A series of new studies on borrower behavior shed some light on the motivations behind those who quit paying their mortgages.

Irvine Home Address … 23 FOXHOLLOW Irvine, CA 92614

Resale Home Price …… $319,900

On and on we're charging to the place so many seek

In perfect synchronicity of which so many speak

We feel so close to heaven in this roaring heavy load

And then in sheer abandonment, we shatter and explode.

Judas Priest — Turbo Lover

Strategic default: the abandonment of mortgage and property. A financial explosion.

Most buyers of property were seeking riches from appreciation. They all enjoyed the synchronized movements of the market when everyone was clamoring for more property. Trees don't grow to the sky, and no matter how close prices get to heaven, nirvana is always out of reach.

Strategic Defaults Threaten All Major U.S. Housing Markets

Posted by Keith Jurow 09/30/10 8:00 AM EST

In my last article, we examined the shadow inventory to determine how many distressed properties (not on MLS) were almost certain to be forced onto the market in the not-to-distant future.

For a sensible follow up, let's take an in-depth look at so-called "strategic defaults" to see how many homeowners are likely to "walk away" from their mortgage debt although they might be financially able to continue paying it.

Strategic Default Defined

According to Wikipedia, a strategic default is "the decision by a borrower to stop making payments (i.e., default) on a debt despite having the financial ability to make the payments." This has become the commonly accepted view.

From Accelerated Default: What Strategic Default Really Is: "There is no accepted definition of strategic default. Lenders have tried to define the issue as any borrower who is capable of making a payment and chooses not to. On the surface that sounds reasonable, but that misses a very important distinction. Some people chose to default because they know they can't afford the home and they are merely choosing the timing of the inevitable.

When I think about strategic default, I think about people who chose the timing of their default when there is little reasonable hope of having equity and they are facing escalating payments. The only thing strategic about the default is the timing, not whether or not they will lose the home."

In a recent, thorough study of strategic defaults, an effort was made to narrow its definition even more specifically. The report examining 6.6 million first lien mortgages was published this past April by Morgan Stanley analysts. They considered a default to be strategic only if a borrower went from being current on the debt to 90 days delinquent in consecutive months "without any curing in between or thereafter."

The authors went further and included two other prerequisites. First, the borrower had to be "underwater" on the first lien mortgage. Second, the homeowner had to have an outstanding non-mortgage debt balance of more than $10,000. The purpose of this last requirement was explained to me in a phone conversation with the lead analyst. He clarified that unless the borrower had at least $10,000 in non-mortgage debts which continued to be kept current; it was very likely that the mortgage default was induced by the inability to continue making the payments.

While this definition by the Morgan Stanley analysts is plausible, I consider it to be too narrow. It excludes too many borrowers who choose to stop paying the mortgage even though they may miss payments on some of their other debt obligations. I define a strategic defaulter to be any borrower who goes from never having missed a mortgage payment directly into a 90 day default. We'll examine a graph a little later which clearly illustrates this definition.

This definition is not a bad way to identify people who default by choice, but it doesn't necessarily tell us why they made the choice. Many people who financially implode keep it all together until the reach a breaking point where they capitulate. The only thing we can be sure of about the people Mr. Jarow has singled out is that they were decisive. Once they stopped making payments, they didn't bother to play around with loan modifications or otherwise game the system.

I believe it is important to note that most people chose to default because they know continuing to pay is futile. Just because someone is capable of continuing a futile act doesn't mean that stopping is an irrational decision. In fact, those that acclerate their defaults are far more rational than those who continue to pay when it makes no financial sense for them to do so.

Why Do Homeowners Walk Away from Their Mortgage?

In the midst of the housing bubble, it was inconceivable that a homeowner would voluntarily stop making payments on the mortgage and lapse into default while having the financial means to remain current on the loan.

Then something happened which changed everything. Prices leveled off in 2006 before starting to decline. With certain exceptions, they have been falling ever since around the country. In recent memory, this was something totally new and it has radically altered how homeowners view their house.

In those metros where prices soared the most during the housing bubble and collapsed most severely, many homeowners who have strategically defaulted shared three essential assumptions:

1. The value of their home would not recover to their original purchase price for quite a few years.

2. They could rent a house similar to theirs for considerably less than what they were paying on the mortgage.

3. They could sock away tens of thousands of dollars by stopping mortgage payments before the lender finally got around to foreclosing.

Notice the considerable value lenders obtained by their failure to foreclose. Locally, where house prices are still elevated above reason, people believe house prices will return to peak valuations in a few years and the HELOC party will be back on. Denial keeps people making payments who would ordinarily accelerate their default. Many families in Orange County cannot afford their houses. Many have already defaulted. Few have been foreclosed on so prices remain elevated, and the hopeless maintain denial of a brighter tomorrow.

Put yourself into the mind and the shoes of an underwater homeowner who held these three assumptions. The temptation to default became very difficult to resist. What would you have done?

