What will 2011 bring?

Irvine Home Address … 55 GRAY DOVE Irvine, CA 92618

Resale Home Price …… $1,350,000

But now, I stand alone with my pride

And dream, that you're still by my side

But that was yesterday

I had the world in my hands

But it's not the end of my world (ooh ooh ooh)

Just a slight change of plans

That was yesterday

But today life goes on

No more hiding in yesterday (ooh ooh ooh)

'Cause yesterday's gone

Foriegner — That was Yesterday

For the last few years, I have started with predictions. Last year, I had this recap and predictions:

Recap of Past Predictions

First, I wrote Predictions for 2008, and last year I wrote Predictions for 2009. Nothing too bold or surprising either time:

“Most of the macroeconomic conditions I made in 2008 are still operative, and several of the predictions I made which came true will likely repeat in 2009. These are:

- 2008 will see the worst single-year decline in the median house price ever recorded

- One or more of our major financial institutions and one or more of our major homebuilders will fail

- A severe local recession

- I predict we will see many more angry homedebtor’s troll the blog

I do not believe 2009 will see median house prices decline as much as 2008, but I do believe they will drop significantly, particularly in high-end neighborhoods. The low-end neighborhoods are closer to the bottom than to the top, so 30%+ declines in these neighborhoods are not likely. The high end neighborhoods will experience big drops. Most did not drop 30% last year, so they have more room to drop. The unemployment rate is high, and the economy is in recession which will put pressures on home prices. The dreaded ARM problem is not going away, and these loans will start blowing up this year and on through 2011.”

Not much has changed from my review of the situation a year ago. Lenders did manage to avoid dealing with the problem for a full year, so prices did not budge, and we now have a massive shadow inventory.

“However, there is one bright spot for the housing market that will blunt the declines in 2009: ultra-low mortgage interest rates. We will see properties at rental parity in 2009. The low interest rates are going to reduce the cost of borrowing to the point that many properties will reach rental parity this year.”

I got that one right, and

“With the low interest rates, and with the foreclosures resulting from this year’s loan resets being a year away, we are in a good position to see our first bear market rally. This summer, we might see two or three months of sustained appreciation.”

That happened too, and it happened for the reasons described. As I have noted on other occasions, these conditions are not sustainable.

Predictions for 2010

In looking ahead to 2010, I see a number of important factors that will influence the housing market. Many of the issues discussed today will be the focus of future posts.

Mortgage interest rates will increase in 2010

I don't know how high they will go, but mortgage interest rates will begin their ascent to a (somewhat) natural market. Any stable homeowner who has not refinanced should do it now or forever miss their chance.

This one I got wrong, but only barely.

The interest rate on the mortgage averaged 4.86% in the week ended Thursday, up from 4.81% in the prior week, according to Freddie Mac, a buyer of residential mortgages. A year ago, this mortgage averaged 5.14%.

“For the year as a whole, 30-year fixed mortgage rates averaged just below 4.7%, which represented the lowest annual average since 1955, when the average price of a home was $22,000,” said Frank Nothaft, chief economist at Freddie Mac, in a statement.

With the rise in interest rates over the last 6-8 weeks, interest rates are now within 0.28% of where they started the year, and the strength of the trend reversal suggests we will likely see 5.14% interest rates and perhaps higher in 2011.

I have no idea what interest rates will do. I think they will move higher, but I haven't beaten a coin flip so far. Perhaps the explicit government gurantee on FHA and GSE debt will keep money in residential mortgages even as better rates of return in riskier assets entices some investors. If risk adverse money thinks mortgage loans are a bulletproof investment because the US government is specifically backing the repayment of the loan through the insurance sold by FHA and now the GSEs. This guarantee may cause money to pool in residential mortgages for safety and keep interest rates very low for a long time. It could go either way, and I have no foresight for either scenario. Flip a coin: heads rates go up, and tails rates go down. Ask the magic 8-ball, “Will interest rates go up?” It told me, “Maybe.”

