According to the listing agent, this listing may be a pre-foreclosure or short sale.

Extraordinary find in beautiful Northwood Pointe. One of a kind home features European accents throughout. Venetian plaster by Parisian artisan, custom interior stain glass window, and gorgeous wrought iron bannister and balcony. Detailed crown moldings and baseboards, plantation shutters, dimmer light switches, solid wood interior doors and elegant wood floors. Kitchen with granite opens to family room with fireplace. Separate formal living room with vaulted ceilings and ajacent formal dining room. Convenient downstairs bedroom currently used as an office. Custom built laundry room with solid wood cabinets, granite countertops, deep basin sink, limestone floor .All closets with custom built ins. 3 car garage with loft storage racks and epoxy flooring. Walk to Award Winning Schools, community pool, parks and tennis courts.

by JON PRIOR — Monday, December 20th, 2010, 11:02 am

Bank of America Merrill Lynch analysts said the most likely way households will deleverage roughly $1 trillion in excess debt is through the default of more underwater mortgages.

Home prices in the Standard & Poor's/Case-Shiller 20-city index have dropped 28.6% from the peak in the summer of 2006. This has led to more than 10.8 million homes, or 22.5% of the entire U.S. market in negative equity as of the third quarter, according to the analytics firm CoreLogic. And while that percentage is down from the 50 basis points from the previous quarter, negative equity remains the primary factor holding back a recovery in the housing market and the overall recovery.

Analysts said the collapse in home prices means the asset value supporting Americans' debt is no longer there.

Home values were an illusion created by excessive debt. Americans were offered free money for nothing more than owning a house. This made houses very desirable which prompted more buying and drove prices higher. As prices moved higher, banks were willing to give out more and more free money in order to entice Americans to buy more houses to get more free money.

It was a Ponzi scheme.

The collapse in values is simply a reversion to what prices would have been if we hadn't inflated a massive housing bubble.

“It’s the holidays and talk of deleveraging needs would appear to be sacrilegious or even un-American,” BofAML analysts said. “Most of the deleveraging will come through default of underwater mortgages, although less consumption likely will be part of the equation as well.“

But consumers are not alone. Excess debt is also an issue in municipalities and sovereign nations. Recent increases to interest rates will put more need for the U.S. to begin implement fiscal constraint.

“At a minimum, the vast amounts of excess debt permeating the developed economies will act as a drag on growth for some time,” analysts said.

Of course there will be less consumption. We are no longer giving out hundreds of thousands of dollars of free money to Ponzis. Until we start doing that again, consumer spending will be down. Hopefully, we won't be giving Ponzis billions in tax subsidies and bailouts in the next cycle, but you never know.

An example of necessary deleveraging

Someone bought today's featured property with a great deal of debt. They have so much debt that they can't sell the house for more than the debt owed, and they can't rent it out for enough to cover the payments. This is a money pit. The original buyer is getting nothing out of the property. It doesn't appear as if this property was ever lived in. It looks like a purely speculative play on appreciation without regard to carrying costs.

This leverage has no support. The borrower isn't going to bleed cash every month to support an investment with no current value very long. A borrowers tolerance for negative cashflow is the strength of their kool aid intoxication about prices coming back. What loan owners have is an option position — no current value but potential future value if prices rise — hope and denial are what they cling to.

If prices stay down for a long period of time, distressed borrowers are bleeding cash every month for a reward that never comes. Their option position never gets back in-the-money.

A financial position taken by the herd — many loan owners are underwater clinging to the hope of rising prices — is self defeating. With so many anxious sellers waiting for some magic price point where they get out whole, the herd creates a buffer of overhead supply waiting to be absorbed at higher price points.

Some of the sellers can't wait because the distress is acute. Many of the borrowers who completed HAMP loan modifications still had 65% or greater back-end debt-to-income ratios after the modification. The debt distress will be worse for some than for others, but it will continue to shake out supply until the excess debt — the debt not supportable by incomes — is removed from the system.

