Detailed stats on the Irvine housing market are something we are always

interested in. The Inventory number in the sidebar comes from

ZipRealty. A chart of those numbers shows some interesting trends. We also have some great resources provided by ipoplaya and IrvineRealtor.

A new resource we just learned about are the Neighborhood Analytics that Redfin launched. Irvine charts available after the jump…

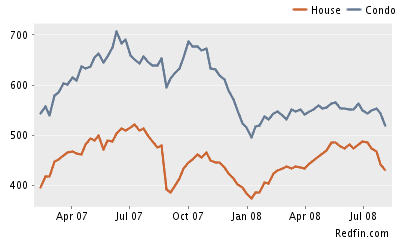

Irvine: Number of Homes for Sale

Irvine Homes: $/Sq. Ft.

{adsense}

Irvine Condos: $/Sq. Ft.

All of these charts can be found on the Irvine page at Redfin. Another cool thing about these charts is that they are also available by neighborhood (ie Northwood, Oak Creek, etc) and by zip. Take a look and let us know if you see anything interesting.

Do you remember the days when a relatively low-priced property would bring out the knife catchers and get bids over the ask? Those days appear to be behind us. The price on today’s featured property was dropped $100,000 at the beginning of the month, and it is still there. It is discounted 30% off its 2005 purchase price which likely represents almost 35% off the peak valuation. With another $70,000 to $90,000 off, this property would be at rental parity. Prices are still free fallling, but at least a potential bottoming figure is in sight. To be honest, I did not think we would be seeing prices like this in 2008.

POPULAR GARDEN ESTATES HOME WITH SPACIOUS, OPEN FLOOR PLAN. STEP DOWN

LIVING ROOM WITH WOOD BEAMS&COZY BRICK FIREPLACE. LARGE KITCHEN

WITH DOUBLE OVEN, PANTRY WITH NOOK AREA. FAMILY ROOM WITH WECOND BRICK

FIREPLACE & BUILT IN BOOK SHELVES. LIGHT TEAK WOOD FLOORS.

PLANTATION SHUTTERS THROUGHOUT. NEWER LIGHT, BERBER CARPET, LARGE

MASTER SUITE WITH DUAL VANITIE, LARGE TUB&SEPARATE SHOWER.

CATHEDRAL CEILINGS. NEWER HVH DIGITAL HEATING SYSTEM. BUILT IN

CEDAR&ORGANIZERS IN CLOSETS. TROPICAL BACKYARD WITH FOUNTAIN.

ROMANTIC JACUZZI AND PALM TREES!!!

COZY BRICK FIREPLACE? Is it just me or do the words “cozy” and “brick” seem incongruous when put together?

WECOND?

ALL CAPS and three exclamation points.

Today’s owners are losing some of their own money. The property was purchased on 9/22/2005 for $780,000. There is a $624,000 Option ARM first mortgage with a 1% teaser rate, and a $78,000 HELOC. If this HELOC was used for the purchase, the downpayment was $78,000. If not, the downpayment was $156,000. It seems likely this 10% was put toward the purchase. Either way, all downpayment money is gone, and the first mortgage is significantly imperiled. If this property sells for its asking price, and if a 6% commission is paid, the total loss on the property will be $263,094. The loss to Countrywide/Bank of America will be $185,094.

I hope you have enjoyed this week at the Irvine Housing Blog. Come back next week as we

continue chronicling ‘the seventh circle of real estate hell.’ Have a great weekend.

🙂

.

Shes a good girl, loves her mam a Loves jesus and america too Shes a good girl, crazy bout elvis Loves horses and her boyfriend too

Its a long day living in reseda Theres a freeway runnin through the yard And Im a bad boy cause I dont even miss her Im a bad boy for breakin her heart

And Im free, free fallin Yeah Im free, free fallin

All the vampires walkin through the valley Move west down ventura boulevard And all the bad boys are standing in the shadows A ll the good girls are home with broken hearts

And Im free, free fallin Yeah Im free, free fallin Free fallin, now Im free fallin, now im Free fallin, now Im free fallin, now im

I wanna glide down over mulholland I wanna write her name in the sky Gonna free fall out into nothin Gonna leave this world for a while

And Im free, free fallin Yeah Im free, free fallin

What were the guys over at IndyMac smokin’? I recently spoke with two developers who have looked at the IndyMac portfolio of large loans. They both said it was nearly impossible to value because it was such an eclectic mix of properties with appraisals of dubious quality. There is a great post at Appraisers Forum on the nonsense over at IndyMac. In residential home lending, IndyMac had positioned itself as the leader in Alt-A loans.