The direction of mortgage interest rates is important for two reasons. One, it motivates people to lock in long term rates. The days of floating your rate lock are over. Playing for short term volatility by delaying your rate lock fights against the broader trend. Rising rates will also stop the refinance market. The days of Ponzi borrowing cheap money are over.

The second reason higher rates is important is because higher rates create costs that cannot be passed on to a borrower who is already borrowing at their limit (see everyone in California). As interest rates go up, the amounts people can finance with a 31% DTI go down. You can't escape the math.

- Incomes must go up — which doesn't seem likely in the face of high unemployment — or

- Debt-to-income ratios are relaxed so borrowers can borrow more. That is called a Ponzi scheme, so to avoid further losses, the DTI will stay capped at 31% for the foreseeable future.

- Loan balances must decrease. This is the most likely scenario since incomes are not going up, and neither are DTI ratios.

Smaller loan balances makes for lower bids from potential buyers. The desire for real estate may be strong, the measurable demand will be shrinking along with loan balances. Prices would have to move lower with the inventory that needs to move through the system.

Inventory will increase in 2010

Eventually, lenders are going to have to foreclose on properties, kick out the squatters, and resell the houses in the resale market. Inventory is coming; how much of that we will see in 2010 is anyone's guess, but I believe we will see much more than we saw in 2009.

Affordability will improve as mid to high end properties are released to the market, and prices of the houses of greatest interest to buyers in Irvine should come down because, despite the buyer interest, there are more properties in distress than there are buyers interested in obtaining them.

One year ago there were 446 homes on the MLS. On the last business day of 2011, there were 725 homes for sale in Irvine. That's an increase of over 60%! I mark that down as a win.

Properties selling at or below rental parity becomes the norm in 2010.

As I have noted on other occasions, many properties, even in Irvine, are trading at or below rental parity. This will happen more often, and it will happen at higher and higher price points.

This is what we observed in late 2010 due to falling prices and super low interest rates.

Sales volumes will increase in 2010

Despite the rumors of a healthy real estate market, transaction volumes remain 15% below historic norms on a seasonally adjusted basis. Sales volumes will increase due to greater supply, and prices will go down.

Sales were up slightly, but not much. Unemployment continues to be a problem and the lack of a move-up market continues to plague sales.

Prices in Irvine will fall 2%-5% in 2010

Increasing interest rates will decrease affordability, and increasing supply will force saleguaranteehe market. The combination will cause prices to begin a multi-year slow decline similar to the 1994-1997 period. The price decline will not be orderly, and the relative stability in the median will mask seismic shifts within the market at sales composition changes (more mid to high end properties will sell) and prices of individual properties decline.

Even though the rally fizzled out, it may have carried prices up enough to stop them from going negative year-over-year. I concede defeat.

Basically, my outlook for 2011 is unchanged from 2010. (1) Inventory will go up. (2) Properties selling at or below rental parity will be the norm. (3) Sales volumes will increase. (4) Prices in Irvine will fall 2% to 5% in 2011.

Whatever the result, the leg down in pricing from the double-dip will be the last move down in this market cycle. The housing market will bottom at different times in different market tiers. I think the biggest discounts will be at the high end going forward. The lowest tier of the housing market may have already hit bottom. If not, it will bottom first. With low end support producing the first wave of move-up equity buyers, the slow grinding declines of higher price points can finally cease, perhaps in 2014. During the next three years, expect a range-bound housing market with a slightly lower bias.

If you want a series of projections on the housing market I like, check out Calculated Risk's post:

Question #1 for 2011: House Prices

Two weeks ago I posted some questions for next year: Ten Economic Questions for 2011. I'm working through the questions and trying to add some predictions, or at least some thoughts for each question before the end of year.

1) House Prices: How much further will house prices fall on the national repeat sales indexes (Case-Shiller, CoreLogic)? Will house prices bottom in 2011?

