The GSEs have strayed from their original mission, and now they are being used to support bloated house prices. They should be dissolved and their function turned over to private lenders.

Irvine Home Address … 2 GLENOAKS Irvine, CA 92618

Resale Home Price …… $815,000

Time Has Frozen Still What's Left to Be

Hear Nothing

Say Nothing

Cannot Face the Fact I Think for Me

No Guarantee

Metallica — Dyers Eve

Should the government provide loan guarantees to subsidize home ownership? The arguments in favor of government subsidies all come down to putting people into homes they cannot afford in a free market. The theory is that homeowners care more for their properties and community and are less likely to cause social unrest. There is no real evidence to support this idea, but expanding home ownership has been the cornerstone of government policy since before the Great Depression. The arguments against are summarized below.

Ten Arguments Against a Government Guarantee for Housing Finance

By ANTHONY RANDAZZO From the Reason Foundation — February 9, 2011

There is a growing belief among mortgage investors, industry groups and some policymakers in Washington that some type of explicit government guarantees for mortgage lending will be necessary to undergird a new housing finance system in America. Yet whether by the sale of insurance on mortgage-backed securities or a public utility model replacing Fannie Mae and Freddie Mac with new government-sponsored enterprises, this would be a tragic mistake, repeating the errors of history, and putting taxpayers and the housing industry itself at risk. This policy summary offers ten arguments for why there should be no government role—explicit or implicit—in guaranteeing housing finance.

1. Government guarantees always underprice risk. All federal guarantees underprice risk in order to provide a subsidy for lending. That is their purpose. And taxpayers will be exposed to losses in the future, as those risks materialize.

This simple truth is inescapable, yet proponents deny this fact.

2. Guarantees eventually create instability. Guarantees failed to prevent the savings-and-loan crisis and subprime crisis. In fact, they contributed to the cause of both by distorting the market.

When people believe they have no risk, they behave in foolish ways. Why wouldn't people take out a $600,000 loan to speculate on real estate if they have no money in the deal. It's like getting the free spin or free bet at a Las Vegas casino.

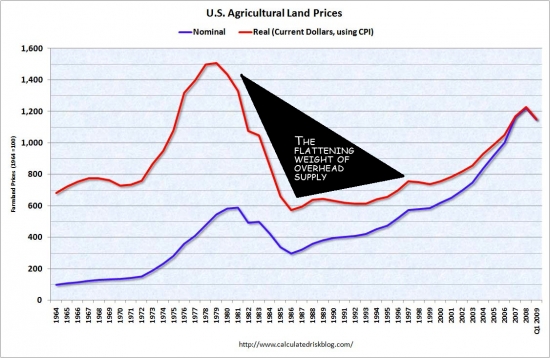

3. Guarantees inflate housing prices by distorting the allocation of capital investments. The artificially increased capital flow will make mortgages cheaper, boosting demand for housing and pushing up prices, ultimately creating another bubble.

It was private loan guarantees known as credit default swaps that caused so much money to flow into real estate and inflate The Great Housing Bubble.

4. Guarantees degrade underwriting standards over time. Historically, a primary justification for guarantees has been to increase the availability of finance to politically important groups with higher credit risks. It is inevitable that this will continue to happen, requiring the government to lower underwriting standards, and resulting in more risky mortgages.

Actually, the FHA has proven remarkably resistant to lowering its lending standards prior to the collapse of the bubble. The FHA has been around long enough to be a subprime lender — a role it has been forced into since 2008.

5. Guarantees are not necessary to ensure capitalization of the housing market. As has begun already, the jumbo market will evolve and practically any credit-worthy potential homebuyer will be able to get a mortgage in a fully private system.

Guarantees ensure more capital enters the housing market, but the secondary mortgage market is evolved enough now to exist without the GSEs to facilitate them.

6. Guarantees are not necessary for homeownership growth. Other nations have substantially higher homeownership rates in spite of having far less government interference in their housing markets.