Many nice tract-home neighborhoods became elevated to the $1,000,000 club by borrowed money. People used to sell their homes and port $500,000 in equity to buy a $1,100,000 home. During the housing bubble, they would borrow $2,000,000 with an Option ARM and push prices of homes up to the ridiculous prices we see today. The problem with this is simple: the debt buyers cannot be replaced with equity buyers. Some neighborhoods may survive, but the more debt a neighborhood has, the more it will fall — when lenders finally get around to pushing out the squatters.

Today's featured property was purchased near the peak on 10/16/2006 for $3,518,000. The owners used a $2,814,167 first mortgage, a $351,771 HELOC, and a $352,062 down payment. Think about that — these people only put about $350K of their own money in a $3.5M purchase.

On 12/8/2006 they obtained a HELOC for $356,078 to get access to their full down payment.

According to the listing agent, this listing may be a pre-foreclosure or short sale.

Million $$ Views Luxury Estate – La Cima Model 1X on Single Loaded Street w Ocean/City Lights & Breathtaking Views * Welcome Entry Courtyard adjoints an Open Air Dining Loggia w Fireplace * 6 BR 6.5 BA + Hm Theater + Bonus Rm 4 Car Garage * Main Floor Master Suite * Complete Saparate Living Suite The Casita is a Private Oasis * 2nd Story Private Access to a spacious Living Rm w Open Kitchen * Super Launddry Rm * Lot of Custom upgrades

Launddry? Saparate?

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

If banks could store time in a bottle, they could keep in on the shelf with their worthless paper until the market gives it life again. Unfortunately, rather than storing time in a bottle, the remaining equity capital in our banking system is leaking away through servicing costs like sand in an hourglass. These servicing costs are hidden by amend-extend-pretend until disposition forces recognition of the losses.

Astute housing market observers note the amend-extend-pretend policy of banks is untenable in the long term. As some point, keeping fantasy books must intersect with reality. The fantasy had house prices going up until reality and fantasy intersected. I don't believe it can or will work out that way.

The weight of the inventory and the incentive to liquidate will have individual banks working against their collective best interest. Ultimately, the fantasy of amend-extend-pretend will become so implausible that the banks will find that position is no longer operative.

But what will it take to force banks to end amend-extend-pretend? In my opinion, the answer is increasing loss severities.

by JON PRIOR — Thursday, December 16th, 2010, 5:28 pm

Loss severities are expected to increase between 5% and 10% on residential mortgage-backed securities in 2011 as loss mitigation costs and foreclosure expenses go up, according to Fitch Ratings. This, analysts said, will push servicers to short sales.

It will not push servicers to short sales because the loss severities are large there too. In some cases, once the bank has to pay sales commissions, back taxes, back HOA dues and other costs at short sale, they would have been better off simply pushing through a foreclosure and getting their cash.

The loss severity, or the percentage of principal lost when a loan is foreclosed, on prime mortgage loans is currently at 44%. This, according to Fitch, will increase to between 49% and 54% in 2011. For Alt-A loans, the current 59% loss severity should increase to between 64% and 69%.

Currently, the loss severity on subprime loans is 75%, but Fitch predicts it will increase to 80% and 85% by the next year.

These loss severities had remained stable for more than a year. In the second quarter of 2009, the amount a lender could recover when it foreclosed on a mortgage was propped up by slightly improving home prices, low mortgage rates, homebuyer tax credits and government-funded modifications.

Loss severities leveled off because prices made a minor rally during the echo-bubble engineered by the government and Federal Reserve. It takes appreciating prices to make up for the losses from servicing costs.

Increased servicing costs from pressures to modify more loans and recent problems with many banks' foreclosure processes will drag down the amount of principal banks can recover from a foreclosure. Borrowers average 19 months without making a payment before they are foreclosed upon, a record high, and Fitch projects this to increase to 25 months in 2011.

Fitch Managing Director Diane Pendley said the answer for some lenders is a short sale.

“Servicers are increasingly turning to less costly alternatives to foreclosure such as short-sales,” Pendley said.

Recovery rates on short sales are usually 10% higher than foreclosures. Pendley said servicers are also reducing the amount of payments they advance to securitization trusts from delinquent borrowers, particularly on subprime loans. In November, Fitch said, servicers advanced only roughly 60% of delinquent subprime loans, down from 90% at the beginning of 2009.