There is no perfect gauge of “normal” house prices. Changes in house prices depend on local supply and demand. Heck, there is no perfect measure of house prices!

That said, probably the three most useful measures of house prices are 1) real house prices, 2) the house price-to-rent ratio, and 3) the house price-to-median household income ratio. These are just general guides.

Real House Prices

The following graph shows the Case-Shiller Composite 20 index, and the CoreLogic House Price Index in real terms (adjusted for inflation using CPI less shelter).

Click on graph for larger image in graph gallery.

In real terms, both indexes are back to early 2001 prices. Also both indexes are at post-bubble lows.

As I've noted before, I don't expect real prices to fall to '98 levels. In many areas – if the population is increasing – house prices increase slightly faster than inflation over time, so there is an upward slope in real prices.

If real prices fall to 100 on this index (seems possible) that implies about a 10% decline in real prices. However what everyone wants to know is the change in nominal prices (not inflation adjusted). If real prices eventually fall 10%, that doesn't mean nominal prices will fall that far. House prices tend to be sticky downwards, except in areas with a large number of foreclosures. That is key a reason why prices have been falling for years, instead of adjusting immediately.

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

Here is a similar graph through October 2010 using the Case-Shiller Composite 20 and CoreLogic House Price Index.

This graph shows the price to rent ratio (January 1998 = 1.0).

I'd expect this ratio to decline another 10% to 20%. That could happen with falling house prices or rents increasing (recent reports suggest rents are now increasing).

Price to Household Income

The third graph shows the Case Shiller National price index (quarterly) and the median household income (from the Census Bureau, 2010 estimated).

Once again this ratio is still a little high, and I'd expect this ratio might decline another 10%. That could be a combination of falling house prices and an increase in the median household income.

This isn't like in 2005 when prices were way out of the normal range by these measures, but it does appear prices are still a little too high.

House Prices and Supply

The final graph (repeat) shows existing home months-of-supply (left axis), and the annualized change in the Case-Shiller composite 20 house price index (right axis, inverted).

House prices are through October using the composite 20 index. Months-of-supply is through November.

We need to continue to watch inventory and months-of-supply closely for hints about house prices. Right now house prices are falling at about a 10% annual rate.

Note: there have been periods with high months-of-supply and rising house prices (see: Lawler: Again on Existing Home Months’ Supply: What’s “Normal?” ) so this is just a guide.

My guess:

I think national house prices – as measured by these repeat sales indexes – will decline another 5% to 10% from the October levels. I think it is likely that nominal house prices will bottom in 2011, but that real house prices (and the price-to-income ratio) will decline for another two to three years.

Some of you take this far too seriously

I enjoy writing for the IHB, and I try to do it the best I can given the new demands on my time. I don't get to spend as much time in the comments as I would like, but i do read them every day and participate from time to time. Mostly I have said what I had to say in the post, and making a comment would have merely restated the post, so i don't bother. I prefer others to have the last word.

When I started out writing for the IHB back in early 2007, people needed to be warned about the impending house price crash, and I was unequivocal in my message not to buy a house. As the price crash ran its course, house prices in many markets became very affordable, but Irvine has only recently seen some deals trade at or below rental parity. In some markets the discount to own versus renting is close to 40%. Can you imagine that?

With the changing conditions, I began to change my message. I began telling people they can buy with the understanding that the house price may likely decline for a few years then recover slowly. If you need to sell in the next 3 to 5 years, don't buy now. Shevy has been saying the same thing since we began working together. It's still true, but the bottom window may be in 1 to 4 years rather than 3 to 5. Buying does not hurt on a nominal basis if you hold for at least 7 years. By then between the loan amortization and the stabilized market, there should be enough equity to pay a realtor and get out, perhaps with a few extra dollars if we inflate another bubble.