The author presumes everyone believes accelerated default is wrong. He portrays it as something evil that people are tempted with. It isn't the default that is a tempting evil, it was taking out the loan in the first place. If someone goes out on an all night bender, are they tempted by evil aspirin in the morning? People who accelerate their defaults are merely curing the problem that was created by their earlier mistakes.

Now you may ask: What has kept most underwater homeowners from defaulting?

Why Do Struggling Homeowners Keep Paying Their Mortgages?

This is not an easy question to answer. I suggest that you take a look at a very thorough discussion of this issue in a paper written by Brent White, a professor of law at the University of Arizona and published in February 2010. Its title is "Underwater and Not Walking Away: Shame, Fear and the Social Management of the Social Crisis." He asserts that there are strong societal norms and pressures that lead to feelings of shame, fear and guilt which prevent many underwater homeowners from choosing to default.

He also cites the strong moral condemnation heaped on strategic defaulters by the press as well as by significant political figures. Take the speech given in March 2008 by then Secretary of the Treasury Henry Paulson. Paulson declared on national television: "Let me emphasize, any homeowner who can afford his mortgage payment but chooses to walk away from an underwater property is simply a speculator – and one who is not honoring his obligations." Coming from the former Chairman of a Wall Street firm that earns billions every year by speculating, these words had a certain hollow ring to them.

Strategic Default Is Merely Collecting On Home Price Protection Insurance Sold By Lenders

Walking Away from a Mortgage to Secure Their Children’s Future

Two Key Studies Show that Strategic Defaults Continue to Grow

Within the past six months, two important studies were published which have tried to get a handle on strategic defaults. First came the April report by three Morgan Stanley analysts entitled "Understanding Strategic Defaults." Remember their narrow definition of a strategic defaulter which I described earlier:

1. an underwater homeowner who goes straight from being current on the mortgage to a 90+ day delinquency "without any curing in between or thereafter"

2. has an outstanding non-mortgage debt balance of at least $10,000 which does not become delinquent

The study analyzed 6.5 million anonymous credit reports from TransUnion's enormous database while focusing on first lien mortgages taken out between 2004 and 2007.

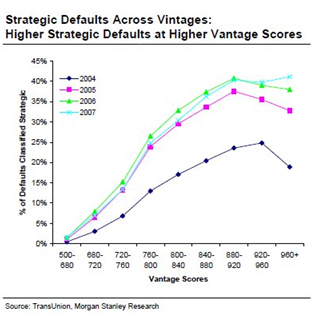

One conclusion which the authors reach is that the percentage of defaults which they label strategic has risen steadily since early 2007. By the end of 2009, 12% of all defaults were strategic. Even more significant is that loans originating in 2007 have a significantly higher proportion of defaults which are strategic than those originated in 2004.

Interesting. It appears that people who have not been in the home as long are more prone to walk away. Are they less attached? Since their values went nowhere but down, did they fail to get a taste of kool aid to keep them hooked?

The following chart clearly shows this difference.

It is also important to note that with higher Vantage credit scores, the strategic default rate rises very sharply. [Vantage scoring was developed jointly by the three credit reporting agencies and now competes with FICO scoring].

Is anyone else surprised that strategice default is more common among people with good credit scores? I guess we really are all subprime now.

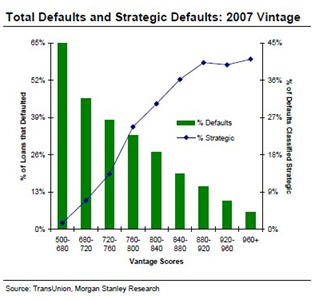

Another Morgan Stanley chart shows us that for loans originated in 2007, the strategic default percentage also climbs with higher credit scores.

Notice that although the percentage of loans which default at each Vantage score level declines, the percentage of defaults which are strategic rises. A fairly safe conclusion to draw from these two charts is that homeowners with high credit scores have less to lose by walking away from their mortgage. The provider of these credit scores, VantageScore Solutions, has reported that the credit score of a homeowner who defaults and ends up in foreclosure falls by an average of 21%. This is probably acceptable for a borrower who can pocket perhaps $40,000 to $60,000 or more by stopping the mortgage payment.

Very interesting data. If you had an 800 FICO score, a strategic default will lower it 160 points to a value of 640. It probably doesn't take long to bring that up enough to qualify for most forms of credit, albeit at a higher rate.

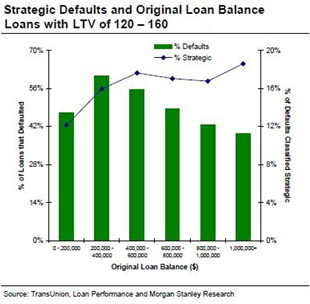

There is one more key chart from the study that is worth looking at. This one looks at strategic default rates for different original loan balances.

