

One result is an increase in code violations. In Clark County, home to Las Vegas, such complaints nearly doubled from 2008 to 2009 and the median price of resale homes dropped to $115,000 in January.

That put's their median somewhere in the late 90s. The Las Vegas market is the apocalypse bubble bloggers predicted would occur in every market. As a reaction to Las Vegas, lenders decided it was wiser to build a huge shadow inventory. The likely have saved themselves a great deal of strategic default.

Neighbors call to complain of abandoned houses, stagnant pools, wild yards and unsecured doors, said Joe Boteilho, the county's code enforcement chief. But the neighborhoods of newly constructed homes are not facing the same blatant signs of disrepair seen in other foreclosure-ravaged states such as Florida, Michigan and California.

It has been a deep plunge for Nevada. Once a leader in job creation and construction, the state had the highest foreclosure rate in the country in January. Delinquent mortgages, meanwhile, are on the rise, with Las Vegas, Reno and Carson City all in the top eight cities per capita in a national real estate study published last month.

Strategic default will dominate the Las Vegas housing market for the foreseeable future. With prices stuck 60% below the peak, late buyers have little or no hope of getting back to breakeven in their lifetimes. How many of you are willing to work 20 years to pay off a mistake like that?

More than 16 percent of Nevadans relocated to new residences within the state in 2008 alone, the highest mobility rate in the nation, the Census data shows.

“We were the hottest market in the nation in terms of the shape of the bubble, how fast it went up,” said Nasser Daneshvary, director of the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas. “And, of course, when something goes up, it comes down hard, too.”

The growth fueled by tourism and the gaming industry has yielded few winners. Short sales and foreclosures have slashed homes prices, ravaged neighborhoods and fueled unemployment in the construction sector, one of Nevada's primary industries. The jobless rate is 14.2 percent, and the state's estimated budget gap starts at $1.5 billion.

In Fernley, the fastest growing city in Nevada from 2000 to 2010, the only sign of construction in recent months was a new Walgreens and a Catholic church. One in 49 homes is in foreclosure.

“It was just very explosive,” said Mayor LeRoy Goodman. “We hit bottom.”

The economy had become overly dependent upon construction. This cruel purging has wiped out everyone in real estate and construction. When activity returns, it will feel like a huge resurgence compared to the severe contraction of 2008. The industry will regrow into a smaller economic engine utilizing less of the workforce. Perhaps they will only build one mega-resort at a time for a while.

This in what was once the land of plenty. The expansion of glass towers and sprawling casinos on the Las Vegas Strip saw a 3.8 percent unemployment rate statewide in the beginning of 2000. Over the next decade, Nevada would grow by 35 percent, the fastest rate in the nation.

Men and women in hard hats carved homes into mountainsides, raised superstores from the dust and wedged plush golf courses into the desert. The state's residential properties grew by more than 40 percent to 1.17 million homes during those years, affording Nevada the youngest housing stock in the country in 2009, according to the Census data. In Clark County, the school district saw an average of 10 new schools a year at its peak growth.

The people who are down on Las Vegas forget its phenomenal growth prior to this recession. Las Vegas is not Detroit. Detroit watched the auto industry leave with no replacement to fill the void. The economic engine of Las Vegas is gaming and sin.

My wager is that vice will be popular in the future and people will continue to flock to Las Vegas for its vices. Therefore, Las Vegas will recover, and so will its real estate market. I could be wrong. I could lose my bet on Las Vegas's future.

As houses and condominium towers rose from the ground, so did prices. The median home price went from $150,000 to $300,000 between 2000 and 2007, according to a University of Nevada, Las Vegas study.

“It was a new town,” said Dennis Smith, president of Home Builders Research, a Las Vegas real estate firm. “There was money everywhere. Everyone wanted to invest in Vegas.”

The state's growing wealth and relaxed lending practices allowed workers with limited incomes to gain home ownership. In many cases, these were the same people who later faced foreclosure. Most Nevadans who lost their homes earned between $24,000 and $72,000, according to a homeowners survey published by the Nevada Association of Realtors in January. Roughly 60 percent said they lost their jobs first, then their homes.

The crash came in 2008, when unemployment passed 7 percent for the first time during the decade.

Even so, nearly 74,000 new homes were built in 2010, according to Census data. Realty companies said there are still buyers who prefer newly-built houses.

A general recovery seems far away. The state's Foreclosure Mediation Program helped more than 4,200 homeowners since its creation in 2009. Nearly 2,000 of those owners were able to keep their properties.

More short sales and foreclosures are projected to further depreciate homes values across Nevada in 2011. Census data to be released starting in June was expected to highlight the state's robust renters' market.

The rental market is strong because many people were booted out in a foreclosure, but they still had jobs, so they stayed in the area and rented. If there were a major exodus from the area — as is happening in Detroit — then rents would decline along with prices.