Tanta at Calculated Risk has a great discussion in her post Reflections on Alt-A. Her basic premise is that Alt-A was never a good business plan. Alt-A loans were generally stated-income and low-doc loans given to people with high FICO scores. The theory was that people who could be responsible with normal debts could do just as well with enormous debts. It isn’t working out too well, particularly for IndyMac.

One of the intriguing ideas from her post is that Subprime will return, albeit in a different form. There has been much discussion about how people who have gone through foreclosure will get back into the housing market. Subprime was originally intended to take people with poor FICO scores that had good income and savings and give them bridge financing until they could repair their FICO scores and refinance into conventional loans. This business model will probably return in a few years as there will be many people in this category. However, Alt-A is likely dead, and it will not be resurrected. Stated-Income, High CLTV, and low or no-doc loans will probably not resurface no matter how good a persons FICO score is simply because people will default on these loans not matter how responsible their past history.

So where does that leave Irvine’s housing market? Without Alt-A, people will not be able to get the loans necessary to support today’s still-inflated prices. Buyers will actually need to qualify for loans based on their real income, and they don’t make that much money. And since many previously Alt-A borrowers have defaulted and are now Subprime, and since Subprime is currently defunct, the buyer pool in Irvine has gotten much, much smaller.

Today’s featured property is a simple story of speculative greed, Alt-A financing and the aftermath of years of irresponsible lending. The buyer used 100% financing and defaulted when prices didn’t go up. IndyMac foreclosed on its first mortgage and wiped out the second. They are now trying to sell the house to recover the value of their first mortgage, and they are over market. The only mystery remaining is how much of their first mortgage they stand to lose.

Tremendous value! Clean, light and bright. Vaulted ceilings. Recessed

lighting. Scraped ceilings. Tile floor throughout. Fireplace with

mantel in living room. Tile roof. Corner lot in quiet family

neighborhood. Close to schools, parks, shopping, freeway. Low HOA. No

Mello Roos!

Isn’t the front yard beautiful? What a value!

I think the kitchen is the 1986 original, too.

The previous owner bought this property on 9/26/2006 which was the approximate peak of Irvine’s market. He used a $552,000 first mortgage a $138,000 second and a $0 downpayment. It looks like he made payments for about a year and gave up. It went back to IndyMac on 6/25/2008. If this property sells for its asking price, and if a 6% commission is paid, IndyMac stands to lose $161,485.

IndyMac may be on crack, but at least they didn’t get Merril-Lynched…

.

How we stop the black panthers? Ronald Reagan cooked up an answer You hear that? What Gil Scott was hearin When our heroes and heroines got hooked on heroin. Crack raised the murder rate in DC and Maryland We invested in that it’s like we got Merril-Lynched And we been hangin from the same tree ever since Sometimes I feel the music is the only medicine So we cook it, cut it, measure it, bag it,sell it The fiends cop it Nowadays they cant tell if that’s that good shit We ain’t sure man Put the CD on your toungue yeah, thats pure man.

From the place where the fathers gone, The mothers is hardly home And the… Gonna lock us up in a…home How the Mexicans say we just tryin to party homes They wanna pack us all in a box like styrofoam

Why are people selling for a loss? Nobody wants to lose money when they sell their house. Many of the sellers we have seen to date put no money down, so they were not losing any money, only their credit score. Lately, I have been seeing more and more sellers who have lost some of their own money. So why are they selling? In the crash of the early 90s many people submerged beneath the debt on their homes. They were unable to sell, and the few that had to sell due to job loss, divorce or other circumstances created the foreclosure problems of the early 90s. However, for as bad as the foreclosures were then, we have already quadrupled the previous peak, and the problem is only getting worse.

I suppose the easy answer to why people are selling is that the owners cannot afford the payments. Many probably still believe real estate is a great investment and all the other kool aid nonsense they believed when they bought the property. Unfortunately, they were unable to hang on long enough to enjoy the benefits of their great purchase. The ones who have capitulated already are the lucky ones in many ways. The disaster is over for them. Now they can go back to living within their means in a rental, and the crushing debt service payments are a distant memory. The owners who have not capitulated yet, the ones who have the means to hang on longer, they are the ones for whom this price collapse will be a major disaster.