Note that the size of the original loan balance has little impact on the strategic default rate.

Rich people and poor people accelerate their defaults at the same rate. I would have guessed that wealthier people would hold out longer by drawing on other sources of credit. Apparently not.

The Key Factor Behind Strategic Defaults

Then what is the decisive factor that causes a strategic default? To answer this, we need to turn to the other recent study.

This past May, a very significant study on strategic defaults was published by the Federal Reserve Board. Entitled "The Depth of Negative Equity and Mortgage Default Decisions," the study was extremely focused in scope. It examined 133,000 non-prime first lien purchase mortgages originated in 2006 in the four bubble states where prices collapsed the most — California, Florida, Nevada and Arizona. All of the loans had 100% financing with no down payment. These loans came to be known as 80/20s – an 80% first lien and a 20% piggy back second lien. It's hard to remember that those deals once flourished.

The first conclusion to note is that an astounding 80% of all these homeowners had defaulted by September 2009.

Anecdotally, I am not surprised by that number. Do you remember back in 2007 and 2008 many of the properties I profiled were 100% financing walkaways. By the end of 2008 and into 2009, we stopped seeing those and we began seeing people who had put 5% to 10% down. It is still rare to see a default where the owner put 20% or more down and there was no HELOC abuse.

Half the defaults occurred in less than 18 months from origination date. During that time, prices had dropped by roughly 20%. By September 2009 when the study's observation period ended, median prices had fallen another 20%.

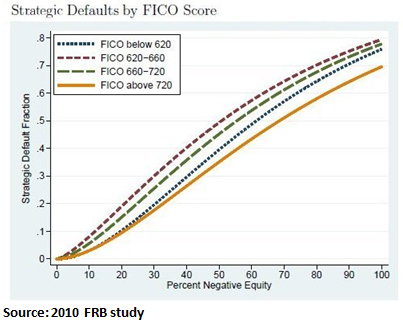

The study really zeroes in on the impact which negative equity has on the decision to walk away from the mortgage. Take a look at this first chart which shows strategic default percentages at different degrees of being underwater.

Notice that the percentage of defaults which are strategic rises steadily as negative equity increases. For example, with FICO scores between 660 and 720, roughly 45% of defaults are strategic when the mortgage amount is 50% more than the value of the home. When the loan is 70% more than the house's value, 60% of the defaults were strategic.

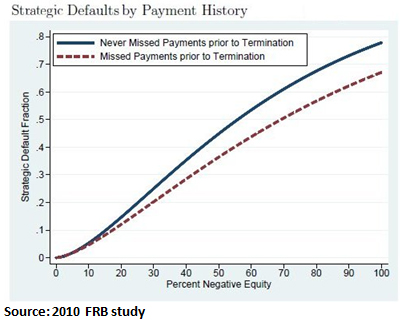

Now take a look at this last chart. It focuses on the impact which negative equity has on strategic defaults based upon whether or not the homeowner missed any mortgage payments prior to defaulting.

This chart shows what I consider to be the best measure of strategic defaulters. It separates defaulting homeowners by whether or not they missed any mortgage payments prior to defaulting. As I see it, a homeowner who suddenly goes from never missing a mortgage payment to defaulting has made a conscious decision to default. The chart reveals that when the mortgage exceeds the home value by 60%, roughly 55% of the defaults are considered to be strategic. For those strategic defaulters who are this far underwater, the benefits of stopping the mortgage payment outweigh the drawbacks (or "costs" as the authors portray it) enough to overcome whatever reservations they might have about walking away.

Intuitively, this makes sense: the further you are underwater, the more hopeless your situation, so you are far more likely to accelerate your default. With deeply underwater homeowners — like anyone who has not defaulted already in Las Vegas — true strategic default becomes much more common. I am sure I would default on my mortgage if I were 50% underwater. Anyone that far underwater is stupid not to default.

Where Do We Go From Here?

The implications of this FRB report are scary. Keep in mind that 80% of the 133,000 no down payment loans examined had gone into default within three years. Clearly, homeowners with no skin in the game have little incentive to continue paying the loan when the property goes further and further underwater.

While many of these 80/20 zero down payment loans have already gone into default, there are still a large number of them originated in 2004-2005 which have not. We know from LoanPerformance that roughly 33% of all the Alt A loans that were securitized in 2004-2006 were 80/20 no down payment deals. Over 20% of all the subprime loans in these mortgage-backed security pools had no down payments. These figures are confirmed by the Liar Loan study which I referred to in a previous article. It found that 28% of the more than 700,000 loans examined in that report which had been originated between 2004 and 2007 were 80/20 no down payment deals.

The problem of strategic defaults goes far beyond those homeowners who put nothing down when they bought their home. Although the Morgan Stanley study found that only 12% of all the defaults observed were homeowners walking away from the mortgage, I think their definition of a strategic defaulter is much too narrow.