Canada has no counterpart to the GSEs, they have no home mortgage interest deduction, and they have a higher home ownership rate than the United States. They either have better borrowers or better government policy.

7. Guarantees drive mortgage investment in unsafe markets. As long as there is a government guarantee covering financial institutions, investors and lenders will look to the government's credit, not the credit of institutions and loan applicants themselves.

This is the problem at the core of all loan insurance.

8. Guarantees are not necessary to preserve the “To Be Announced” market for selling mortgage-backed securities. If needed, a TBA market could easily develop with originators hedging against any short-term interest-rate risks in the private sector.

There is no guarantee the private sector could not provide assuming the risk can be quantified and valued.

9. Guarantees are not needed to prevent “vicious circles” that drive down prices. Mild price movements in the housing market are necessary to keep balance in the market. Keeping prices artificially high reduces housing demand and prolongs recovery. The most common threat of default as prices decline is from borrowers who have little equity in their homes—because they borrowed at high loan-to-value ratios—seeing the value of their homes drop below what they owe. Guarantees support these high-credit-risk borrowers.

Guarantees are not necessary to prevent a downward spiral in home prices because without guarantees, house prices would never become so elevated above fundamental valuations to cause worry about a downward spiral. The current downward spiral in real estate prices has required loan guarantees because prices were so elevated that the repricing of risk would have cut prices in half if not for the guarantees.

10. Even a limited guarantee on just mortgage-backed securities targeted at protecting against the tail risk will slowly distort credit allocation and investment standards, ultimately destabilizing the market and forcing the need to rely on the guarantee.

The FHA experience argues against this last point, but going forward, if we don't do something with the GSEs, reckless behavior will almost certainly take over because the government is backing all the losses. We know what we must do.

The End of Fannie Mae

Treasury wants the company phased out but punts on how to do it.

FEBRUARY 14, 2011

It's enough to make you believe in miracles: The Obama Administration is now on record as saying that Fannie Mae and Freddie Mac should go out of business. It took a global financial panic and $140 billion in taxpayer losses, but on Friday there it was in black-and-white in the U.S. Treasury's report to Congress on reforming the mortgage market: The Administration will “ultimately . . . wind down both institutions.”

This marks a break with decades of bipartisan support and protection for the two government-sponsored giants of mortgage finance. Fannie Mae has its roots in the Roosevelt Administration, and a phalanx of bankers, mortgage lenders, homebuilders and Realtors worked together to keep the companies growing and federal mortgage subsidies flowing. Now even some Democrats—though not yet those on Capitol Hill—admit their business model was a catastrophe waiting to happen.

This is a Wall Street Journal editorial, so the right-wing political posturing pervades the article. However, their point is true: it took a complete catastrophe for politicians to admit failure.

Under the Administration's proposals, Fan and Fred wind down over five to seven years. The two mortgage giants would, in effect, gradually price themselves out of the mortgage finance market by raising guarantee prices and down payment requirements, while lowering the size of the mortgages they could securitize and guarantee. This sounds like a plausible set of first steps to lure private capital back into the mortgage market, where some 92% of all new mortgages are currently underwritten or guaranteed by the government.

That is an excellent idea for phasing out these monsters. If you take away their margins, competitors will slowly emerge and take up the slack.

The $5 trillion question, however, is what would replace Fan and Fred. And here the Obama Administration has punted, offering the “pros and cons” of three broad proposals without endorsing any one of them.

Door No. 1 is the best of the lot by our lights. Under this option, federal guarantees would be limited to Federal Housing Administration (FHA) loans for lower-income buyers and VA assistance for veterans and farm programs—each a narrowly targeted market segment. A Treasury official says this would reduce the taxpayer backstop over time to about 10% to 15% of the mortgage market.

The Administration puts the case for federal withdrawal from the broader housing market in compelling terms: “The strength of this option is that it would minimize distortions in capital allocation across sectors, reduce moral hazard in mortgage lending and drastically reduce direct taxpayer exposure to private lenders' losses.” Bravo.