“This year will be the worst,” said Rep. Shelley Berkley, D-Las Vegas, who co-chairs the Democratic Caucus Housing Stabilization Task Force in Washington. “The unemployment rate is not going down. The values of the homes keep going down and the ability to pay your mortgage is just not there.”

The Ackerly family moved into a rental house after they defaulted on their mortgage. The value of their $240,000 North Las Vegas home was worth $80,000 by the time they left. Unlike some of their neighbors, they didn't take the new kitchen cabinets, or the palm trees they had planted in the yard, or any of the other improvements they lovingly made to the house after they moved in.

“We were done with it,” said Alan Ackerly.

The things people take and leave behind

One of the properties I bought in March had the kitchen stripped out by the former owners. It's an empty room with a pipe-hole in the wall.

For some reason, people like to leave vacuum cleaners behind. Perhaps they don't want the dust from a foreclosure in their new house? I don't know. But I find one left behind in nearly every property.

I had one property where the former owner removed every doorknob in the house, but then they left them in a pile on the floor and didn't take them. In that same house, they took the garbage disposal. What's the resale value of a used garbage disposal?

A few weeks ago I wrote about the losers who left their family pets to die. We saved them, but not before they endured countless days without food or water trapped in the back yard.

The owners of today's featured property left it broom clean. They even left a note on the water softener telling the next owner it needed service. Who does that? Who leaves a maintenance note on a property they are losing in foreclosure? Good people. That's who.

The virtue of quick processing

In early March, with B of A coming off its Nevada moratorium, I had a few properties in escrow, so I decided to deploy the last $200K I had available. The number of properties pushed through the Las Vegas auction site in March to third parties has been remarkable. I picked up five this month. Any rumors of an end to the foreclosure problems in Las Vegas will be dashed when the March foreclosure numbers are announced. Remember you heard that here first.

On March 2nd, I bought two properties, and with a new sense of urgency rivaling a FedEx operation, we got one of the two properties on the market two days later in time for weekend showing.

We still had work to do on this property. Basically, I decided to list the property while we were working on it to see what happened. Worst case is that I turn off some potential buyers who see it before it is ready. I wouldn't do that here in Irvine, but Las Vegas is a different market, so I thought I would try it.

Early the next week, even before Jacki gets crews out to start work, an interested buyer makes an as-is offer within $5,000 of my asking price. Since I was just about to embark on a $5,000 renovation, this offer was a no-brainer, and I took the deal. I was in escrow within eight days of the auction.

That was eye opening.

I realized I had been operating as if I were flipping in Irvine or Orange County. In Las Vegas time-to-market is more important than quality of presentation. The properties in my existing inventory — the stuff that is losing value as it ages — all show very well. We focused a great deal of attention on small details, and likely overspent what we should have to make these properties show well. It hasn't made a difference. Price is what sells in Las Vegas. Get to the market quickly and less expensively than your competition, or you lose money.

As good as good can get

This week as I was patting myself on the back for the quick flip, I took the money from some recent closings and bought three more properties. The featured property below was purchased on Friday, March 18, 2011. That's last Friday.

On Saturday, Jacki has the locks changed, took a few photos, and installed the Supra key. Sunday morning some prospective buyers looked at the property. Monday morning (yesterday) we got a full asking price offer which I have accepted.

Four days from auction purchase to full-price offer. We may open escrow today. It doesn't get better than that.

Property Type: Single Family Residential, Detached

Year Built: 2003

Community: Lynbrook

County: Clark

MLS#: 1129717

Source: GLVAR

Status: Exclusive Right

On Redfin: 1 day

Cumulative: 2 days

New Listing (24 hours)

————————————————-

MOVE IN READY! Not a Short Sale or REO. Quick Response from Seller. 1-Story Home, 3 Bedroom, 2 Bath in a gated community. Neighborhood near Schools, Shopping, Dining, Parks and Recreation. Charming Open Floor Plan with lots of Natural Light.

Flipping Out

I hope you enjoyed my Las Vegas anecdotes. As you can see, most of my time and energy have been devoted to that end. I don't think I have revealed any trade secrets or given my competitors any valuable information. Perhaps a few may be dissuaded from trying when they know how hard it really is.

It's a hard business, and if you don't know what you're doing, you can quickly lose a lot of money. It requires a lot of time, money, patience, the ability to accurately value property, and a working understanding of real estate law. It can be a lucrative business if you can figure out before the opportunity disappears.

Surviving the turnover of the first group of properties, I feel like I have the team and the systems in place to do well. I am looking forward to the rest of 2011. For those of you interested in my fund, I'm sorry, but it is closed to new investors. Maybe next year….

.png)

.jpg)

.jpg)

.JPG)