The chart from that study which we looked at earlier shows strategic default rates when the loan exceeded the home value by 20-60%. Total default rates were over 40% for mortgages of all sizes. This tells me that a substantial proportion of all these defaults by underwater homeowners were walk-aways.

It is not only the four worst bubble states examined in the FRB study to which these two reports are applicable. Remember, prices have declined by 30% or more in just about all of the 25 large metros that had the highest number of distressed properties which I examined in my previous article on the shadow inventory.

Another chart from the Morgan Stanley study showed that for all the 6.6 million loans analyzed, the percentage of them defaulting rose steadily from 45% for loans with a LTV of 100 to 63% for loans with a LTV of 155. It seems clear from these two reports that as home values continue to decline and LTV ratios rise, the number of homeowners choosing to strategically default and walk away from their mortgage obligation will relentlessly grow. That means real trouble for all major housing markets around the country.

Where we go from here is simple: we foreclose on the squatters and let whatever happens happen. There is no real dilemma here. We just don't want to do what is necessary and endure the pain that goes along with it.

The HELOC Lifestyle

California is the only place in the world where people come to believe they can live on home price appreciation as a reliable source of income. It isn't surprising that real estate takes on a special level of desirability when each house comes with a built-in ATM machine. It becomes obvious that people come to expect and rely on this source of income when you witness them steadily and methodically increasing their mortgage balance.

Of course, since banks allow people to borrow this money and become dependant upon this source of income, houses become desirable beyond all reason. The competition for free money becomes intense, house prices rise, and when the market rally fizzles, prices crash back to earth, and the banks lose billions of dollars.

- The owners of today's featured property paid $175,000 on 3/18/1999. They used a $169,750 first mortgage and a $5,250 down payment.

- On 11/15/2001 they refinanced with a $229,500 first mortgage.

- On 12/4/2002 they refinanced with a $240,000 first mortgage.

- On 2/11/2003 they refinanced with a $278,000 first mortgage.

- On 11/1/2004 they refinanced with a $300,000 first mortgage.

-

On 2/11/2008 they refinanced with a $323,000 first mortgage.

- Total mortgage equity withdrawal was $153,250.

- Total squatting time is about 15 months so far.

Foreclosure Record

Recording Date: 09/14/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 03/24/2010

Document Type: Notice of Rescission

Foreclosure Record

Recording Date: 03/09/2010

Document Type: Notice of Default

Foreclosure Record

Recording Date: 10/30/2009

Document Type: Notice of Default

This is what passes for good mortgage management in California. They tried to live within their means so to speak; they only spent what they perceived to be within the bounds of normal appreciation for their property. Of course, they were wrong, but that is the mindset by which they approached their mortgage management.

Am I the only one who thinks this is crazy?

Irvine Home Address … 23 FOXHOLLOW Irvine, CA 92614 ![]()

Resale Home Price … $319,900

Home Purchase Price … $175,000

Home Purchase Date …. 3/18/1999

Net Gain (Loss) ………. $125,706

Percent Change ………. 71.8%

Annual Appreciation … 5.2%

Cost of Ownership

————————————————-

$319,900 ………. Asking Price

$11,197 ………. 3.5% Down FHA Financing

4.74% …………… Mortgage Interest Rate

$308,704 ………. 30-Year Mortgage

$64,292 ………. Income Requirement

$1,608 ………. Monthly Mortgage Payment

$277 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$27 ………. Homeowners Insurance

$340 ………. Homeowners Association Fees

============================================

$2,252 ………. Monthly Cash Outlays

-$150 ………. Tax Savings (% of Interest and Property Tax)

-$389 ………. Equity Hidden in Payment

$20 ………. Lost Income to Down Payment (net of taxes)

$40 ………. Maintenance and Replacement Reserves

============================================

$1,774 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$3,199 ………. Furnishing and Move In @1%

$3,199 ………. Closing Costs @1%

$3,087 ………… Interest Points @1% of Loan

$11,197 ………. Down Payment

============================================

$20,682 ………. Total Cash Costs

$27,100 ………… Emergency Cash Reserves

============================================

$47,782 ………. Total Savings Needed

Property Details for 23 FOXHOLLOW Irvine, CA 92614

——————————————————————————

Beds: 3

Baths: 1 full 1 part baths

Home size: 1,300 sq ft

($246 / sq ft)

Lot Size: n/a

Year Built: 1985

Days on Market: 17

Listing Updated: 40443

MLS Number: S632715

Property Type: Condominium, Residential

Community: Woodbridge

Tract: St

——————————————————————————

According to the listing agent, this listing may be a pre-foreclosure or short sale.

