Last night due to a technical problem at 10:50, I lost today's post. I last successfully saved the basic infrastructure of a post, but the analysis of the CEOs comments — something I spent two hours writing — was gone.

For a moment, I was in total shock. I could believe what happened. After a few unsuccessful attempts at recovery, I conceded defeat, and I was devastated. The sense of loss was powerful and jolting. Then the reality of staying up late to re-write the post set in, and I was just devastated (and pissed). I sought out my wife to calm down.

I didn't realize how important it was to me to put up a daily post (weekdays anyway). I felt like an injured Brett Favre who wanted to start if for no other reason than he always started. Some guys are just built that way. I calmed down, wrote this pep talk to myself, drank my coffee, and hunkered down to rewrite it all. Reliability trumps sleep.

In the comments of that post, one of the astute observers expressed concerns over what looks like an unhealthy obsession. I appreciate the concern, but I can assure everyone that I am doing well.

The experience has caused me to re-evaluate how much time I am spending on the blog, and for a variety of reasons, I am going to stop doing full-blown posts on Saturdays. I may still write stuff for fun, but I will not be creating regular real estate related posts.

The IHB is a workplace blog. People tend to read the IHB in the mornings on weekdays. That is when our daily traffic peaks. On the weekends, traffic typically drops off 30% irrespective of the weekend content.

The primary reason I am stopping weekend posts is purely selfish. I am not willing to give up my Friday evenings any more.

The IHB as personal discipline and nourishment

The main reason I was so driven to get the post out this week after my technical disaster is because I value what the IHB has done for me, and I want to continue that. I was not motivated out of obligation or the desire to please the readership. I was motivated by purely personal reasons to maintain a discipline that nourishes me mentally and emotionally.

All self esteem comes from self discipline. You are your habits. I am proud of my achievement each day I put out a post, and I enjoy the mental challenge of doing it. Whether my business dealings leave me feeling up or down, I know that when I write a post, I will be left feeling energized and renewed. The IHB is not a burden for me. In fact, it has become an integral part of the series of accomplishments that provide self confidence to deal with the challenges of life.

Perhaps I am a bit too driven at times. Anyone who has developed a special skill did so because they have a passion for whatever it is that they mastered. When passion is the driving force behind any activity, it can be uplifting rather than depleting. The real balance is to make sure that pursuing the uplifting activity isn't taking away from other areas of life. The nourishment of the IHB has been taking away from the greater nourishment of spending time with my family on Friday evenings. Therefore, I am only going to write weekend posts if I am inspired.

Shevy has been preparing to write some weekend posts. We were going to have him write on Sundays because it was the only open day. Perhaps he will step up to fill the void I am leaving behind.

Thank you for reading my weekend drivel, and thank you for your understanding.

My strongest feelings of home still reside in my home town in central Wisconsin. It's not a place I can indulge my entitlements, so I find myself wandering the globe looking for a place I can have the closeness of community and the conveniences of modern society. Irvine is as close as I have come.

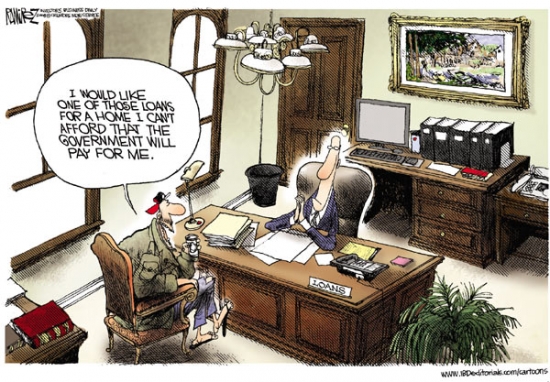

For many, if not most, a sense of community starts with buying a home. The ability of Americans to buy homes depends on their ability to obtain mortgages. The future of home lending is being debated in Washington now, and the future prices of homes could be greatly impacted by the outcome.

… Let’s turn back the clock for a moment to the second half of 2006. At that time, firms and people around the world held a wide array of financial assets that were ultimately backed by U.S. residential land. (Think, for example, of mortgage-backed securities or any asset backed by mortgage-backed securities.) They viewed those assets as being largely free of risk. Investors may have understood that a fall in the value of U.S. land would impose large losses on them. However, they put low odds on such a decline taking place. Rather, they seemed to believe that U.S. land prices would continue to rise at a steady clip.

By the second half of 2007, that belief began to unravel in the face of incoming data. People were beginning to learn the hard way that U.S. land was a risky investment. Now the only question was how risky. The uncertainty about the answer to this question planted the seeds for a global financial panic.

What do I mean by the term “financial panic”? Financial panics are events that blur the line between liquidity and solvency. A firm is solvent if its revenues (in a discounted present value sense) exceed its expenditures. A firm is liquid if it is able to raise enough funds—either by borrowing or by selling assets—to pay its current costs. In a well-functioning financial market, solvent firms are typically liquid, because they are able to borrow against their future profits. In contrast, in a financial panic, lenders feel unable to assess the future profits and/or collateral of borrowers. Borrowing becomes highly constrained, and even highly solvent firms may become illiquid.

The dilemma for lenders during a panic is to determine who is solvent and who is not, that's why all the liquidity dries up. No lender wants to pour money down a black hole.

Lending is sometimes characterized as a confidence game: if lenders all believed firms were solvent, they would be solvent because even the unsustainable Ponzi ventures would be sustained by more borrowed money.

Lending is a confidence game with regard to solvent institutions. When lenders lose the ability to discern between those who are insolvent and those who are not, they stop all lending: a credit crunch.

The federal reserve and the US Government came up with a solution. By declaring insolvent institutions solvent by decree, government makes some firms too big to fail, and it makes the US taxpayer responsible for plugging a hole in our economy that threatens to bring down our banking system.

During the mid-2000s, many forms of collateral around the world were either implicitly or explicitly backed by U.S. residential land. As I’ve described, beginning in mid-2007, it started to become clear that this asset had more risk than financial markets had originally appreciated. It was not clear, though, how much more risk was involved. As a result, financial markets became increasingly uncertain about how to evaluate assets backed by U.S. land. That uncertainty translated into uncertainty about the ultimate solvency of institutions holding those assets—and the ultimate solvency of any of those institutions’ creditors.