When I write for the IHB, i like to be creative, and sometimes that includes trying to capture an emotion or attitude in a cartoon or pull it out of a news story. Sometimes will will advocate positions or write in a certain style because it is fun, not because it is some deeply held belief. I enjoy the humor in the stories, and the culture of home price appreciation Ponzies is a funny item to document. They are part of the housing story. I didn't cast the part, I merely report the activity and note it for what it is. It's the entitlement that is shocking to me. And the huge dollar amounts borrowed and spent is shocking too. These borrowers ripping off the banks that gave them the free money… well, what does two wrongs make?

I don't stress much about the Ponzis. I write about them because they are the story. They are not the majority in Irvine. Most people here are good people who work hard and save money. Kudos to them. However, Ponzies have a significant presence as evidenced by the property records, and the toll the market must pay for their activities is yet to be paid.

The IHB is still just a hobby. I write some crazy stuff about housing, and people stop by to read it. It's a laugh. Don't take it too seriously. I don't.

Seriously, we will continue to improve

Writing for the IHB is a great personal discipline for me. It takes habits and deadlines that must not be missed. I have tried to make each post feel thought through and cared about. I want to continue to present information to a high standard. Unfortunately, I must accomplish this within the time available. I will improve in 2011.

We plan to provide more market data and other information. I don't know what form that will take, but I would like to present understandable housing market data. There are other bells and whistles we are considering, but for now, I will remain mum until we have something ready to debut.

Most people who look for a home in Irvine search on the internet and when they do, they nearly all find the IHB. Unfortunately, not all of these people find what they are looking for. We hope we can serve more of their needs with future site enhancements.

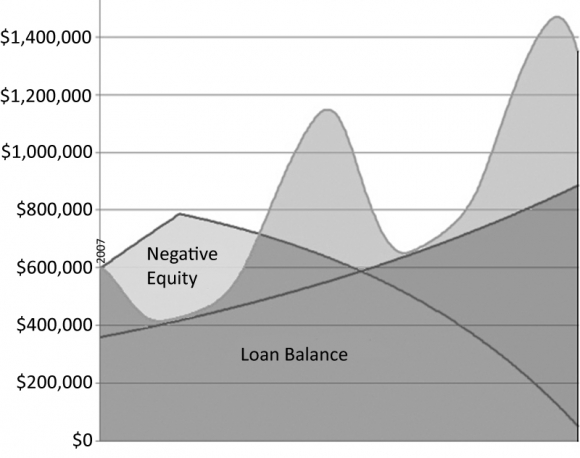

Irvine Home Address … 55 GRAY DOVE Irvine, CA 92618 ![]()

Resale Home Price … $1,350,000

Home Purchase Price … $1,110,000

Home Purchase Date …. 12/5/2007

Net Gain (Loss) ………. $159,000

Percent Change ………. 14.3%

Annual Appreciation … 6.4%

Cost of Ownership

————————————————-

$1,350,000 ………. Asking Price

$270,000 ………. 20% Down Conventional

5.07% …………… Mortgage Interest Rate

$1,080,000 ………. 30-Year Mortgage

$281,763 ………. Income Requirement

$5,844 ………. Monthly Mortgage Payment

$1170 ………. Property Tax

$450 ………. Special Taxes and Levies (Mello Roos)

$225 ………. Homeowners Insurance

$175 ………. Homeowners Association Fees

============================================

$7,864 ………. Monthly Cash Outlays

-$1511 ………. Tax Savings (% of Interest and Property Tax)

-$1281 ………. Equity Hidden in Payment

$536 ………. Lost Income to Down Payment (net of taxes)

$169 ………. Maintenance and Replacement Reserves

============================================

$5,777 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$13,500 ………. Furnishing and Move In @1%

$13,500 ………. Closing Costs @1%

$10,800 ………… Interest Points @1% of Loan

$270,000 ………. Down Payment

============================================

$307,800 ………. Total Cash Costs

$88,500 ………… Emergency Cash Reserves

============================================

$396,300 ………. Total Savings Needed

Property Details for 55 GRAY DOVE Irvine, CA 92618

——————————————————————————

Beds: 3

Baths: 3 full 1 part baths

Home size: 2,717 sq ft

($497 / sq ft)

