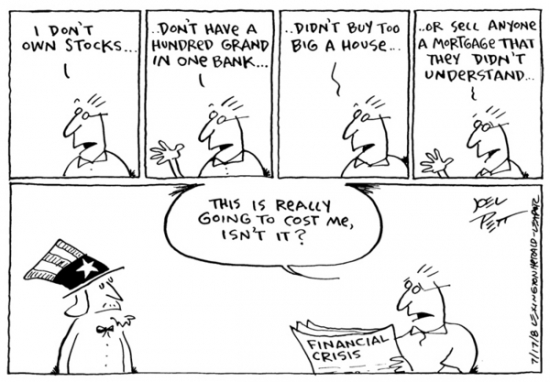

Government policymakers have gone through heroic efforts to save the housing market. The question is: should they?

Irvine Home Address … 20 AVANZARE Irvine, CA 92606

Resale Home Price …… $599,000

There's nothing left to say

But so much left that I don't know

We never had a choice

This world is too much noise

It takes me under

It takes me under once again

Rise Against — Savior

Should US Taxpayers responsible for every underwater homeowner? Many in government act as if they should, and many in the mainstream media report as if the status quo should be preserved.

It's common at housing blogs to find calls for the government to get out of the housing market. It's rare when you find this sentiment coming from a local newspaper editorial in conservative South Carolina.

Should we work to 'save' housing market?

Source: Herald; Rock Hill, S.C.

Publication date: January 5, 2011

By Thomas Sowell

“Housing Market Setback Forecast,” the newspaper headline said. A recently released report on housing says that home sales are down more than 25 percent and the inventory of unsold homes is about 50 percent higher than it was the same time last year.

This is just one of innumerable stories about the woes of the housing market. We all understand about human beings having woes. But how can a housing market have either setbacks or woes? Moreover, why should politicians be riding to the rescue of the housing market with the taxpayers' money?

Investors lost money. Many of them were homeowners who over-indebted themselves to capture appreciation. That's our daily tale of woe. Politicians are riding to the rescue, not to save the crying masses who lost money on their homes, but to save their large campaign backers in the banking industry. The are raping the US taxpayer because they can.

We hear all sorts of sad stories about people whose homes are “under water” or who are facing foreclosure. But why should our attention be arbitrarily focused on these particular people, rather than on the many other people who would benefit from being able to buy those same houses if the prices came down? The government is artificially keeping the prices up with subsidies and with pressures on lenders to accommodate the current occupants.

Can we not walk and chew gum at the same time? Is our attention span so limited that we can only think about one set of people that the media and the politicians have chosen to highlight?

Hasn't that been the story of the housing bubble from the mainstream media? Renters don't exist. Not like real people who own houses. The interests of renters as a group does not capture the attention of anyone in the mainstream media. The story is rarely told from their point of view.

Do other people count for less just because the media don't put their pictures in the paper or on the TV screen? Or because politicians are ignoring them?

Sometimes we are more concerned about some people because they are especially deserving. But this cannot be said about those who borrowed money to buy homes that they could not afford, or who borrowed against the equity in their homes, and now find that what they owe is more than the home is worth.

If anyone is especially deserving, it is those who had the common sense to avoid taking on bigger financial obligations than they could handle, but who are now expected to pay as taxpayers for other people's irresponsibility.

The circumstance that angers me most from the housing bubble is what has been done to the people who were responsible.

No doubt some people who are facing foreclosures might have been able to continue making their mortgage payments if they had not lost their jobs. But since when were we all guaranteed never to lose our jobs? People used to put money aside “for a rainy day.” But now people who have spent like there are no rainy days are supposed to have the taxpayers pay to give them an umbrella.

Why are so few making more noise about this? Think of the message we are sending everyone. Once Uncle Sam commits to bailing out everyone, what incentive is there to be prudent?

What about the people who saved and put their money in a bank? Those who blithely say that the banks ought to modify the mortgage terms to accommodate people who are behind in making their monthly payments forget that, however “rich” a bank may be, most of its money actually belongs to vast numbers of depositors, most of whom are not rich.

Those depositors deserve to get the best return on their money that supply and demand can offer. Why should people who save be sacrificed for the benefit of those who spent more than they could afford?

When the federal reserve lowers interest rates it diverts money to banks that would have gone to savers. Stealing from the prudent for the greater good, right?

Why are politicians so focused on one set of people, at the expense of other people? Because “saving” one set of people increases the chances of getting those people's votes. Letting supply and demand determine what happens in the housing market gets nobody's votes.