Here is where the confidence game interpretation becomes dangerous. This banker is describing this situation as if land is really worth what people were paying in 2006, and if the confidence game had not been disrupted, prices would still be there. That isn't reality.

The reason financial markets ware unsure how to value mortgage-backed securities is because the value of the house was grossly distorted by the financial products of the bubble. With the air abruptly removed from mortgage balances, prices were destined to fall.

As investors became more concerned about the quality of mortgage loans, the secondary market for private-label mortgage-backed securities nearly disappeared. As a result, about 90 percent of mortgages originated over the past two years were guaranteed by government-controlled entities such as Freddie Mac, Fannie Mae, the Federal Housing Authority, or the Veterans Administration. Investors are willing to purchase mortgages and mortgage-backed securities from these agencies mainly because they have faith that the federal government stands behind those instruments.

The only reason private investors are paying prices that permit 5% interest rates is due to the government backing. If investors had to price risk into the market, as they do with jumbo loans, interest rates would be significantly higher.

This heavy reliance on government guarantees is not a sound long-term strategy. Over time, our country needs a mortgage market that returns to greater reliance on private risk-taking and private risk assessment, along with the enhanced regulatory oversight that is already in place. And, in fact, discussions are currently taking place on suitable options for bringing more private capital back into the mortgage market.

Even more generally, I believe that as a country, we need to take this opportunity to rethink many aspects of our public policy programs in the context of housing finance. Home ownership has long been part of the American dream, in no little part because home owners have invested not just in their houses but in their communities. But, through the mortgage interest tax deduction and other programs, we are encouraging people to buy homes by taking on debt—and sometimes large amounts of debt. If we truly want to encourage home ownership, we should contemplate programs that provide incentives for individuals to save and become equity holders in their homes—and, by extension, in their communities….

Are loan owners equity holders in their communities?

The argument used by policymakers for a wide range of government home-ownership assistance programs is home ownership quiets social unrest. People don't riot in a community they feel a connection with.

At some level, there is truth to the idea that people with a feeling of ownership take better care of things. Does owning a home create a feeling civic pride?

Let's assume that it does. The effect may be small, but civic pride is emotionally satisfying, and it tends to get incumbents elected to office, so policies that promote civic pride are favored by government.

What is truly important for civic pride? Does the manner in which a house is occupied have a major impact on civic pride?

If fee-simple title holder with no mortgage encumbrance — a true home owner — feels civic pride as an extension of their ownership, it is likely that mortgage holders also feel this pride in home ownership and community even though their actual ownership claim to real estate (equity) may be very small. The feeling of ownership is only loosely tied to a claim to an asset of tangible value.

In the case of underwater home owners, their claim to real estate has no current liquidation value. For their own personal balance sheets, the property still has option value — their position may have liquidation value again in the future if prices go back up and they have equity again. This option value is the dangling carrot of hope that keeps debtors on the hamster wheel to service the debt. When debtors lose this hope, they strategically default.

The lending line of support in Irvine has been holding median mortgage balances in a tight range since the credit crunch in late 2007. That level of lending is holding the median sales price about 20% below the peak. At that price level, peak buyers are right on the cusp of going underwater.

Once prices drop below the previous median loan peak, the cascade effect of strategic defaults pounds market prices back to the stone ages. This is the lending cartel's greatest fear. Based on the tendency to strategically default, I deduce that loan owners do not have a deep bond with the community at large — or at least not a bond that prompts them to take one for the team.

What about renters?

As a renter, I often ask myself what my connection to the community really is. Like loan owners, I have no equity stake in Irvine real estate. And like a loan owner's option value, I have an intangible freedom value they do not enjoy.

I feel as part of the community as anyone. Being the writer of this blog for four years, I have woven myself into the local fabric. I recently moved to Woodbury, and I feel very comfortable and at-home here. As a renter, I can attest to the possibility of renters for community involvement and a feeling of belonging.

Home ownership does not define one's sense of community.

They waited until the equity was gone, then they foreclosed

When banks stopped processing all mortgage delinquencies as they happened in early 2008, they had to establish buckets of similar loans and determine what to do with them.

One such bucket is composed of properties where the mortgage holder is delinquent, but they still have significant equity. Lenders have no urgency to foreclose on this group because as long as their is equity, they can foreclose whenever they want and still get paid in full. In fact, since they profit on all the fees and late charges, they have incentive to drag the process out until the loan balance is large enough to consume all equity.

That is what the lender did on today's featured property.

The property was purchased on 4/23/2004 for $900,000. The owner overpaid using a $595,000 first mortgage and a $305,000 down payment. Savvy cash buyer, right?

On 6/29/2004 she got a $100,000 HELOC, but it doesn't appear to have been used. On 12/27/2005 she obtained a $55,000 stand-alone second.

By late 2005, this property only had $650,000 in debt, and at the time, it was likely worth much more than that. In late 2007 or early 2008, she went delinquent on the first mortgage.

Foreclosure Record

Recording Date: 04/22/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 08/28/2008

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 05/08/2008

Document Type: Notice of Default

Wells Fargo was the loan servicer, and they foreclosed on 12/7/2010 for $713,932 — the outstanding balance on the first mortgage.

During the time this debtor was delinquent, the loan went from less than $600,000 to more than $700,000. The lender let them squat until their equity ran out, then they foreclosed.

-$798 ………. Tax Savings (% of Interest and Property Tax)

-$772 ………. Equity Hidden in Payment (Amortization)

$289 ………. Lost Income to Down Payment (net of taxes)

$195 ………. Maintenance and Replacement Reserves

============================================

$3,166 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$7,799 ………. Furnishing and Move In @1%

$7,799 ………. Closing Costs @1%

$6,239 ………… Interest Points @1% of Loan

$155,980 ………. Down Payment

============================================

$177,817 ………. Total Cash Costs

$48,500 ………… Emergency Cash Reserves

============================================

$226,317 ………. Total Savings Needed

Property Details for 14 FREEDOM Pl Irvine, CA 92602

——————————————————————————

Beds: 5

Baths: 3

Sq. Ft.: 2550

$306/SF

Property Type: Residential, Single Family

Style: Two Level, Traditional

Year Built: 2000

Community: 0

County: Orange

MLS#: P772387

Source: SoCalMLS

Status: Active

On Redfin: 31 days

——————————————————————————

Bank Repo! Fresh interior two tone paint and new carpet. Beautiful 5 br 3 ba pool home value priced for quick sale! Spacious living room, dining area, separate family room with granite fireplace and plantation shutters, open & bright kitchen with granite counters and center island, gorgeous distressed hardwood floors throughout, one bedroom and bath downstairs, master suite with granite tile floor master bath, dual sink vanity, separate tub and shower, tile roof. Super motivated seller. Submit!!!

