It is now becoming much cheaper to own than to rent in many markets. Anyone renting by choice in the Las Vegas area is a fool. Today's featured property is a Henderson, Nevada, property with a cost of ownership much lower than a comparable rental. So much cheaper to own that properties like these make great investments.

Home Address … 1608 CHESTNUT St Henderson, NV 89011

Resale Home Price …… $113,900

This place ain't doing me any good

I'm in the wrong town, I should be in Hollywood

Just for a second there I thought I saw something move

People are crazy, times are strange

I'm locked in tight, I'm out of range

I used to care, but things have changed

Bob Dylan — Things Have Changed

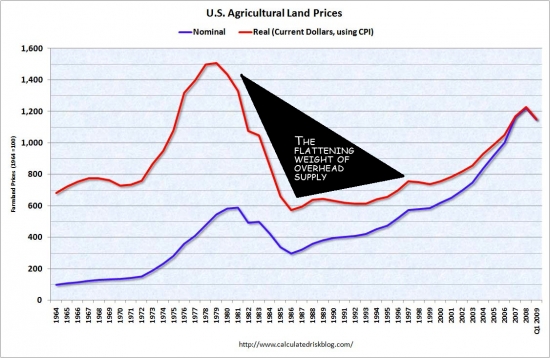

During the housing bubble prices rose to levels where owning cost twice as much as renting in many California markets. As many predicted, the deflation of the bubble is causing markets to overshoot fundamental valuations to the downside — including many here in California.

Trulia report shows buying cheaper than renting in most major metro areas

It is cheaper to buy a two-bedroom home than rent one in 72% of major metropolitan areas around the U.S., according to the Trulia rent vs. buy index released Monday.

The real estate data firm said increased demand for rental properties is driving the cost of homeownership down nationwide.

“Since the start of the Great Recession, many former homeowners have flooded the rental market,” said Pete Flint, chief executive and co-founder of Trulia. “Following the principles of supply and demand, renting has become relatively more expensive than buying in most markets.”

Trulia compared the median list price of a two-bedroom home with the median price paid for rent in 50 cities. The company then assigned a price-to-rent ratio to each city, with any number below 15 signifying a homebuyer's market and any number above 21 signifying a renter's market. Any market between those two numbers has more balanced rent versus buy costs.

The cost of homeownership includes mortgage principal and interest, closing costs, property taxes, hazard insurance and homeowner association dues. It excludes all maintenance, bills, and security costs. The cost of renting a unit includes rent and insurance.

Among the most affordable housing markets are Miami and Las Vegas, both of which have a price-to-rent ratio of 6 and where foreclosure rates have been the highest in recent years. Miami posted the highest number of foreclosures in the third quarter, according to RealtyTrac. Filings were up 9% from 2009 to about 58,600. RealtyTrac reported that Las Vegas had the highest rate of foreclosure in the third quarter, when one in every 25 housing units received a foreclosure filing.

Trulia reported that it is cheaper to buy than rent in several Texas cities, including Arlington, San Antonio and El Paso. The foreclosure rate in Texas dropped to 1.82% in the third quarter from 1.95%, according to the Texas Mortgage Bankers Association. During the third quarter, the national average home foreclosure rate was 4.39%.

The Trulia rent vs. buy index found that it is cheaper to rent than buy in only 8% of markets, including New York, Seattle, Kansas City, Mo.; and San Francisco. The price-to-rent ratios in these cities were 31, 24, 21, and 21, respectively.

In the remaining cities tracked by Trulia, the study found that buying may be a financially sound long-term option despite the affordability of renting in those markets.

“Oakland and Los Angeles, which are experiencing similar rates of unemployment or foreclosure filings as Phoenix, Miami and Sacramento, are still more affordable to renters,” the report said. “Moreover, close proximity to economic centers with promising job growth projections has propped up both the demand for homes and costs of home homeownership in Oakland and Los Angeles.”

For a complete list of housing markets in the order they rank in homebuyer affordability compared to renter affordability, click here.

Trulia is a San Francisco-based real estate data network with a searchable database of listed homes. The firm recently acquired Movity, a real estate data firm that specializes in geographical reporting.

Write to Christine Ricciardi.

Follow her on Twitter @HWnewbieCR.

What kind of property is cheaper to own than to rent?