Each month a loan is delinquent it costs 1.5% of the loan balance in carrying costs. That is a troubling rate of financial decay. Time is the actually the bank's enemy when it comes to loan loss severities. Banks are providing squatters time in hopes they will get current and keep the zombie debt alive. Eventually, the carrying costs are going to make the loss severities so large that banks will either liquidate or implode, after which they will be liquidated anyway.

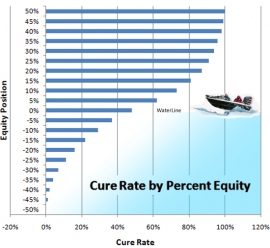

… Let’s start with real-world implications. The average borrower in foreclosure has been stuck in the default pipeline for more than 16 months, according to Lender Processing Services (LPS: 29.66 -1.69%), without making any sort of payment on their mortgage. That's well over a year, with some states even averaging north of this number. No wonder servicers are increasingly halting principal and interest advances, deeming loans unrecoverable. At that level of severe delinquency, there is simply no cure that can restore a loan to performing.

Here’s why: Consider that the average carry cost of a home in foreclosure is 1.5% of unpaid principal balance per month, on average, a figure I’ve been given by various servicing executives. For a $200,000 loan in foreclosure, that amounts to more than $48,000 in accumulated carry costs given the average age. That’s roughly a quarter of the entire original indebted amount.

(If you wondered how loss severities above 100% are materializing on liquidated debt, by the way, this is how you get there.) …

Loan severities will continue to increase as appreciation no longer hides the bleeding on bank's balance sheets. The longer these foreclosures are dragged out, the worse the loss severities will become.

A HELOC the bank deserves to lose

Sometimes when I see a really stupid loan in the property records, it really infuriates me that taxpayers are making up the business losses of people who approved such stupid loans. The owners of today's featured property went Ponzi. It was obvious they had gone Ponzi. However, some banking genius thought it was a good idea to extend a HELOC to a Ponzi in second position to an Option ARM. WTF?

Second position to an Option ARM?

Lenders willing to take on that kind of risk deserve the losses they receive. They gave the owners of this house free money to spend. They spent it, and now they can't pay it back. Anyone with an ounce of common sense could look at the property records and see this coming. Why didn't the banks bother?

Banks won't worry about future loan losses either now that they know the rest of us will bail them out. Moral hazard is an impossible problem to overcome. It can only be avoided.

This property was purchased on 6/26/2000 for $392,000 according to the property records. There is also a $392,000 first mortgage and a $58,800 second mortgage, so it is more likely the owners paid closer to $450,800.

On 3/18/2002 they refinanced with a $387,000 first mortgage.

On 11/13/2002 they refinanced with a $300,000 first mortgage and a $92,000 second mortgage.

On 3/2/2004 they obtained a $220,000 HELOC, and the problems began.

On 7/21/2004 they refinanced the first mortgage for $522,000 and obtained a $128,000 HELOC.

On 6/20/2006 they refinanced with a $656,000 Option ARM first mortgage and obtained a $82,000 HELOC.

I find that HELOC offensive in its stupidity. Anyone in lending with half a brain could see it was only a matter of time before these borrowers imploded (they already went Ponzi) yet they were extended a $82,000 HELOC on top of a loan product with a growing balance, the Option ARM.

If lenders had any concern for risk, they would not have made that loan. It angers me that I am paying for it with taxpayer bailouts.

Next housing bubble, I am going to figure out how to get a HELOC on my rental.