He's back. And this time, the forces of light and goodness will prevail, right?

And now, Soylent Green Is People

(And my cartoons. None of the artwork in this post or any other is mine, and some of the cartoons are direct reproductions. My “cartooning” is limited to some limited photoshop work and the use of additional text generally in Comic Sans font.).

The Bankers Circle Of Life – principal reduction programs and unintended consequences.

Soylent Green Is People — April 7, 2011

Banks have had it good for the past couple of years. They’ve feasted on taxpayer subsidized capital, allowed accounting tricks to book phantom profits, and transferred privately created risk to the public’s balance sheet with nary a whisper of protest. Many responsible home owners continue to enriched said same bankers by paying mortgages that can never be refinanced into today’s lower rates. By owing more than the present value of their property, many home owners are trapped in a cycle that often ends in financial ruin.

The final insult to those who chose to live up to their promise to repay instead of living large through leverage will soon be here. How do I know this to be true? Since Irvine lives in the shadow of the House of Mouse, I thought it best to re-tell a family favorite to help illustrate how we got here, and what our inescapable future might look like.

In 2003 homeowners from far and wide came to see what special thing NAr-Fiki was revealing to the people of the USALands. Holding for all to see as an example of our bright future was Home Ownership, the offspring of King Conforming.

As Home Ownership grew older, King Conforming took him up to the highest point of the land – Peak Equity – and showed him a bountiful future. “Someday you’ll be a part of the Circle of Life. You’ll buy a home, pay off the loan, have plenty of equity to share with your children, and eventually see them become a home owner just like you.” That’s how it’s supposed to work out.

Unfortunately things began to go the wrong way in the USALands. Bankers ran out of loan programs that allowed greater fools to purchase homes at ever inflated prices. People began to panic. A mad rush to the exit began.

Home prices fell, crushing King Conforming. The only Big Cat left alive after the stampede was Home Ownership’s mean old Uncle “Sam” and the banker cartel.

During the Great Recession, Uncle Sam and his minions pushed Home Ownership out of the USALands. Jobs were few and far between. Prices were tunneling their way to the center of the earth. Only a few places seemed hospitable to relocate to. Eventually Home Ownership found the OC Oasis, a land flowing with milk an honey. There he made a few friends – the chatty Rodent and a well fed Pig. Home Ownership marveled at the lifestyles Rodent and Pig had – swimming pools with waterfalls, eating out more than in every night. How could they pay for their life of luxury? “Home Equity Ponzia” said Rodent. “It’s a wonderful thing”. Home Equity Ponzia, ain’t no crying shame”. “It means “No Worries” exclaimed Pig. Home Ownership was a little unsure of what all this meant and so didn’t dive in to debt along with his new neighbors.

As time went on life in the OC Oasis wasn’t going as planned. He wasn’t fully employed, things were getting a bit tight financially. In a vision one night King Conforming appeared telling Home Ownership that since he paid his house loan on time, certainly there were programs available that might make things easier, but they could only be obtained by going back to the land that Uncle Sam ruled. Even old NAr-Fiki came by, reminding Home Ownership that strategic default was a shameful, bad thing.

Home Ownership asked Uncle Sam to force his minions to let up on his loan terms, but to no avail. “Change?” asked Uncle Sam… “What is this hopey change you speak of? My banker cartel can’t profit from changing your loan terms so why would we do it?” Home Owner tried down to the last ounce of his strength and legal capacity to wrest control of his financial future from the bankers clutches but alas, it wasn’t to be.

Home Ownership was surprised to see his friends Rodent and Pig sitting next to Uncle Sam. ” Whatever remains after my bankers are done with you”, sneered Uncle Sam, “will be given to these two”. “Hey”, Rodent and Pig sang in unison, “We’ve got to maintain our lifestyle somehow. HomeEquity Ponzia!” Uncle Sam’s last words to the cornered Home Owner were chilling – “That’s how the Circle of Life really is, baby!”

And so the bankers devoured Home Ownership. The End.

Hey, I didn’t say the story would had a happy ending. This isn’t some friggin’ fairy tale.

Principal reduction plans are coming to USALands. Uncle Sam and his banker minions have several programs in place to get this started.

We’ll focus in this post on what may become the biggest, baddest one of all, but first:

The Why Question.

Why are bankers going to reduce principal? What benefit might there be for them? The answer to this question is fundamental in understanding the reason for these programs. Like any complex story, it’s best told when the details are simplified. The following is a close approximation of why PA loans will start in earnest, but not a scenario that fits all circumstances. Also, we’re going to use a few assumed names along the way for copyright avoidance illustration purposes.

In 2008 Bank of Albania (BA) was given incentives by the Government to absorb the assets of the troubled mortgage lender Capital Wagon (CW), one of many marriages of convenience during those days. Venture capitalists also began to purchase from the FDIC mortgage debt from other failed banks over the past few years. Thecompanies essentially paid a net price of .20 cents on the dollar or less for these troubled mortgage assets. Some assets turned in to REO’s, some loans were modified to keep the regulators and Congress at bay, but a vast number of these loans are simply not performing, threatening to swamp the survivor institutions balance sheets.

HUD created several programs to help facilitate mortgage relief for income distressed home owners, but it is the FHA Short Refinance / Negative Equity program that will be used to cycle the remaining private non-performing loans into taxpayer guaranteed debt.

Aren't they all bad banks?

Banks like BA will create a “bad bank” (BBA) – a place to dump off load their CW legacy assets at perhaps .40 cents on the dollar. That’s a nice profitable return (since their cost basis was .20 COTD) that BA conceivably could use to declare itself a “Well Capitalized” bank again.