Lot Size: 5,227 sq ft

Year Built: 2007

Days on Market: 58

Listing Updated: 40485

MLS Number: S637990

Property Type: Single Family, Residential

Community: Portola Springs

Tract: Lasc

——————————————————————————

Beautifully customized home with spacious floor plan and architectural features such as rounded corners and door arches. Highly upgraded throughout including the gourment kitchen with granite countertops, custom cabinetry, high end stainless steel appliances and a wine frig/bar area. Travertine flooring downstairs, designer carpet upstairs, custom cabinetry in all baths, solid wood doors, custom shutters, surround sound system, epoxy finished garage floor and much more. The tropically landscaped backyard includes over $100k in upgrades with a travertine patio, pool, spa, BBQ, bar and firepit. Must see to appreciate!

gourment?

Banks need a moral stigma to be associated with loan repayment. If the transaction were viewed by borrowers as a simple business transaction — which it is — then issues of morality are not effective at cajoling debtors into repayment, particularly when default is in the best interest of the debtor. Banks have long relied on borrower morality to get repaid.

Banks need a moral stigma to be associated with loan repayment. If the transaction were viewed by borrowers as a simple business transaction — which it is — then issues of morality are not effective at cajoling debtors into repayment, particularly when default is in the best interest of the debtor. Banks have long relied on borrower morality to get repaid.

Given these circumstances, only during brief periods of upward volatility (sucker rallies) is it possible to reap major appreciation benefits from owning residential real estate. It has always been about utility of ownership, but people are only now detoxifying from the kool aid enough to see it.

Given these circumstances, only during brief periods of upward volatility (sucker rallies) is it possible to reap major appreciation benefits from owning residential real estate. It has always been about utility of ownership, but people are only now detoxifying from the kool aid enough to see it.

This Luxury Built Pardee Home is situated at the end of the cul-de-sac Nestled alongside Nature. Step thru the Gated entryway to two sitting areas, Built-in BBQ features Granite top seating gather around the firepit or just enjoy the nearly 10,000 sq. ft. lot and upgraded hardscaping. 5 bedrooms & Bonus Room allow room for any family needs. Designer Mahogany cabinetry, Viking Professional Stainless Steel appliances, Blt-in desk, Baltic Brown Granite Counters Center island w/bar seating. Living/Family Room Fireplaces. Spacious Family Room with cozy breakfast nook. Laura Ashley Plantation Shutters throughout. Recessed Lighting, Wired for surrond sound or security. 3 car garage features Remoteless entry & Epoxy flooring. Master suite features elegant Master Bath with jacuzzi tub and dual shower fixtures. Upstairs laundry room. Upgraded carpeting and neutral decor makes it easy for this to be your new home, VERY CLEAN and hardly lived it.

This Luxury Built Pardee Home is situated at the end of the cul-de-sac Nestled alongside Nature. Step thru the Gated entryway to two sitting areas, Built-in BBQ features Granite top seating gather around the firepit or just enjoy the nearly 10,000 sq. ft. lot and upgraded hardscaping. 5 bedrooms & Bonus Room allow room for any family needs. Designer Mahogany cabinetry, Viking Professional Stainless Steel appliances, Blt-in desk, Baltic Brown Granite Counters Center island w/bar seating. Living/Family Room Fireplaces. Spacious Family Room with cozy breakfast nook. Laura Ashley Plantation Shutters throughout. Recessed Lighting, Wired for surrond sound or security. 3 car garage features Remoteless entry & Epoxy flooring. Master suite features elegant Master Bath with jacuzzi tub and dual shower fixtures. Upstairs laundry room. Upgraded carpeting and neutral decor makes it easy for this to be your new home, VERY CLEAN and hardly lived it.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)