Treasury points to other benefits: “With less incentive to invest in housing, more capital will flow into other areas of the economy, potentially leading to more long-run economic growth and reducing the inflationary pressure on housing assets. Risk throughout the system may also be reduced, as private actors will not be as inclined to take on excessive risk without the assurance of a government guarantee behind them. And finally, direct taxpayer risk exposure to private losses in the mortgage market would be limited to the loans guaranteed by FHA and other narrowly targeted government loan programs: no longer would taxpayers be at direct risk for guarantees covering most of the nation's mortgages.”

Those two paragraphs more or less sum up 20 years of Journal editorials on housing.

The political right must be ecstatic. They are getting everything they have every wanted with housing. Those two paragraphs from a government report summarize the situation better than I can.

So what's not to like? The Administration says this option could reduce access to credit for some home buyers, and that it would leave the government without the tools to intervene in a future crisis. As for the credit point, other countries have high rates of home ownership with far less government support. If the government stands aside, it would open the way for alternative forms of finance, such as covered bonds, that now can't compete in the U.S. because of government favoritism for the 30-year mortgage model. This would open options for borrowers by increasing the diversity of financing.

As for a future crisis, government intervention is less likely to be needed if the market isn't distorted by government subsidies in the first place.

Amen. Just as affordability products make prices unaffordable, subsidies create the market need for future supports and subsidies.

Behind Door No. 2 is a rump Fan or Fred, one that would stay small in “normal” times but stand ready to step in with Uncle Sam's firepower in a future housing-finance crisis. But as the Administration acknowledges, it would be difficult both to stay small and retain the capacity to go large when needed. We'd add that the political pressure to expand any federal mortgage-lending program would be too great for lawmakers to resist. Within a generation, the winding down of Fan and Fred would be unwound.

Can the GSEs Exist Outside of Government Conservatorship? No. they can't. If they try to keep it around, it will become a political Hydra. Each time we cut off its head, two more will grow in its place.

But the greatest danger lies behind Door No. 3, which looks like Fannie in a new suit. Under this last option, the Administration envisages a group of tightly regulated, well-capitalized private mortgage insurers whose policies would be backstopped by government reinsurance. The government would charge premiums for this insurance, “which would be used to cover future claims and recoup losses to protect taxpayers.” This reintroduces the lethal mix of private profit and public risk by other means.

The problem with Fan and Fred from the beginning was not—despite the Administration's claims—that the profit motive corrupted their benign goals. Rather, the political influence and financial power of the housing lobby ensured that the companies operated outside the normal rules of politics and financial discipline. Thanks to an implicit government guarantee, the market never put any limit on their growth, even as their liabilities climbed into the trillions. Few politicians had the nerve to challenge a housing lobby that would attack them for opposing home ownership. The same political flaws would afflict a future reinsurer and its coterie of putatively private insurers.

The power of the housing lobby is implicit even in the Treasury's refusal to pick a preferred reform. As with entitlement reform, the Administration is leaving the hard work to House Republicans, who will bear the brunt of the political blowback. A reasonable GOP fear is that the Administration, whatever its rhetoric now, will pounce with a veto when it's politically advantageous—in, say, 2012.

Our view is that there should be no federal housing guarantee. If Congress wants to subsidize housing for the poor, it ought to do so explicitly through annual appropriations. One lesson—perhaps the most important—of the financial crisis is that broad policy favors for housing hurt every American by misallocating capital and credit. The feds created incentives to pour money into McMansions we didn't need while robbing scarce capital from manufacturing, biotech and other uses that might have created better jobs and led to a more balanced and faster growing economy.

We realize this is political heresy, but it is the beginning of wisdom in getting government out of the mortgage market. We're glad to see the Administration concede this rhetorically, even if it lacks the courage to embrace its logical policy conclusions.

The conservatives are right on this issue. The GSEs need to be dismantled. The FHA can stay in its current form and continue to provide the emergency backstop market protection it always has. The GSEs are redundant, and their current form of private ownership with public guarantees on the losses is dangerous.