BBA will now contact the home owners and offer them an FHA Short Pay refinance. Imagine a home owner getting a call from their loan servicer that goes something like this:

BBA – Hi, is this Mr. Refi Rodent?

RR – Yes it is.

BBA – I see you owe us $500,000 on a Stated Income 5/1 ARM.

RR – You mean the loan I’ve not made the $2,700 payment on for the last two years, The one with a rate of 3.2%?

BBA – Certainly! Here’s what I’d like to offer you. We see that home values in your area are now at $350,000. What if we cut your principal balance by $175,000 down to $325,000 and give you a 6.0% 30 year fixed loan. The payment would be $2,260. You owe less, your payment is reduced by $440, and all we ask is that you re-start to pay your loan for the next 60 days while we process this principal reduction. Deal?

RR – Frak YAH!

So in a few quick months BBA has turned a non-performing, un-sellable $500,000 loan (that cost them $200,000 when “purchased” from BA) into a shiny new easily re-sellable recourse FHA loan at $325,000 which you and I now are on the hook for as a taxpayer. My guess then is that BBA will in turn sell the loan back to BA at .80 cents on the dollar ($260,000) which makes the “Bad Bank” look like a pretty savvy operator. BA now has a 6.0% rate loan on their books which cost them originally around $100,000. The Bankers Circle of Life!

Remember this important factoid: The banks paid the market value of these loans or $100,000. The borrower is paying on the contractual value, or $500,000. When an FHA Short Pay refinance is transacted, the home owner is not getting a reduction in principal equal to the value of the loan, according to the bank’s valuation of the asset. The home owner is actually increasing the amount of their debt from the $100,000 assumed value to $325,000 present value based on current home prices. What happens tomorrow if the value of homes drops by another 20%? That’s the FHA Short Refinance borrowers Circle of Life. Their best course may be to again stop paying their loan. Rescue came to them once before. Whose to say it won’t happen again?

Some loan service companies offering these negative equity refinances will add a 5 year clawback provision. If there is a principal reduction of $100,000 and you sell at a higher price than current value, the home owner will have to give up the gain. After 5 years pass the feature sunsets. I’d be happy to wait 60 months before pulling the rip cord and bailing out if it meant I could sell for a gain, wouldn’t you?

Additional issues.

The borrowers who will have these offers made to them are those who took out Alternative Financing (ALT-A) or other now toxic portfolio loans, not traditional FNMA Agency 30 fixed rates. The Government created the Home Affordable Refinance Program (HARP) for those mortgages. These loans simply had the rate and not the principal balances reduced. Loan to Values under HARP were capped at 125% which does not help you if you purchased in parts of the Inland Empire or pretty much anywhere in Kern County. You’re stuck with the loan balance and the rate from 2006 unless you strategically default. Thanks for playing.

As principal reductions begin to spread, the social consequences will be catastrophic. When your neighbor comes over to share their excitement about their BA loan balance reduced by 35%, what will BA’s response be when you phone to get the same deal? That call will go something like this:

Responsible Home Owner: Hi, I’ve got a $417,000 30 year fixed loan that I didn’t refinance. My rate is 6.0% but values are such that I cannot fit within the HARP guidelines. The neighbor across the street just refinanced with you and got a lower balance. I’d like to do the same thing.

BA – I see that your loan is owned by Fannie Mae. Take it up with them.

Responsible Home Owner – But you made the loan, you take the payments, and you just refinanced someone I can see from my living room window lounging in his back yard pool. What’s the deal?

BA – I’m sorry, We actually bought this loan from another bank that wasn’t us even though we did have the loan originally. Besides only special cases can use this program. Would you like to open a new CD account with us? Our new rates are .00011013 percent for 60 month!

Responsible Home Owner – FFFFFRRRAAAACKKK YOOOOOOO!

Why should Responsible Home Owner continue to make their house payment at that point? Is it made out of guilt, obligation, or shame? To be honest, I’d have real doubts why I should fork over good money after bad if my neighbors got a consequence free haircut on their loan balance.

What now happens to property values? Well for one lets say values remain flat. The FHA Short Pay home owner decide to put their home on the market at the same time you do. Their sale will be an “Equity Sale” at a market price. Yours will be a Short Sale that might not close. If values fall further, their home will might also be a Short Sale, perhaps even an assumed FHA loan. Yours will likely become an REO. If values increase, you might eek out a slight profit and rent from there on out. Their gain will go towards the purchase of a better home in a nicer neighborhood.

In a world where principal forgiveness, unevenly and inequitably applied, becomes normative, the responsible will end up as waste byproduct in the Bankers Circle of Life. You can’t fight the coming principal reduction wave. It’s reach will stretch not just through the financial world, but down to the very streets we live on. It’s simply the amplified end point of a national policy of that enforces zero consequences for any actions.

Hakuna Matata er… HomeEquity Ponzia to all.

Soylent Green Is People.

It's the Circle of Life

And it moves us all

Through despair and hope

Through faith and love

Till we find our place

On the path unwinding

In the Circle

The Circle of Life

The Lion King — The Circle of Life

Some short sales aren't really for sale?

Today's featured property has been on the MLS for over three years. When a property is on the market for nearly 1,111 days, is it really for sale? Either the price is too high, or other conditions are preventing a sale from taking place which effectively remove it from the listing pool.

I write often about shadow inventory, but has anyone measured the MLS inventory that never transacts? There are currently 157 properties on the MLS that have been for sale for more than 180 days. Not to give false hope to the bulls, but if 150 listed properties aren't really for sale, how much inventory do we really have?

View: Back Bay, City Lights, Estuary, Golf Course, Hills, Mountain, Park/Green Belt, Pool, Trees/Woods, Water

Year Built: 2003

Community: Airport Area

County: Orange

MLS#: S515125

Source: SoCalMLS

Status: Active

——————————————————————————

Best location in building with breathtaking views of the San Joaquin Nature Preserve and Wetlands, golf course, city lights, along with one of the three pools. This is a rare, private one bedroom and one bath Carlton Arms unit, with a walk-in closet, brand new carpet, granite counter tops, washer, dryer, dishwasher, refrigerator, crown moldings, and additional appliances included. The Watermarke community offers spectacular ammenities boasting three pools and four spas with cabanas, a 24-hour elite fitness center, facialist, masseuse, covered and lighted full-court basketball, ground and roof top tennis courts, and parks with playgrounds. The Clubhouse also offers concierge services, a gourmet kitchen, dry cleaning, sitting areas, an extensive library, custom movie/screening theater room, and business center. A must-see opportunity awaits!