Home Address … 1608 CHESTNUT St Henderson, NV 89011 ![]()

Resale Home Price … $113,900

Home Purchase Price … $83,200

Home Purchase Date …. 1/20/11

Net Gain (Loss) ………. $23,866

Percent Change ………. 28.7%

Annual Appreciation … 442.8%

Cost of Ownership

————————————————-

$113,900 ………. Asking Price

$3,987 ………. 3.5% Down FHA Financing

4.99% …………… Mortgage Interest Rate

$109,914 ………. 30-Year Mortgage

$23,557 ………. Income Requirement

$589 ………. Monthly Mortgage Payment

$99 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$19 ………. Homeowners Insurance

$0 ………. Homeowners Association Fees

============================================

$707 ………. Monthly Cash Outlays

-$56 ………. Tax Savings (% of Interest and Property Tax)

-$132 ………. Equity Hidden in Payment

$8 ………. Lost Income to Down Payment (net of taxes)

$14 ………. Maintenance and Replacement Reserves

============================================

$541 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$1,139 ………. Furnishing and Move In @1%

$1,139 ………. Closing Costs @1%

$1,099 ………… Interest Points @1% of Loan

$3,987 ………. Down Payment

============================================

$7,364 ………. Total Cash Costs

$8,200 ………… Emergency Cash Reserves

============================================

$15,564 ………. Total Savings Needed

Property Details for 1608 CHESTNUT St Henderson, NV 89011

——————————————————————————

Beds: 3

Baths: 2

Sq. Ft.: 1335

$ 85/SF

Lot Size: 6,534 Sq. Ft.

Property Type: Single Family Residential, Detached

Year Built: 2006

County: Clark

MLS#: 1118172

Source: GLVAR

Status: Exclusive Right Property

On Redfin: 3 days

Cumulative: 3 days

——————————————————————————

MOVE IN READY! Not a Short Sale or REO. Quick response from seller. Newly rehabbed home, all new paint inside this single story custom home in Henderson, has 3 bedrooms and 2 full bathrooms, lots of upgrades in this home. If you are looking for a reasonably priced home for your clients with no HOA Dues; you have found it.

What is the comp value?

That question is more difficult for this property than others because it was one of about a dozen properties built in 2006 and 2007 as infill in the older neighborhood. When you look at the neighborhood comps, you see many at $80,000 to $90,000, but the new stuff is all selling in a tight range at $113,000.

Comparable Sales

——————————————————————————

1628 PALM ST, 2007, 4/2, 1475 SF, $119900, $81.23/SF, 1628 PALM ST sold :$113,000

1636 PALM ST, 2007, 3/2, 1475 SF, $113500, $76.89/SF, 1636 PALM ST sold: $113,500

1612 PALM ST, 2007, 4/2, 1475 SF, $124999, $84.68/SF, 1612 PALM ST sold: $112,000

It's a great rental

I originally purchased this property to resell as a rental. Rental comps suggest it would rent for $1,100 to $1,150.

Comparable Rentals

——————————————————————————

1912 EVELYN AV — 3 bed 2 bath 1232 SF — 1998 List: $1100

505 HOLICK AV — 3 bed 2 bath 1229 SF — 1983 List: $1095

563 DUTCHMAN AV — 4 bed 2 bath 1415 SF — 1986 List: $995

519 TABONY AV — 4 bed 2 bath 1415 SF — 1986 List: $1300

554 TABONY AV — 4 bed 2 bath 1415 SF — 1986 List: $1075

1632 PALM ST — 4 bed 2 bath 1475 SF — 2007 List: $1100

205 E CORN ST — 4 bed 2 bath 1475 SF — 2007 List: $1150

| Asking Price Range | ||

| Comparable Value Full Asking Price (buy it now) | $113,900 | |

| Discounted Asking Price (reserve price) | $112,900 | |

| All Cash Purchase Financial Analysis | ||

| Net Income | $7,289 | |

| Capitalization Rate = Net Income / Total Cost | 6.4% | |

| Mortgage Purchase Financial Analysis | 15-Year | 30-Year |

| Mortgage Interest Rate | 4.6% | 5.1% |

| Actual Monthly Cashflow | $- | $115 |

| Cashflow after Financing | $3,688 | $4,072 |

| Initial Capital Investment (down payment) | $34,767 | $22,780 |

| Cash-On-Cash Return = Cashflow / Investment | 10.6% | 17.9% |

A cash buyer for this property would receive a 6.4% return on their money. A financed buyer using a 30-year fixed-rate mortgage would be cashflow positive with 20% down and earn a 17.9% return on the down payment investment.