Desirable 3 bedroom two story condominium in the Somerset Tract near an amazing and tranquil rest and park area, Green Belt and Pool. This perfect starter home includes super upgraded laminate and travertine floors. Kitchen has gas stove and stainless steel sink. Crown moulding and 3 inch baseboards grace each of the rooms, along with custom paint, smooth ceilings, and textured walls. For your comfort, home also features an oversized five year old air conditioner. Bathrooms feature new light fixtures. Living Room is showcased with a slate Fireplace and beautiful French Doors that open on to the Patio with an 8 year old fruit bearing guava tree. Enjoy all the Woodbridge area amenities, including the Lakes, Pools, Parks, Schools and Shopping. This home is lovingly maintained by this family and not a short sale fixer upper.

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

Have a great weekend,

Irvine Renter

To interpret the word “futile” here one needs to make some kind of assumption of what the mortgage payment is meant to achieve. If you believe that mortgage payments are made to extinguish the lender’s lien on the property that you own, then continuing to make the payments is not futile as when the payments are completed, the lien will be released. The borrower will enjoy the precise house they elected to buy free of any liens. Where is the futility in that? I suppose that if you rather believe that the purpose of the mortgage is to provide leverage for a strongly appreciating and reasonably liquid capital investment, then under the circumstances continuing to make payments could be viewed as futile. But if that is the case, why would anyone get snippy over the implication that the borrower is a speculator – whether made by a fabulously wealthy individual or anyone else?

Yes, but if you have $100k of negative equity, you just stop paying and, a few years later, when you get kicked out, you leave and buy a similar place for that $100k less. Now you have even lower payments and got 2 years of free rent.

The problem is that it is in you financial best interest to stop paying.

Is your argument that actions that may have results that are not in your best financial interest are de facto futile?

“The borrower will enjoy the precise house they elected to buy free of any liens.”

In California, the county has a forever lien on the county property via taxation.

The day when they get rid of Prop 13 is the day when long term property owners will be worried (not that 1.something percent is not killing them already along with Mello Roos).

Who is “they”? Prop 13 is a Constitutional amendment. Prop 13 is to the California legislature what Social Security is to the US Congress. Ha ha liberals, just try to steal from the seniors!

Then again, all the dumb bunnies in California bypass Prop 13 every time they vote for bonds. Dumb, dumb, dumb! Want to increase your property taxes despite a Constitutional amendment against it?

Yes please!

Californians are idiots.

I’ve heard that only 35% of Las Vegas homes are owner occupied.

Sounds like a booming economic opportunity. 65% of Las Vegas homes are vacant or rented. Looks promising for the future of Las Vegas. Brains and upper class families abound.

I’m not a big fan of Planet Reality… But he does have a point about the risks of Vegas landlording.

http://www.lasvegassun.com/news/2010/oct/07/man-late-rent-accused-arson-damage-100000/

If Vegas was a game of SimCity, a winning game strategy would be to bulldoze 1/3 of it to get it back to a manageable and sustainable size.

Of course I wouldn’t get too high and mighty about the quality of Irvine residents… At some point the squatters, and rental units that are only rentals because the owners can’t sell them are going to put a tarnish on the gold standard that is Irvine.

You may not be a big fan of me but I have been right.

Next week I will be cashing in some of the long interest rate positions I took on early last year at a 25%+ return. I won’t cash most out since quantitative easing is set to push rates to my prediction: record low tbills and 3.5-4% mortgage rates.

Irvine Remter has always said LV is a great opportunity because former owners need a place to live and will need to rent. When 65% of former owners are vacant houses, banks, landlords and renters,, well it’s a great fantasy. Maybe new jobs will create renters, time to buy LV.

The sad thing is, you could both be right. If interest rates fall to 3%, how much is rent to cover loan costs of 50,000? How much is rent to attain positive cash flow?

Probably not much at all. So the economy can tank, LV turns to even more low income jobs and almost homeless government sponsored renters, Irvine becomes a premium asian immigrant community(the new Hoag Hospital left out Floor #4 because of chinese superstition!!!)

That’s HOAG Hospital, you know, like Newport Beach, like money, like the upper 1% of the nations wealth.

I think IR has a really good chance to make good investment here, after all, if the market collapses again, you will always own the damn house. Risk everywhere, and PR CONGRATS on making 25% return, holy sheet, you should manage my deferred comp portfolio…where should I invest all my empty beer cans I’m acquiring?

The more people who believe Las Vegas is Detroit, the less competition I face to acquire the properties I want. Market despair is a classic sign of a market bottom. The best deals go to those who buy based on reason when others are selling based on emotion.

Prices in Las Vegas have rolled back to the 90s. At auction, I am obtaining property at late 80s early 90s prices which are below replacement costs. If everyone recognized the value I am obtaining, I would face more competition, prices would go up, and the deals would not be so compelling.

I am thrilled that naysayers come post here. It demonstrates market despair better than any explanation I can give. Like the many others who have come to this blog and told me that I am wrong, their foolish comments will remain long after the market reveals their folly and they disappear from embarrassment. In the meantime, I will continue to pick up Las Vegas flips with 15% to 20% net margins and buy-and-hold cashflow properties with 8% to 10% capitalization rates. I hope the despair continues. It is the only reason the deals are so good.