Thank you, Soylent Green Is People. Apparently, you are my cartooning muse.

Over half of poll respondents believe home ownership encourages excessive debt. Is the glass half full? Is public becoming more aware of the true cost of ownership? Is the glass half empty? Is the public becoming apathetic to the huge debt burdens they are asked to take on.

Debt is only a problem for those who plan to pay it off. Ponzis, and sophisticated personal financial managers, use debt as a tool. If debt is on a house Ponzis can borrow against, the house is given the responsibility for paying off the debt. This shifting of responsibility is the Ponzi moment.

Going Ponzi is a psychological event. It occurs when the debtor comes to believe they will never pay off a debt with their wage income. They abdicate responsibility for repayment to the house itself. For Ponzis debt is not a problem. Only the inability to obtain more debt slows down a Ponzi.

If the Ponzi mind becomes widespread, house prices get bid up by those willing to pay any price to obtain free HELOC money. The rest of the world — the people who plan to pay down a mortgage with their wage income — they are faced with paying the Ponzi premium, and they face the risk of loss if they want to liquidate after one of the inevitable market crashes.

This article reviews a recent poll on American attitudes towards owning a home in light of the Great Recession and the housing crisis, and reevaluates the place of homeownership in the American Dream.

Homeownership is at home in the American Dream

Eighty percent of Americans believe it is of total importance they buy a home one day, 90% say they would buy their current homes again and 70% would advise their family and friends to purchase a home as a valuable long-term investment. Clearly the vast majority of Americans still sport a decisive thumbs up to homeownership despite the risk of loss inherent in homeownership made evident by the Great Recession and the housing crisis.

Our concepts of ownership are primal. Our desire to possess and defend a territory is rooted in basic survival needs for food and shelter. Irrespective of what happens to the price of shelter, people are going to desire it.

What's truly delusional is the despite the long-term losses people are going to endure, so many would still advise their friends and family to commit the same financial mistake and purchase a house as an investment. It is consumption, not investment.

All this is according to the latest Allstate Insurance and National Journal Heartland Monitor Poll which Financial Dynamic conducted to monitor middle-class America’s maneuvers in the economy’s post-recessionary aftermath. (The poll recorded a +/- 3% margin of error for 1000 respondents.) [For more information on the “Homeownership and the American Dream” poll, see National Journal article, A Solid Foundation: Why Americans still long for their own homes.]

The American Dream of wealth and independence sustains American homeownership, a national aspiration which is the result of society’s suspension of disbelief in the myth that home prices continually go up.

It does require an amazing cognitive dissonance to ignore the crash and continue to cling to old fantasies, or even deny the crash entirely. People filter data to see what they want to see.

For example, two-thirds of those Americans polled experienced some type of financial distress such as an underwater mortgage and still believe owning is better than renting.

It takes a great deal of faith in appreciation to believe ownership is better than renting when (1) the cost of ownership is higher than renting and (2) owning prohibits moving without a short sale. Trapped in an expensive money-rentership arrangement doesn't sound better than the cost savings and freedom of renting.

Seventy-five percent believe homeownership will help them achieve the American Dream, compared to the 22% who believe otherwise, and 80% believe owning a home is an integral piece of the American Dream, second only to raising a family.

Californians polled in the survey generally exhibit the same level of national spirit for homeownership ― 68%, compared to the national 75%, believe owning a home will help them live the Dream. In addition, 83% believe owning is a better financial decision than renting, and 71% would advise family and friends to buy a home to build long-term assets. (The poll’s California data recorded a +/- 10% margin of error for 99 respondents.)

Optimism and persistence are American

Homeownership is not solely an economic decision. The American image of the home is deeply imbued with social and cultural sentiments. Though 25% believe owning a home is the best type of investment for their money only behind a retirement plan, 60% in the survey view homeownership chiefly as a means to settle down and raise a family. Thirty-six percent view homeownership as an opportunity to build equity.

I wonder what percent in California would say home ownership is an opportunity to get free spending money? I bet it's higher than 36%.

The general consensus is present economic troubles and housing market miseries are but minor impediments to the American Dream. Sixty-three percent of Americans and 67% of Californians trust the housing crisis is temporary and the housing market will improve. Nationwide 60% believe their skills coupled with a tough work ethic ― rather than the economy ― has the most impact on their ability to achieve the Dream.

It's good to know more than half still believe they have to work and contribute in order to achieve their dreams. If we every lose that, we are doomed as a nation.

Splintered views in uncertain times

Though many Americans are convinced they control their own Dream, the Great Recession and the housing crisis cast doubt over what part the government plays in subsidizing American homeowners. Americans and Californians are split over the matter. Fifty percent of the nation and 42% of the state want to reduce the role of government agencies like Fannie Mae and Freddie Mac, yet 42% nationwide and 52% statewide want the government to continue its role. On the home mortgage tax deduction question, 50% want the government to keep the subsidy, while 43% want to limit or eliminate it. Californians polled at 56% to keep the subsidy and 37% to trim it down or cut it out. [For more information on getting rid of the home mortgage tax deduction, see the February 2011 first tuesday article,The home mortgage tax deduction: inducing debt and stifling mobility.]

I think it's interesting that nearly half would like to see the GSEs disappear along with the mortgage interest deduction. That represents a significant change of thinking since the bubble popped in 2006.

It should be noted the poll shows some Americans appear misinformed about how the government housing policy works. Seventy-five percent report they have not benefited from federal homeownership policy even though 71% report they have taken a home mortgage tax deduction.

Americans do not understand the myriad of ways government policy impacts the housing market. It isn't surprising that 75% don't realize they benefit in some fashion (how many have government-backed loans?)

The same level of ambivalence exists on the question of whether homeownership stabilizes American society. Forty-two percent agree homeownership has created stable communities because it encourages people to actively invest in a neighborhood and its surrounding area. However, 51% think homeownership encourages people to incur high amounts of debt, which renders them unable to pay their mortgages if they lose their jobs, and results in increased foreclosures and blighted communities.