Bear markets are self fueling. Once a price decline gains momentum, the “weak hands” are shaken out, and as they are, they sell and drive prices even lower. This puts a new series of owners in distress and creates a downward spiral. The only thing that stops a bear market like this one is capitulation among owners who give up waiting for prices to come back to breakeven, or a new influx of buyers.

Larger numbers of buyers will not enter the market until prices are affordable. This isn’t because it is financially prudent or because people started reading this blog. Once a vicious price decline gets underway, the tightening of credit prevents many buyers from committing financial suicide. Whereas lenders were willing to give anyone $600,000 a few years ago, now they are only willing to give $300,000 to a select few with good jobs and solid credit ratings. The realtor spin about “pent up demand” is complete bull$hit. There is probably a lot of pent up desire for housing, but demand is measured in dollars, and there is a major lack of demand with the absence of lender funds, and a large and growing “pent up supply” of REOs.

I have mentioned a number of times that I believe this fall and winter will see another major leg down in the market. The economic recession will be in full swing. When times are tough and jobs are uncertain, it is not a time when people commit to large purchases like houses. Also, it is becoming increasingly obvious there is strong downward momentum in prices. This is prompting many to put off purchases because prices will be lower later. As the foreclosure problem worsens and more and more loans begin resetting to higher payments, supply will continue to enter the market.

Usually there is a strong seasonal component to inventory. This year we did not get a big inventory spike in the summer. Perhaps it is our “inverted year” and we will see ballooning inventories this fall and winter. There are many REOs that are not listed yet, and these will hit the market eventually. The lenders would have been better served selling them this summer when there was some volume. Now many of these will hit in the fall and winter when few buyers are around. Since this is must-sell inventory, it will push prices lower.

This is a Short Sale. We have begun the process with the seller and the

bank to get your clients in as quickly as possilbe! Bring Offers for

this Highly Upgraded Desireable open floor plan with Hardwood floors,

Gourmet Kitchen, Stainless Appliances, Breakfast Counter & Formal

Dining. THIS HOME WAS UPGRADED AT THE PURCHASE AND STILL SHOWS NEW!!!

Two Car Garage with Direct Access. Enjoy Award Winning Quail Hill

schools and resort style amenities. Minutes away from shopping,

entertainment, restaurants, Irvine Sprectrum, Business area, Hospitals,

Freeways and the Beach!!! Bring your fussiest buyer. Friendly cat not

included…

Lame attempt at humor… Check. (Friendly cat not

included…)

Bogus Clichés… Check. (Highly Upgraded)

This realtor earns an “A” for realtorese.

[adsense-ir}

So what do people do when they actually put a little money down? They start with an asking price that gets their money back.

Listing Price History

Date

Price

Nov 10, 2007

$565,000

May 25, 2008

$500,000

Jul 07, 2008

$450,000

Jul 15, 2008

$430,000

Six months of denial, then two big price drops followed by more market chasing. The asking price is only 20% off the peak, so they will likely have to discount this another 5% to 10% to attract a knife catcher. This will likely bottom between $290,000 and $320,000. It is only two bedrooms, so it may go lower. Only time will tell. Our seller originally paid $536,000 on 5/25/2006. She used a $428,400 first mortgage, a $80,300 HELOC and a $27,300 downpayment. There is no other activity, so the seller is at least out her $27,300 downpayment. It is possible that the HELOC was not tapped for the downpayment, but at some point along the way, it probably was. If this property sells for its asking price, and if a 6% commission is paid, the total loss on the property will be $131,800.

.

Ooh man, dig that crazy chick.

Who wears short shorts We wear short shorts They’re such short shorts We like short shorts Who wears short shorts We wear short shorts.

Who wears short shorts We wear short shorts They’re such short shorts We like short shorts Who wears short shorts We wear short shorts.

Today’s rollback is truly impressive, not because it is a great property or a great deal, but because the discount is so severe. The low end of the market is searching for the bottom, and it hasn’t found it yet. What is also interesting about this property is its cost per square foot. At $174/SF, it is the least expensive place in Irvine. This might be expected on a large property over 3,000 SF, but when you see a price like that on a small condo, it is signaling more declines in the market. Smaller units almost always carry a higher price tag on a per square foot basis. From a construction cost perspective this makes sense because the smaller units still have the expensive bathroom and kitchen space and very little of the inexpensive filler.