Or I could simply be right yet again.

PR Dont worry about being right or wrong. Just the fact that IR is buying as an unskilled out of state investor with his business plan based on this being the bottom for Vegas speaks volumes. I wonder how his investors are going to feel in a few months when the cash flow just does not materialize. All its going to take is a few renters going Agro on his homes or the downturn getting deeper still. Then he is going to need more investors to cover the ones he needs to pay.

See where this is heading ? Its a slippery slope

of typical RE Greed. Hopefully he is aware as are his investors that this is a VERY risky investment. Personally I want to just preserve my cash. Not throw it away on a Vegas gambling trip.

Can you say Knife Catching at its finest?

Hope he likes driving to Vegas all the time. Or adding some unsupervised Nevada employees.

How do you….it might just work out for him. Thats the risk he is willing to take and you aren’t so why do you care?

IR, I just don’t get your reasoning on LV. You claim to base your decision on reason instead of emotion, but what reasoning do you use? What facts are you basing your decision on?

If you flip a few places and make money, then good for you, seriously. I’m glad you have the ability and determination to pull that off; that’s the American entrepreneurial spirit!

Regarding your buy and hold properties, I still don’t see how Vegas is going to get any better any time soon. Is LV really at the bottom just because prices are at 90s levels? Are there any surefire signs that prices will not go significantly lower? What industry does LV have that will bring job growth in the near term, or even long term?

I’m not a naysayer because of some emotional attachment to Las Vegas; I’m trying to look at the facts with an open mind. I’m even inclined to believe that Vegas is even more vulnerable to another big leg down than Irvine.

lowrydr310,

I have written several posts on why I believe in Las Vegas. I have clearly laid out my reasoning for buying property there. I will probably do another one in the coming weeks.

Las Vegas does not need to get better any time soon. I am not buying these properties for appreciation. I am buying them either for their current flip spreads or their current cashflow.

If there were surefire signs the prices would not go lower, everyone would buy there and prices would go higher. It is the despair in the market and the (incorrect) perception of risk that keeps people from buying and creates the opportunity for me to buy.

Las Vegas is a gaming town. When the national economy improves, people will travel to Las Vegas and leave money there. Las Vegas is not Detroit.

With as low as prices already are in Las Vegas, it is unlikely that the low end properties will take another leg down. I am not the only one who is able to compute a rate of return and see that investing in these properties makes much more sense than speculating in Orange County real estate. It is investors like me that will form a bottom in Las Vegas by purchasing properties with great positive cashflow for below replacement cots.

Another month comes and goes in Las Vegas.

http://www.lasvegassun.com/news/2010/oct/08/home-sales-prices-tumble-september-inventory-rises/

The gold standard is right.

You need to hitch that wagon to the right horse.

There’s a line of FCBs a mile long, loaded with cash on the sidelines just waiting to buy in Irvine.

Protip: When mocking the contrast between Vegas and Irvine, you should pick a characteristic of Irvine that Vegas lacks, instead of two quantities notably lacking in both.

Wow, thank you for insulting me as I was an Irvine residence from ’01 til ’04 and have worked in Silicon Valley high tech companies (including a biggie there) for more than 18 years.

I guess all the products coming out of Silicon Valley are craps to you. Why are you using the internet to post this message? Oh shoot…I forgot…internet was a DARPA invention. Silly me again.

You think that my statement declaring brains to be lacking in Irvine – hyperbolic, I admit – means that you, personally, are a doofus?

Chip on shoulder much? Get in bar fights much?

High paying families in Irvine scored a few hundred points higher than you on the college boards, but compared to Las Vegas, LV is special ed.

Yet so many of these Irvine geniuses are in hock to the tune of 5x-6x their earnings. Maybe there aren’t so many brilliant folks in Irvine, or maybe the SATs need to be reconfigured into three segments: “verbal”, “mathematical”, and “not going into debt for quadruple your household income”.

As for scores: they didn’t beat me by more than 150 points, I’ll wager, unless 1600 is no longer the top. And my personal income is 40% higher than the median household income in Irvine, while my personal debt is $0.

If you think that SATs & PhDs are the bedrock on which high home prices are built, you should vacate Irvine in favor of Albuquerque. Albuquerque prices don’t have much further to drop, even in the residential areas thick with PhDs.

If the banks or Feds forgive prinicple I would like to know where my $80-200K is for being a prudent owner and renter?

Where is the money for the prudent?? The moral hazzard here is simply mind-boggling!

The SoCal housing market is so broken that it will take a decade or more to normalize, and by normalize I mean a return to fundamentals of income and expense. I see a slow grind for as far as we care to imagine.

You all realize that even if all people owned their house outright most won’t be able to pay the property taxes and basic expenses with a $1,200 / month SS check and their $90K in total savings in their IRA (which they will have to pay tax on)!! Trouble!!!