| Rental Income | Terms | Calculations |

| Gross Rent | $1,130 | |

| Vacancy and Collection Loss | 5.0% | $57 |

| Monthly Rental Income | $1,074 | |

| Operating Expenses | Terms | Calculations |

| Property Tax | 2.67% | $253 |

| Homeowners Insurance | 0.50% | $50 |

| Maintenance and Replacement Reserves | 0.50% | $50 |

| Homeowners Association Fees | $- | $0 |

| Property Management Fees (% of Gross Rent) | 10.0% | $113 |

| Monthly Cash Expenses | $466 | |

| Net Operating Income | $607 | |

| Monthly Payment (based on maximum loan) | $492 | |

| Actual Monthly Cashflow (assuming impounds) | $115 | |

| Interest Expense (subtract from NOI to obtain P&L) | $383 | |

| Total P&L After Expenses and Debt (loan amortization plus excess) | $224 |

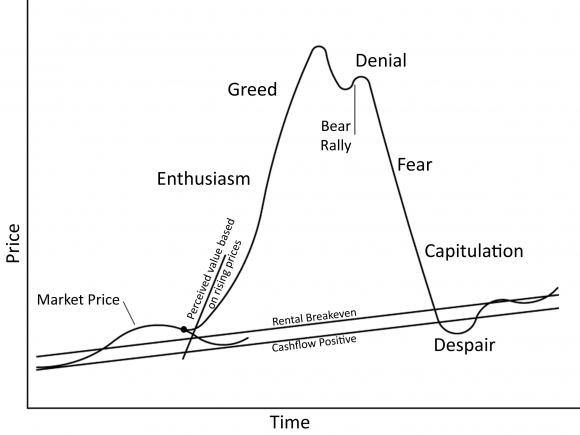

When I measure the rate of return, I include both the excess monthly cashflow and the equity hidden in the loan repayment. Also, I only consider the current cashflow. I can make the case that properties trading at mid 90s prices are due for a bounce back, but with the overhead supply, any rebound won't be for many years.

This is an investment you take because you want current cashflow with long-term asset preservation. The resale value of this property may go down for a year or two, but with cheap and stable financing, there is no reason to sell while values are depressed. There is also the very real possibility that people buying for positive cashflow will create a durable bottom and values may not decline much further on these properties.

Personally, I think the under $150K market in Las Vegas is solid, but then again, i am selling a property in that price range, so take my opinion for what it is worth. I am not a seller because I don't believe in the product. I am a seller because flipping is my business.

Who runs the show?  (2).jpg)

I have been very blessed to find the right person to run my fund's operations in Las Vegas, Jackie Evans. Jacki was recommended by my wife who knew her years ago. Jacki has always been a very hard worker, and as circumstance would have it, she was ready to make a move from the mortgage side of the industry. Her experience as a lender processing hundreds of loans gives her the organizational skills and real estate background necessary to manage the purchase-to-sell process.

Her performance to date has been outstanding, and I am becoming increasingly comfortable delegating important tasks in the process.The renovation of this property was entirely done by her. I never stepped foot on this property. I didn't have to. I think she is doing a great job, so today, we are showing her off.

What it used to be

When I bought this property at auction, I knew the property was only a few years old, and it had a great kitchen and tile in the main areas. I wasn't planning to repaint despite the garish yellow color. After some discussion, and an eager contractor offering a very good deal, we decided to repaint with a more neutral color. Perhaps my plain vanilla tastes are showing, but I prefer the new look.

Highway Robbery Cash-For-Keys

When the fund I operate is fully deployed, I purchase rental propoerties all-cash for other investors. One one of these deals, when we went to negotiate cash-for-keys, the occupant was a holdover tenant who wanted to stay. Since we didn't have to pay to get an owner to leave, renovate the property and find a renter, a significant up-front investment was eliminated. The rate of return went from about 9% to nearly 13%. That was a success. This property was not.

The owners of this property were beligerent, destitute and well educated on the cash-for-keys game. The owners told us we needed to give them $4,000 or they would rip out the cabinets, counter tops, appliances, light fixtures, celing fans, toilets, tubs, you name it, they were going to take it or destroy it. A scorched earth policy.

When we asked them if they realized what they were saying to us was illegal. The personal property was theirs, but the items afixed to the real estate was mine. They replied that they didn't care. They didn't have anything of value to take if we sued them; after all, they just lost their house.

I didn't call their bluff. It wasn't worth it. I wrote them a big check — not $4,000 but big enough — they left everything in place, and I had possession a few days later.

Usually, I don't roll over that easy, but given the circumstances, I think it was the right call. I do have some middle-class squatters in two of my properties that I wil gleefully kick to the curb after they have exhausted their legal remedies in the eviction process. After two and a half years of free living on the bank, they want two or three more months on me.

I am not the only one in this business who has seen shady stuff. Aaron Norris stopped by last year and commented on people drafting fake leases to get cash for keys. I had that on a recent property too.

Addendum

When I prepared this post, I was hoping to solicit some buyer interest. Late Friday evening I get a call that an offer for $114,100 was presented to us. I have decided to take that offer (it is FHA, so it doesn't pencil to full asking). Any of you interested in cashflow properties like this one. keep watching these weekend posts. I will display more here.

sales@idealhomebrokers.com

.jpg)