If current occupants are put out of their homes and the prices come down to a level where others can afford to buy those homes, nobody will give politicians credit – or, more to the point, their votes. Nor should they.

Rescuing particular people at the expense of other people produces votes. It also produces dependency on government, which is good for politicians, but bad for society.

That is why politicians give what Adam Smith called “a most unnecessary attention” to things that would sort themselves out better and faster without heavy-handed government intervention.

Why do the media fall in with this arbitrary focus on particular people who are having trouble holding on to homes they cannot afford? Partly because it makes a good story and partly because too many people in the media simply go with the politicians' talking points. That is a lot easier than thinking.

But the rest of us have no excuse for not thinking – or for letting ourselves be stampeded by rhetoric about “saving” the housing market.

Thomas Sowell is a senior fellow at the Hoover Institution. His Web site is www.tsowell.com.

Actually, every homeowner in America has a huge incentive to let politicians do whatever is necessary to save them. Willful ignorance will rule the day. It always does.

The fate of sheeple

I am trying to do more posts on different mortgage situations I find in the property records. The HELOC abuse cases are still the most interesting, but they do not tell the full story of the housing bubble.

A sheeple would be a middle of the road borrower: someone who didn't take out the most exotic terms and who put some money down but less than 20%.

Your typical Irvine sheeple borrower at the top of the bubble was more like today's owners. They bought at the wrong time with the wrong financing, and they are losing their home, their equity, and their credit rating. California real estate is not always a pot of gold.

These owners paid $753.000 on 6/5/2005. They used a $602,400 ARM, a $75,300 HELOC, and a $75,300 down payment. Five and a half years later, and the owners are selling short, and the bank is hoping prices haven't dropped more than 20%. The owner doesn't care anymore.

Foreclosure Record

Recording Date: 11/24/2010

Document Type: Notice of Default

Irvine Home Address … 20 AVANZARE Irvine, CA 92606 ![]()

Resale Home Price … $599,000

Home Purchase Price … $753,000

Home Purchase Date …. 6/3/05

Net Gain (Loss) ………. $(189,940)

Percent Change ………. -25.2%

Annual Appreciation … -4.0%

Cost of Ownership

————————————————-

$599,000 ………. Asking Price

$119,800 ………. 20% Down Conventional

4.79% …………… Mortgage Interest Rate

$479,200 ………. 30-Year Mortgage

$121,081 ………. Income Requirement

$2,511 ………. Monthly Mortgage Payment

$519 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$100 ………. Homeowners Insurance

$162 ………. Homeowners Association Fees

============================================

$3,292 ………. Monthly Cash Outlays

-$426 ………. Tax Savings (% of Interest and Property Tax)

-$598 ………. Equity Hidden in Payment

$219 ………. Lost Income to Down Payment (net of taxes)

$75 ………. Maintenance and Replacement Reserves

============================================

$2,562 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$5,990 ………. Furnishing and Move In @1%

$5,990 ………. Closing Costs @1%

$4,792 ………… Interest Points @1% of Loan

$119,800 ………. Down Payment

============================================

$136,572 ………. Total Cash Costs

$39,200 ………… Emergency Cash Reserves

============================================

$175,772 ………. Total Savings Needed

Property Details for 20 AVANZARE Irvine, CA 92606

——————————————————————————

Beds: 4

Baths: 2 full 1 part baths

Home size: 1,876 sq ft

($319 / sq ft)

Lot Size: 2,582 sq ft

Year Built: 1996

Days on Market: 210

Listing Updated: 40543

MLS Number: S622739

Property Type: Single Family, Residential

Community: Westpark

Tract: Trovata (Trov)

——————————————————————————

According to the listing agent, this listing may be a pre-foreclosure or short sale.

Short Sale: Light & bright detached home In desirable Westpark area. This beautiful home has 4 bedrooms, living room, family room & Formal dining room. Kitchen with tile floor, granite counters & breakfast counter. Large master suite w/walk-in closet, shower & large bath tub. Separate laundry room upstairs. Side yard w/patio. Wood floors downstairs, Laminate on stairs/hallway & carpet in bedrooms. Plantation shutters. Washer, dryer & Refrigerator are included. Walking distance to association pool, spa, tennis court & park. Walk to Plaza Vista Elementary school. Very close to shopping center. EZ access to freeway.

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

Have a great weekend,

Irvine Renter

.png)

.jpg)

.jpg)