My .02

BD

Your $80K-$200K as a renter will be realized in a few more years when prices are reasonable in Irvine.

This is true but, if they are taking money from the productive to give to the irresponsible I am mad. Oh wait, this is what our government does now… pick winners and loosers based on ‘need’. Since, they need it more you and I have to pay the price.

Unbelievable.

BD

even as a current renter, I don’t have a huge problem with mortgage forgiveness, and it seems now that some home “owners” might finally be finding a technicality to get mortgage balance erased. http://articles.moneycentral.msn.com/Banking/HomeFinancing/weston-what-the-foreclosure-fiasco-means.aspx

What I really care about is how will mortgage forgiveness will affect my ability to afford a home (condo, SFR…etc.). I suppose less supply means higher prices but there might be other factors related to the economy as a whole.

With $1200/mo in SS check, that comes out to $14400/yr. Standard IRS deduction is about $11000 for married filed jointly (assuming hubby and wifey with no children during retirement). With the additional 2 deductions of about $4k each, you’re looking at a total whack of $19000 per year from AGI.

I would move some of that 90k from taxable IRA to Roth per year (say about 10k/year) while only using the passive income from total IRA combined. After 9 years, the couple should be completely tax free. Furthermore, each year, the taxes that they will have to pay is a minuscule hundreds of dollars because of the IRA conversion and passive income from taxable IRA.

Trouble??? I don’t see it.

Bank of America halts foreclosure sales in 50 states

http://www.latimes.com/business/la-fiw-bank-of-america-foreclosures-20101008,0,3527580.story

Everyone quick, get an FHA Loan with B of A and you never have to pay your mortgage! Strategically default and squat. Talk about cheap living, unbelievable. Please say it’s not true. Maybe renters should get together and declare a moratorium on paying their rent, they can’t possibly evict hundreds of thousands of renters all at once.

Shevy

TIC could care less. They would bulldoze the building after they evicted us just to show their arrogance.

bltserv– good point, probably won’t work with The Irvine Company. However, there are plenty of shady landlords out there that aren’t paying their mortgage and are collecting rent from people whose taxes are being used to artificially prop up the price of the home they want to buy and allowing the landlord to “own” the property for months if not years after they quit paying. Moreover, plenty of active leases with this scenario, one has to make an effort to make sure they are not leasing this type of property these days.

Does anyone notice the foreclosure halts by banks COINCIDE with the peak of Option ARMs reset/recast chart for this year (see the Credit Swiss reset chart)

Is this another tactic (excuse, lie) that big banks is delaying the foreclosure storm (not having to write down… mark to fantasy…) that is going on right now, and waiting for either economy getting better, house price going up, or govt. bailout?

If I remember correctly from the Credit Swiss chart, this Sept./Oct. is the first big peak in reset/recast since late summer of ’08 which everyone knows what happened in the fall ’08.

Appreciate any thoughts!

and the elections. Even though this is made to look like they’re coming down on the banks I highly doubt it. The banks are feeding some major money into some campaigns. Supply was getting too high, prices were getting soft. That can’t happen, it may hurt bank execs bonuses and incumbents.

Regarding the Credit Swiss chart, with all of the mods and how low rates have gotten, I would guess the accuracy is relatively poor now. Does anyone know or have the best most up to date chart? If there is one, I’m guessing it will leave now doubt how far the can has been kicked.

I think the coincidence in time between the moratorium and the lull in the selling season is also important. All of today’s foreclosures are fall and winter MLS sales. The inventory is already bloated, and there are fewer buyers. Any delay helps the banks manage current for-sale inventories.

It’s a win win for BoA. This way they look like the good guys, and manage to extend and pretend on home prices.

According to my source B of A foreclosed on 8 properties today at the court house in Santa Ana, however, that the volume overall is way down. I have not had time to read the details of their moratorium. In addition, First American Title rep told me that his contact at First American told me this afternoon that they believe it’s politically driven.

I’m guessing you saw last night’s Daily Show about how the Mortgage Bankers Ass’n strategically defaulted on its $78M office building in D.C. and rented a similar office 5 blocks away. Wyatt Cenac went to town on that. It was hilarious.

I’ve heard about that but I missed it. Wife had softball.If that does not send a message.

The large scale forclosure moratorium will likely be the catalyst for a surge in ‘strategic defalults’. All of the people on the fringes with a negative equity position will likely use this ban on foreclosures as the final catalyst to ‘walk away’. They already were in limbo thinking about the best financial decision for their family and future.

I’ll bet this is the catalyst. Wait 3 months and we will see a surge in deliquincies….

What do you all think? IR?

My .02

BD

I agree BD, an increase in strategic defaults for sure. CA AG Brown justed now joined the chorus and called on banks to halt foreclosures in CA. And lawsuits will be coming in droves from investors in CDOs to recover CDO losses from the banks. Lawyers and squatters win. Again.