Walking away from $400,000

Today's featured property is not for sale. It is a recent closing in Oak Creek that sold at a loss of about $180,000 after commissions. At first glance this doesn't seem like a big loss, but when you factor in the $200,000 or more this owner spent on upgrades, this house turned into a money pit.

With current financing conditions, this property would cost about $3,500 per month to own. Would it rent for that? If I could afford it, I would pay $3,500 a month to live there. I wouild be delighted to show a deal like this and say I bought it. (I didn't.) Those buyers are as happy as anyone can be that just paid $815,000 for a beautiful tract home in a nice but somewhat noisy neighborhood. I could see spending many happy hours in that pool. I love this house. Isn't the three-car garage cool? 😉

This is perhaps the nicest property I have seen transact at a price I thought was at rental parity.

Irvine Home Address … 2 GLENOAKS Irvine, CA 92618 ![]()

Resale Home Price … $815,000

Home Purchase Price … $945,000

Home Purchase Date …. 6/19/06

Net Gain (Loss) ………. $(178,900)

Percent Change ………. -18.9%

Annual Appreciation … -3.2%

Cost of Ownership

————————————————-

$815,000 ………. Asking Price

$163,000 ………. 20% Down Conventional

5.02% …………… Mortgage Interest Rate

$652,000 ………. 30-Year Mortgage

$169,138 ………. Income Requirement

$3,508 ………. Monthly Mortgage Payment

$706 ………. Property Tax

$252 ………. Special Taxes and Levies (Mello Roos)

$136 ………. Homeowners Insurance

$136 ………. Homeowners Association Fees

============================================

$4,738 ………. Monthly Cash Outlays

-$858 ………. Tax Savings (% of Interest and Property Tax)

-$781 ………. Equity Hidden in Payment

$319 ………. Lost Income to Down Payment (net of taxes)

$102 ………. Maintenance and Replacement Reserves

============================================

$3,520 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$8,150 ………. Furnishing and Move In @1%

$8,150 ………. Closing Costs @1%

$6,520 ………… Interest Points @1% of Loan

$163,000 ………. Down Payment

============================================

$185,820 ………. Total Cash Costs

$53,900 ………… Emergency Cash Reserves

============================================

$239,720 ………. Total Savings Needed

Property Details for 2 GLENOAKS Irvine, CA 92618

——————————————————————————

Beds: 4

Baths: 3

Sq. Ft.: 2273

$359/SF

Lot Size: 6,130 Sq. Ft.

Property Type: Residential, Single Family

Style: Two Level, Traditional

View: Pool, Faces Northwest

Year Built: 2000

Community: Oak Creek

County: Orange

MLS#: S633860

Source: SoCalMLS

Status: This home is sold and off the market.

——————————————————————————

Huge corner lot with magnificent custom salt water PRIVATE POOL & oversized 8-person SPA and waterfall. Volcano-blower with FOUNTAIN effect in shallow-end. Flagstone decking, raised patio and Slate-tiled BBQ area. GOURMET KITCHEN with Solid Cherry-Wood cabinets, including pull-outs & easy-touch drawers. High-end STAINLESS STEEL APPLIANCES. Tumbled travertine backsplash with imported tile inlay. SLAB GRANITE COUNTERS. Upgrades galore. Dark HARDWOOD FLOORS in living room, family room, upstairs hallway and Bull Nose stairs. Custom stone fireplace. Custom built-in entertainment center. Decorator paint. Recessed lighting. Luxurious ITALIAN TUMBLED TRAVERTINE SPA SHOWER, huge tub, custom mosaic tile accents, dual sinks. OVERSIZED WALK-IN CLOSET. Shoe closet holds 80 pairs of shoes! Convenient upstairs laundry. 3-CAR GARAGE with storage cabinets. YOU WILL LOVE THIS HOUSE! Really close to the many association amenities, elementary school, upscale shops & restaurants!

.jpg)

.jpg)

.jpg)