-$476 ………. Tax Savings (% of Interest and Property Tax)

-$651 ………. Equity Hidden in Payment

$247 ………. Lost Income to Down Payment (net of taxes)

$83 ………. Maintenance and Replacement Reserves

============================================

$2,758 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$6,609 ………. Furnishing and Move In @1%

$6,609 ………. Closing Costs @1%

$5,287 ………… Interest Points @1% of Loan

$132,180 ………. Down Payment

============================================

$150,685 ………. Total Cash Costs

$42,200 ………… Emergency Cash Reserves

============================================

$192,885 ………. Total Savings Needed

Property Details for 8 WESTMORELAND Irvine, CA 92620

——————————————————————————

Beds: 4

Baths: 3 baths

Home size: 2,132 sq ft

($310 / sq ft)

Lot Size: 4,750 sq ft

Year Built: 1985

Days on Market: 75

Listing Updated: 40522

MLS Number: U10004545

Property Type: Single Family, Residential

Community: Northwood

Tract: Cs

——————————————————————————

According to the listing agent, this listing is a bank owned (foreclosed) property.

Price reduction. REO. Nice 4 bedroom, 3 full baths SFR in very nice Courtside neighborhood. Newly painted interior, new stove, over the range microwave, new sink, disposal, etc. Very nicely landscaped with a deep lot. Near everything, freeways & shopping.

At a basic level, each of us wants the safety and security of an ordinary world of predictable surroundings and routines. The real estate and mortgage world we live in today is a surreal landscape of failed loan programs, ever-tightening credit standards, and uncertainty about the future of real estate prices.

The success or failure of many loan programs will determine the likelihood of their reappearance in an altered form. Subprime first-mortgage lending will return. The 20% down piggy-back loans and 100% HELOCs are not coming back soon. The second mortgage liens — the key problem for bank's residential loan portfolios — are performing very badly, and they will continue to post losses exceeding expectations. However, these loans are performing better than I thought they would because people are choosing to pay these credit lines even if they bail on the first mortgage.

Few good options

A distressed and underwater homeowner has few good options concerning their mortgage obligations. Most just keep paying even if it means sacrificing everything else. Many choose to accelerate their inevitable defaults, and they quit paying on both the first mortgage and the second mortgage.

If a borrower fails to pay either loan, the lender can chose to foreclose or try to negotiate a settlement. A seocnd mortgage lien holder has very little leverage in these negotiations because in a foreclosure, that lender is no longer secured by the property, and if the borrower has no other assets, there is little chance of recovery on the bad loan.

I had expected to see many people default on their second mortgage while keeping the first mortgage current. The first mortgage may not be underwater even though the CLTV is more than 100%. Most borrowers would consider the threat of foreclosure from a second lien holder to be an empty threat because that second mortgage gets wiped out in the foreclosure. People could go on paying the first mortgage and stay in the house because the second mortgage would not foreclose. What we are actually seeing is the opposite of what I expected.

by KERRY CURRY — Tuesday, December 14th, 2010, 6:50 am

Borrowers who strategically default on their first mortgage often continue to pay on home equity lines of credit, according to a new white paper from two authors with the Philadelphia Federal Reserve.

The authors, Julapa Jagtiani and William W. Lang, said they wanted to take a closer look at the little-studied phenomenon of strategic default behavior as it relates to first- and second-lien mortgages.

“Predicting mortgage losses has become more difficult with the increase in strategic default behavior and the increase in loan modifications,” the paper said.

Our current accounting fantasies encapsulated in amend-extend-pretend is based on mythical loss recoveries based on past behavior. The study periods do not include times like now — when strategic default is a good idea. Strategic default is going to be much more severe than ever before, and banks are going to lose much more money than they currently project. When amend-extend-pretend becomes a crisis, when the banks lies are fully revealed, lenders will say their fraudulent accounting projections were based on past data. The actual performance didn't match past projections due to the housing bubble. No kidding.

“Focusing on mortgage defaults, our results indicate that the default rate for first mortgages far exceeded those of the second-lien mortgages during the financial crisis. This behavior was not observed in the pre-financial crisis period (i.e., the booming period of 2004-2006).”

About 20% of borrowers in the process of foreclosure due to defaults on the first mortgage kept their second-lien mortgage current. Among those who defaulted on their second-lien mortgages, about 80% also defaulted on their first-lien mortgage.

Data for the study came from a large random sample of individual credit records drawn at the end of each quarter from Equifax, a national credit bureau. The authors only studied consumers who had one first mortgage and at least one home equity line of credit or home equity loan over the period beginning in the fourth quarter of 2004 and ending in the second quarter of 2010. The study merged the Equifax data with another database of loan-level data from LPS Applied Analytics.