The community benefits of home ownership are overshadowed by the harsh reality of dodgy loans creating blight and foreclosures. Remember Vicente the Fox?

California’s response to the relationship between homeownership and the health of a community differed from national results, which is not surprising since the state has been hit much worse by the housing crisis than the rest of the country. Seventy-seven percent of Californians report their homes have decreased in value (fact: all have decreased), compared to the 41% nationwide, and 40% say their homes are underwater, compared to the 18% nationwide.

The other 23% are the permanently kool aid intoxicated or completely oblivious.

As a result, 61% of Californians believe homeownership has only made communities less stable.

Home ownership didn't destabilize communities, loan ownership did.

Younger Americans surveyed seemed the most uncertain about buying a home, but overall, the poll demonstrates the economic down has caused Americans to ask questions about homeownership and the American Dream, but it has not budged their desire for it.

Time to reevaluate the Dream

Americans, and Californians included, are split or confused on what role the government has on the issue of homeownership. They are divided as to whether the government should continue to intervene in the housing market.

Americans crave homeownership, even if they understand they will have to trudge through the backwash of another cyclical recession and accompanying housing crash. But Americans need to distinguish: the Dream is homeownership, not homedebtorship, as promoted by interest deductions. The craving however is not the result of tax policies, which if eliminated would not alter the American compulsion to own and gain wealth.

Homeownership is not for everyone, and those who are forced to finance that acquisition might ask themselves whether owning is the right decision. The job mobility provided by renting is what has always enhanced California’s economy, attracting the most creative and industrious people in the world. Here, homeownership is near 50% of those housed in California, while the rest of the nation ranges around 70%.

The real estate industry calls the mortgage interest deduction the “catalyst of the American Dream,” but an American Dream based on irresponsible indulgence has more costs than benefits. [For more information on the housing subsidy problem, see the December 2010 first tuesday article, The mortgage interest tax deduction imbroglio – the squabble continues.]

At its very core, a home is a form of shelter, a basic life necessity. However since the 1970s, national public policy encouraged and exploited by lenders, builders and brokers marketed homeownership as a symbol of success and autonomy. The glamorous spotlight on the accessibility of homeownership for everyone thus casts a shadow of disapproval on renting, but what is there to be embarrassed about when paying cash to buy a home? If being in debt is a foundation to homeownership in America (and one of the reasons for the housing crisis), then Americans need to change their attitudes towards homeownership. Dreaming about homeownership is laudable, but on a solid foundation. [For more information on the trends of American attitudes towards housing, see the October 2010 first tuesday article, Is homeownership a luxury or necessity?]

$417/SF in debt

These little houses carry a remarkable amount of debt. I really like this neighborhood, but the prices of houses here are extraordinarily high on a per-square-foot basis. Today's featured property was purchased on 11/29/2004 for $520,000. The owners used a $416,000 first mortgage and a $104,000 down payment. They refinanced on 10/13/2005 with a $420,000 first mortgage and a $80,000 second mortgage. They withdrew all but $20,000 of their down payment.

They are priced to sell at breakeven in hopes of capturing the remainder of their down payment. However, since they are the highest priced home in Northwood on a per-square-foot basis, I have my doubts whether they will get their money back.

Charm galore in this 2 bedroom plus den cottage home in Northwood Pointe. Light & open floorplan features living room w/ built ins, gourmet kitchen w/ sparkling white counters & cabinets, & dining area w/ cozy fireplace. All rooms are open to each other, making this a perfect floorplan for living & entertaining. Gorgeous slate tile flooring accents the main floor. Tranquil master bedroom features bath area with dual sinks, travertine tile floors, & walk in closet. Second bedroom has it's own private full bath w/ travertine tile floor. The versatile den could also be used as an office, playroom, nursery, workout room, or craft area. Your yard & outdoor living area is highlighted by a custom built in BBQ area w/ sink & slate topped dining bar, a patio trellis with outdoor lighting, & mature trees for privacy. Enjoy relaxing in this tranquil oasis at the end of the day. 2 car garage has built in storage. Walking distance to award winning Canyon View Elementary & Northwood High. A real gem!

The Wells Fargo CEO is getting involved in the political posturing around mortgage market reform being considered in Washington. Today we will examine his recent statements on reform.

The CEO of Wells Fargo, John Stumpf (I like saying that last name), has put forth some good ideas concerning mortgage reform. I recently reported that he wanted to see a 30% down payment requirement on the new qualified residential mortgage. His proposal is self-serving as his bank is better able to carry loans than small banks, but it also makes for good policy, so I'll embrace him when he's right.

By John Stumpf, chairman, president, and CEO, Wells FargoApril 4, 2011: 6:09 AM ET

FORTUNE — For most Americans, their home is the largest and most important investment they will ever make. Ensuring that they have the right kind of mortgage is critical to their financial well-being and — as we've seen recently — critical to our entire economy.

That means we have to solve the Fannie Mae and Freddie Mac problem and eventually figure out the proper role of the federal government in supporting a secondary market for home mortgages. Doing that right is one of the most important issues facing Congress and the Obama administration.

This issue is very important. As i wrote recently in Defining qualified residential mortgages: a battle over minimum down payments, “We have witnessed many tempest-in-a-teapot issues like robo-signer that flare up and go away without long-term impact on the housing market. This issue is different. The minimum qualifying standard on this loan is going to become the bedrock of mortgage finance. If we get this wrong, we will rebuild the mortgage market on a weak foundation.”

Some people ask, Why do we even need a secondary market for home mortgages? Why don't we just go back to the good old days before those markets existed and require banks to hang on to all the mortgages they create?

Let me tell you why. When I went to buy my first house in 1976, mortgage money was hard to find. In fact, it was rationed. Banks simply didn't have the deposits on hand to meet the demand. That was 35 years ago, and we don't want to go back to those “good old days.” Mortgage rationing is not the future we want for our customers, their children, or their grandchildren.

I would have no problem at all going back to the mortgage market of 1976. Mortgages were almost exclusively 30-year fixed rates, debt-to-income ratios were manageable, and house prices were affordable. The debt we created since then has only served to inflate real estate values, destabilize pricing, and increase the overall level of indebtedness among the populace. From a banker's point of view, the last 35 years made great progress — at enslaving the population.