The low end of the market must find a bottom before the market can stabilize. Without price stabilization there, the move-up market is non-existent, and the substitution effect will eventually pull down the larger, more desirable properties. Someone looking for a two bedroom place might take a smaller property if the price differential is great enough. Is that second bedroom really worth paying double for? Today’s featured property is probably the least desirable property in Irvine. It is old, small, ugly and in need up renovation (although it is a livable rental.) All premiums can be measured off units at the bottom. Properties in Brio may be superior, but would you pay 80% more ($360,000) for a smaller unit there? (2701 Ladrillo Aisle, Irvine, CA 92606) People looking at 1 bedroom properties will not likely pay an 80% premium no matter how much nicer the property might be. As you can see this will put further price pressures on units in Brio, and this will reverberate through the entire chain of move ups. High-end property prices will not hold up with continued price erosion at the bottom of the market. The high end may continue to be populated by a few knife catchers, but as the substitution effect really kicks in, volume will decline further, and the imbalance of supply and demand will create a fragile market. REOs that find the few remaining buyers will finally overwhelm the feeble price support, and the next leg down will begin. Look for it this fall and winter.

Lowest price for this square footage in the city. Unbeliveable

opportunity to own a spacious two story townhome in Irvine for under

$200,000. Previous owner had an extension built out over the living

area which could very easily be converted to a second bedroom or used

as an office/den. This home needs some work, so bring your paintbrush

and tool box. The patio overlooks a beautiful water scene with an

island and lily pads and is quiet and serene. Lower level has pergo

flooring and a wood burning or gas fireplace. There is a full laundry

room on the patio and the home has central air. There is one covered

parking space but ample unlimited street parking a few steps from the

home. No Mello Roos. Complex has two pools and tennis courts. Located

in Northwood close to award winning schools, stores the 405 and 5

freeways and toll roads. We expect this to sell in days at this price

so hurry. Great for a first time buyer or investor.

Unbeliveable?

I would be very concerned about the unpermitted extension…

Great for a first time buyer or investor? Oh, really? It cost these people their good credit, but at least they took a wad of bank cash with them on the way out.

Check out the sales history. This is a 2003 rollback:

Sales History

Date

Price

Appreciation

May 08, 1996

$90,000

—

Oct 26, 2001

$173,500

12.8%/yr

Apr 11, 2003

$215,000

15.9%/yr

Mar 26, 2004

$295,000

39.1%/yr

This is practically a 2001 rollback. Of course, some excited knife catcher will probably bid over the asking price. This may be near rental parity for an owner occupant, but who wants to own and live here? An investor looking for positive cashflow would still bid less than this asking price.

None of this is a concern to today’s owners of course. They bought the place in 2004 with a $236,000 first mortgage, a $44,250 second mortgage, and a $14,750 downpayment. They refinanced in 2005 with a $284,000 first and a $71,000 second leaving a total property debt of $355,000. They got their downpayment back plus an additional $60,000. If this property sells for its asking price, and if a 6% commission is paid, then Master Financial Inc. stands to lose $167,094. That is almost half of their loan balance. Ouch!

.

Tell me, doctor, where are we going this time Is this the 50’s, or 1999 All I wanted to do – was play my guitar and sing

So take me away, I don’t mind But you’d better promise me, I’ll be back in time Gotta get back in time

Don’t bet your future, on one roll of the dice Better remember, lightning never strikes twice Please don’t drive eighty eight, don’t wanna be late again

So take me away, I don’t mind But you better promise me, I’ll be back in time Gotta get back in time Gotta get back in time Get me back in time

Gotta get back in time Gotta get back in time Get back, get back

Get back Marty

Gotta get back in time Gotta get back in time Get back, get back

Shes a good girl, loves her mam a

Shes a good girl, loves her mam a

Tremendous value! Clean, light and bright. Vaulted ceilings. Recessed

Tremendous value! Clean, light and bright. Vaulted ceilings. Recessed How we stop the black panthers?

How we stop the black panthers?

Ooh man, dig that crazy chick.

Ooh man, dig that crazy chick.

Tell me, doctor, where are we going this time

Tell me, doctor, where are we going this time