The data contradict the hypothesis that consumers would strategically default on a second lien and keep their first lien current to reduce their monthly payment and thus avoid a foreclosure, the white paper said.

That is what I thought would happen.

Instead, a far larger number of households do the opposite; that is, they default on their first lien — thus risking a foreclosure — while keeping their underwater second-lien mortgages current.

The reason?

The authors hypothesized that borrowers have incentives to keep their second lien current — after having stopped paying their first mortgage — in order to maintain their access to credit through the HELOC.

I think that conclusion is highly suspect. Most of these people likely don't have a HELOC they can access because they are underwater.

The study also found that the size of the unused line of credit is an important factor. Homeowners with larger credit lines are less likely to default, as they are motivated to maintain their access to the credit line.

That sounds more reasonable. For people with equity, access is merely having liquidity. Of course, homeowners with larger credit lines and plenty of equity probably don't need to borrow much money and aren't in as much financial distress as those who are maxed out.

Like other studies and white papers, this one also found that negative equity is a big driver in strategic default.

“A large portion of first mortgages with estimated LTV (loan-to-value) ratios greater than 100% is still current, but the continued willingness and ability of these homeowners to make their mortgage payments is subject to great uncertainty,” the authors wrote.

The paper also noted that banks are not punishing borrowers who default on their first mortgages by limiting access to their home equity lines of credit. That could be due to poor risk management practices or lack of timely updates on consumer's risk scores, the paper said.

“Most of the HELOC lines were not increased or decreased after the borrowers defaulted on their first mortgages,” the paper said. “About 90% of the lines remain unchanged even after three quarters following first mortgage default. Interestingly, a small percentage (3% to 6%) of these borrowers had their HELOC lines increased.”

I find it astonishing that people who default don't have their credit lines frozen immediately. Isn't continued borrowing after a default a good sign that a borrower has gone Ponzi? Banks can't be that stupid, can they?

Lenders have the right to foreclose in defaults of first- or second-lien mortgages.

Given the large number of current homeowners with negative equity, there are likely a large number of borrowers who could default on their home equity loans without being forced into foreclosure, the paper noted.

“The data indicate, however, that borrowers rarely engage in this strategy even though it appears to be viable.“

Although homeowners could default on their second-lien mortgages, lower their mortgage payment, and stay in the home, the loan contract stays valid and unpaid interest payments would keep accumulating. Should the house be sold, the second-lien creditor would be eligible for the recovery after the first-lien creditor is paid, the paper said.

Perhaps it is this last point that stops more people from defaulting on their second mortgages. Perhaps borrowers really do recognize that second mortgage debt is just like a credit card that follows them after they leave the house. If people accept that they can't escape the debt without bankruptcy, and they are unwilling to give up access to credit, then they will keep paying their second mortgages to keep the credit lines alive.

How did they spend their house?

I can 't give you a detailed story on how this family buried themselves with mortgage debt. I'm sure their entitlements demanded they spend copious amounts of cash. This house was purchased back in 1993 for $255,000, and it went into foreclosure being worth three times as much. We all know how that happens. Unfortunately, the sordid details are missing from my data source. Whatever they did, we can assume it was typical of the others I have profiled and leave it at that.

-$715 ………. Tax Savings (% of Interest and Property Tax)

-$684 ………. Equity Hidden in Payment

$260 ………. Lost Income to Down Payment (net of taxes)

$87 ………. Maintenance and Replacement Reserves

============================================

$2,607 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$6,950 ………. Furnishing and Move In @1%

$6,950 ………. Closing Costs @1%

$5,560 ………… Interest Points @1% of Loan

$139,000 ………. Down Payment

============================================

$158,460 ………. Total Cash Costs

$39,900 ………… Emergency Cash Reserves

============================================

$198,360 ………. Total Savings Needed

Property Details for 28 YORKTOWN Irvine, CA 92620

——————————————————————————

Beds: 4

Baths: 2 baths

Home size: 1,918 sq ft

($362 / sq ft)