Yep… this moratorium decision just put another year of slow grind lower in pricing for SoCal. I’m now thinking 2013/14 for bottom on the nice stuff- $800K+

Thuoghts?

BD

This type of thing is really hard to project especially with all of the interference, however, we had an up cycle of circa 7 years that was larger than any real estate bubble we have ever seen that ended in 2007, a 7-9 year down cycle without any messing with it was likely. With all of the games, who knows, we can start the clock adding days after B of A’s announcement.

There is no free lunch. If there is another widespread moratorium that goes on for any length of time, strategic default will become the norm. Why would anyone continue to pay their mortgage when they can default and keep the house?

And conversely. Why would anyone attempt to buy a Foreclosed Property while the title could end up being in dispute at a later date. The entire Title Insurance business will freeze behind this news. The “Perfect Storm” is really setting up nicely for the next leg down.

Old Republic has already stated that it will not issue title insurance on properties forclosed upon by certain servicers/lenders. I suspect they are just the first and won’t be the last.

Not sure I would touch a foreclosed property at this point. Especially not a property that I can’t get title insurance on.

I’m sure the vast majority of foreclosures with bogus paperwork are real in one respect, the loan owners stopped paying on the loan. But what is going to screw the title insurers or the buyers is if the chain of title is suspect. If GMAC sells the foreclosure, but some CDO buyer still has fractional rights to the property, how will that end up playing out?

This is a great point. Title insurance reaction will be key.

Yeah, those clear chain of title issues caused by all the forged paperwork & MERS irregularities are frankly scaring the crap out of me – the shadow market inventory & related issues were bad enough but all the fraud discovered & discussed last week (good example here, many more available) seem to increase the problem’s severity by an order of magnitude at the least. Who would knowingly buy a foreclosed house w/a faulty title? Even having title insurance is no guarantee, the title insurance companies have armies of lawyers to ensure the title insurance companies come out ahead. Yves @ Naked Capitalism had a good article here about “Wells Fargo dumping title risk on hapless buyers via a new addendum imposed on buyers shortly before closing”

IR, I really hope you are able to get clear title to the houses you are hoping to by in Las Vegas. Is this title defect something you are planning to write about? I for one would like to read it!

How many foreclosures did they stop? What was the average loan? How many more foreclosures will this encourage? Who is going to pay for this?

Housing prices in costal SoCal – soon to be the greatest slow motion train wreck in history.

Why anyone would continue to may on a mortgage that will be as underwater as those in coastal CA regardless of their personal ability to do so is anyone’s guess – but, I suggest hope for a rebound is not a sound strategy.

Massive ‘strategic defaults’ of expensive coastal CA RE is on its way…

http://seekingalpha.com/article/228961-where-is-the-foreclosure-mess-leading?source=hp_wc

…just my .02 but, people that paid $2M for something that is now worth $1.2 will walk…

If you were wealthy and were down a half-million plus wouldn’t you walk? Who cares about a hit to your credit when you can pay cash! And I’d rather pay the tax on these phantom earnings than eat the whole thing…

Slow motion train wreck – now arriving all over coastal OC.

BD

Not all states, and not all loans are no-recourse. If you are wealthy, and have a recourse loan, walking away from a loan is not the end of the story. Or at least I hope it is not.

Very true… let’s all hope they are foced to take their losses or stick it out.

We should all be looking at housing as a house, and an investment that pays us back over 30 years by providing a great place to live and some forced savings.

All other dreams are just that. I would like to buy now but, I keep thinking I could move in 10 years and if interest rates rise by only a couple or three points then purchasing power will drop by 30% (10% for every point on a 30 year fixed).

I can imagine owning a place for 10 years only to sell and find out that after I pay a 6% sales commision I’m either under water or break even.

Why take the risk? The tax deduction is BS… most will pay that much annualy for upkeep and HOA fees … or some of us get the deduction thrown out all together with AMT.

This is most certainly true for ‘high end’ properties.

I still think – “Timber”! The stuff we all want has the most to fall…

I’ll keep watching the wreck…

My .02

BD

1-? 2-? 3-? 4-responsible homeowners & low to middle income taxpayers.

Have you ever seen a building collapse? When the top floors go the rest gets compressed down. This is no different for housing prices.

If / When the high end of housing begins to fall it will compress values for everything below it…

Why pay 300 dollars a square foot for a condo in HB when you can pay 220 dollars a square foot for a much bigger SFV? This will happen because the higher priced properties – in general – require so much more in carrying costs.

This will also happen because, once we emerge from artifically low rates (either by choice or force from the international debt buyers)carrying costs will rise.

Why do you think Fletcher Jones and other luxury car sellers only advertise monthly payments? The “rich” apparently aren’t that rich in OC… they pay with borrowed money like everyone else.

Just my .02

BD