Consider these facts: There are 76 million homes in the U.S., of which 51 million have mortgages. Taken together, those mortgages represent a debt of $11 trillion. That's a level of debt that banks can't afford to hold on their balance sheets alone. As a nation, if we want to make home ownership broadly available and affordable, we need a secondary mortgage market that operates fairly and efficiently for all parties.

Freddie Mac and Fannie Mae were created in part to help achieve those goals, but they've run into big trouble along the way. They now own or guarantee nearly 31 million home loans, worth more than $5 trillion. Their role is so critical in mortgage finance that the federal government bailed them out in 2008 to the tune of what might end up to be more than $250 billion.

This is how your tax dollars are paying the debts of Ponzis everywhere. The stupid loans both insured and purchased by the GSEs at the top of the housing bubble paid for many things I would rather not see my tax dollars go toward.

So as Fannie and Freddie unwind, as they certainly will, what principles should shape the future of home financing? I believe the answer comes in three parts. First, all parties involved in making and investing in mortgage loans need to share a financial interest in the quality of those loans. That includes the customer taking out the loan, the financial institution or broker originating the loan, and the investor who ultimately owns the loan. All parties need to have skin in the game. If originators don't have a financial interest in the loan, they will have less concern for its quality, and poor lending decisions will happen and be passed along to investors. That creates a house of cards.

I believe his analysis is accurate. Without financial accountability throughout the supply chain, the incentives are wrong, and bad behavior will ultimately ensue.

A healthy debate is already taking place about how much a homeowner should put down and how much a bank should keep on its balance sheet when it bundles and sells mortgage loans. There is no magic number out there, but I can tell you one thing: The more the risks and rewards of a mortgage loan are shared by all parties — and the better those risks and rewards are understood — the better the quality of the loan will be.

Will this mean higher down payments for homeowners and more financial skin in the game for banks? Probably so, but the long-term costs for homeowners, bankers, and the economy will be dramatically lower. Just look at what past mortgage lending practices have cost all of us.

Mr. Stumpf bears some responsibility for the past mortgage lending practices that caused our woes, doesn't he?

Second, whatever role the federal government assumes in mortgage finance going forward, its role needs to be explicit, not implicit. Currently federal backing for Fannie and Freddie is implied because they are “government-sponsored enterprises.” It needs to be crystal clear for investors around the world whether GSE loans are backed by the full faith and credit of the United States. If they are, consumers would benefit from worldwide liquidity for mortgage products.

Right now, it is crystal clear: GSE mortgage-backed securities are insured by Uncle Sam. There is little difference in risk between a 10-year T-bill and a GSE MBS. There is usually a spread between the two that represents the risk premium the market demands for risk of loss. With direct government backing, the spread is very small, so mortgage interest rates are relatively close to 10-year yields.

Keeping interest rates low allows lenders to roll over their toxic debt into amortizing loans insured by the US government. Eventually the mortgage market will be cleansed, or at least the losses will be transferred to Uncle Sam who can borrow money to pay for it. If lenders absorb all the losses, significant capital would exit the banking system, and our economy would be seriously impaired.

The private market at the government fringe — the jumbo market — is a complete mess. Spreads are high because jumbo loans carry risk, and the underwriting standards are high which means very few borrowers qualify. Hence, the high end has low transaction volume, and a lot of shadow inventory.

If we fully convert to a private market, mortgage interest rates will almost certainly rise because the private market will price the risk back in to mortgage-backed securities. If rates rise too soon, affordability will become a problem, and the supply liquidation will push prices lower.

To protect taxpayers, adequate levels of private capital should be required to take the risk of loss. In this way, the federal government would only act as a “catastrophe risk” backstop much like the role the FDIC plays in protecting bank deposits up to a certain limit. Banks would pay a fee, just as they do for FDIC insurance, and the homeowner's mortgage would be guaranteed up to a certain amount by the federal agency providing the insurance.

This is the traditional role of the FHA. The government through the FHA makes sure loans will always be made available to people who meet their underwriting guidelines. These guidelines are strict in order to protect the government from loss. And despite some weakening after the bubble, FHA guidelines still serve to limit the taxpayer's risk.

The private market is free to underwrite FHA loans, or it can create competing products to entice customers. Since the FHA is a government agency, it doesn't mind losing market share to the private sector. It has no pressure to change its guidelines to adapt to the market. If its market share goes down, the bureaucrats process less paper. They get paid the same either way.

The FHA is a worthy government bureaucracy as far as they go, but the rigid guidelines they adhere to make for a poor business model. Private sector lenders must be responsive to changes in the marketplace or they will lose customers and go out of business. Therefore private lenders must have more flexible guidelines than the FHA if they are to survive.

The GSEs are a poor synthesis of a government program and a private sector endeavor. The mandate of a government program is to provide financing and limit taxpayer risk. This is incompatible with the survival needs of a business entity. The GSEs were asked to provide financial innovation. Financial innovation is an oxymoron. It usually results in a financial bubble or Ponzi scheme.

The GSEs in their current form must die.

And third, as we move forward in a post-GSE marketplace, we need to make sure we have uniform underwriting and servicing standards for mortgage loans, and more common products for what are called conforming mortgage loans. An efficient secondary market depends on relatively standard products and processes. Otherwise every batch of loans has to be examined in detail for its unique qualities, an examination that results in higher transaction costs and ultimately less attractive investments. The lack of standardization drains the lifeblood out of secondary market operations.

Mortgage financing is a big deal for millions of Americans and for our economy overall. All sides should be looking for solutions that will help all Americans. The path forward will not be easy, but I truly believe the solutions can be found. It will require hard work, courage, and cooperation across the board.

The real question we must face with the GSEs is to what degree society wants to subsidize the mortgages of middle- and upper-middle class Americans. We could convert the shell of the GSEs back into a government program, sell off the portfolio of securities, and collect insurance fees to reserve for future losses. We could layer them on top of the FHA to provide price support to places like Orange County.

There will be many in Republican rural America that will resist the idea of their tax dollars going to subsidize the shenanigans they see on the Real Orange County housewives. Republican Orange County won't resist quite so much.

CNN Money on mortgage issues

A little Ponzi

Not all Irvine loan owners are big-time Ponzis. Some are merely frequent credit card consolidators who slowly but consistently grow their mortgage balances albeit at a rate less than appreciation. Is that wise?

I hate to give borrowers in this category a “passing” grade, but this is the reality for most Americans. Growing credit card or mortgage debt slowly generally can be compensated for through home price appreciation, and although I consider this a bad idea, I can't really call it HELOC abuse, just foolish HELOC use. Is there a distinction there? I will let you decide.

Financial planners will tell you that most people fail to budget properly for unexpected expenses (they don't save), so when they fall behind a little each month, they put the balance on a credit card and hope they can pay it back with a tax return — or during the bubble with a visit to the housing ATM.

People are still going to manage their bills this way going forward, and there will be pressures to “liberate” this equity to pay for these expenses. The money changers will continue to peddle this nonsense as sophisticated financial management. It is a stupid way to manage debt, and I give it a C.

This property was purchased at the bottom of the last real estate crash.

On 9/22/1997 they paid $301,000 for today's featured property by using a $240,450 first mortgage, a $30,050 second mortgage, and a $30,600 down payment.

On 1/12/1999 they obtained a $55,000 stand-alone second and withdrew most of their down payment.

On 1/29/2002 they refinanced with a $282,000 first mortgage.

On 7/9/2003 they refinanced with a $322,700 first mortgage.

On 7/14/2006 they refinanced with a $322,000 first mortgage. I am impressed by that one. Three years after their last refinance, a period in which their property value went up 50% or more, they did not add to their mortgage.

On 5/23/2008 they refinanced with a $350,000 first mortgage.

On 8/3/2010 they refinanced one last time with a $360,000 first mortgage.

The will likely leave the closing table with a $500,000 check. It's not as big as it could be, but it is much more than most Ponzis take with them.

The problem with Ponzi borrowing isn't the high-profile flame outs I profile here frequently. The real problem is the pervasive use of Ponzi borrowing to sustain daily life. It's the little guy multiplied millions of times that destabilizes our economy. California has become so dependent upon borrowed money that the entire state economy crumbles when mortgage money fails to flow in.

The only real solution is a period of frugality and economic weakness while the Ponzis adjust to living within their means. We will see some of this natural economic purging take place as many Ponzis endure the unceremonious fall from entitlement. However, this cleansing will not go far enough because government policy and our federal reserve seem determined to keep the Ponzi scheme alive.

* * * ONE OF ONLY 10 HOMES ON A SINGLE LOADED STREET FACING MEADOWOOD PARK AND CANYON VIEW ELEMENTARY SCHOOL * * * Cleaner than a Microsoft and Apple computer lab – COMBINED!!! MOST UNIQUE LOCATION ON THE IRVINE RANCH! Light and bright east facing with cathedral ceilings! Incredible privacy and location. Amazing floor plan with guest suite downstairs, 3 bedroom upstairs with option for bonus over garage or 5th bedroom with own bathroom. upgarded with cutom paint, large covered patio, granite kitchen counters, upagrded cabinets, plantation shutters. Hardly been lived in and immaculately clean!

MOST UNIQUE LOCATION? I don't think uniqueness can be modified. How is something less unique than something else? It's either unique or it's not, right?

* * * Cleaner than a Microsoft and Apple computer lab – COMBINED!!! He has a sense of humor.

upgarded? upagrded?

What were you doing at 10:50 last night?

Last night due to a technical problem at 10:50, I lost today's post. I last successfully saved the basic infrastructure of a post, but the analysis of the CEOs comments — something I spent two hours writing — was gone.

For a moment, I was in total shock. I could believe what happened. After a few unsuccessful attempts at recovery, I conceded defeat, and I was devastated. The sense of loss was powerful and jolting. Then the reality of staying up late to re-write the post set in, and I was just devastated (and pissed). I sought out my wife to calm down.

I didn't realize how important it was to me to put up a daily post (weekdays anyway). I felt like an injured Brett Favre who wanted to start if for no other reason than he always started. Some guys are just built that way. I calmed down, wrote this pep talk to myself, drank my coffee, and hunkered down to rewrite it all. Reliability trumps sleep.

.jpg)

.png)

As Home Ownership grew older, King Conforming took him up to the highest point of the land – Peak Equity – and showed him a bountiful future. “Someday you’ll be a part of the Circle of Life. You’ll buy a home, pay off the loan, have plenty of equity to share with your children, and eventually see them become a home owner just like you.” That’s how it’s supposed to work out.

As Home Ownership grew older, King Conforming took him up to the highest point of the land – Peak Equity – and showed him a bountiful future. “Someday you’ll be a part of the Circle of Life. You’ll buy a home, pay off the loan, have plenty of equity to share with your children, and eventually see them become a home owner just like you.” That’s how it’s supposed to work out.

.png)

All rooms are open to each other, making this a perfect floorplan for living & entertaining. Gorgeous slate tile flooring accents the main floor. Tranquil master bedroom features bath area with dual sinks, travertine tile floors, & walk in closet. Second bedroom has it's own private full bath w/ travertine tile floor. The versatile den could also be used as an office, playroom, nursery, workout room, or craft area. Your yard & outdoor living area is highlighted by a custom built in BBQ area w/ sink & slate topped dining bar, a patio trellis with outdoor lighting, & mature trees for privacy. Enjoy relaxing in this tranquil oasis at the end of the day. 2 car garage has built in storage. Walking distance to award winning Canyon View Elementary & Northwood High. A real gem!

All rooms are open to each other, making this a perfect floorplan for living & entertaining. Gorgeous slate tile flooring accents the main floor. Tranquil master bedroom features bath area with dual sinks, travertine tile floors, & walk in closet. Second bedroom has it's own private full bath w/ travertine tile floor. The versatile den could also be used as an office, playroom, nursery, workout room, or craft area. Your yard & outdoor living area is highlighted by a custom built in BBQ area w/ sink & slate topped dining bar, a patio trellis with outdoor lighting, & mature trees for privacy. Enjoy relaxing in this tranquil oasis at the end of the day. 2 car garage has built in storage. Walking distance to award winning Canyon View Elementary & Northwood High. A real gem!