Lot Size: 4,758 sq ft

Year Built: 1977

Days on Market: 44

Listing Updated: 40526

MLS Number: S638130

Property Type: Single Family, Residential

Community: Northwood

Tract: Ip

——————————————————————————

INVESTOR OWNED FORECLOSURE, INCREDIBLE OPPORTUNITY ON THIS QUIET CUL-DE-SAC HOME!! This home just had a $70K remodel and is totally turnkey. It has never been lived in since the remodel. Spacious private master suite, w/ walk-in closet. Three other larger than average bedrooms w/ mirrored closets. The complete kitchen remodel will be the pride of you at home gourmet with its New Appliances, Granite Counters, Stone Floor, & Custom Cabinets. The living room features soaring cathedral ceilings & a cozy Travertine fireplace. The bathrooms are completely remodeled including under mount sinks, Granite Counters, New Fixtures, and Custom Cabinets. The ceilings have been scraped, Canned lights, 4' Base boards, Crown Moulding, Plantation shutters, New carpet, & New designer paint throughout. Extra large 3 car garage has direct entry to the home. A great location just steps from Northwood Park.

Irvine isn't the only community that thinks it's special and their house prices are immune to decline. Today we look at the small Orlando suburb, Celebration, Florida.

The last place I lived in Florida before moving to California was the Disney creation, Celebration, Florida. I had just sold my house in Leesburg, Florida, and my soon-to-be wife and I rented the apartment (now condo) above Max's Cafe downtown. It sold me on living in planned communities.

Celebration, Florida, is a small suburb of Orlando. The property was designed and developed by the Disney Company on their own land under principals set down by Walt Disney himself. Celebration was Walt Disney's utopian vision of the perfect American life.

After living there for a year, I felt they did a wonderful job of creating a small town in large and growing metropolis. Particularly if you lived at or near the downtown like we did, you had recreation, dining, and entertainment in an enjoyably walkable place.

(mine was in the building on left, middle of three with large white awnings over the corner restaurant)

Celebration has much in common with Irvine. Both communities were developed by a single landowner ensuring a consistent level of quality throughout. Both communities were marketed at a more affluent move-up buyer but smaller products at lower price points provided a nice mix of owners. Both communities also saw house prices inflated dramatically during the housing bubble.

So where is Celebration different from Irvine. Irvine must be special because Celebration's house prices have crashed while Irvine's have held up. It must be different here, right?

Walt Disney Co. built Celebration, Florida, as an idealized version of a circa-World War II small town, where litter-free streets are lined with white picket fences and front porches entice neighbors to sit after dinner.

Now, there’s trouble in the 16-year-old paradise set within earshot of the nightly fireworks at Walt Disney World Resort.

Celebration’s foreclosure rate is about double the state’s pace as homeowners who paid a premium for a vision of utopia fall behind on their mortgages. Earlier this month, a resident on the verge of losing his house shot himself after a 14-hour standoff with police. Three days before that, the town had its first murder when a man was bludgeoned with an ax.

Celebration had everything going for it making even the most insane prices seem like a logical recognition of value by the market. There was no reason to believe house prices would decline in Celebration except for the fact that prices were way too high.

“A lot of people bought homes in Celebration thinking Tinker Bell had sprinkled the town with pixie dust,” said Michael Olenick, chief executive officer of mortgage-data firm Legalprise Inc., referring to the character in Disney’s “Peter Pan” movie whose magical dust allows people to fly as long as they think happy thoughts. “Reality is hitting hard.”

The foreclosure rate in Celebration since the beginning of 2009, based on notices of so-called lis pendens that initiate a case, is one for every 20 residents, compared with one per 48 people in Florida as a whole, according to Legalprise, in West Palm Beach. Celebration home values have dropped as much as 60 percent from the 2006 peak, while statewide values are down 51 percent, data from Seattle-based research firm Zillow Inc. show.

That is astonishing to me that a premium community could fall so hard. Celebration is great. Desirability is not causing prices to crater there.

‘Fantasyland’ Premium

Celebration foreclosures are happening at a faster pace in part because property owners in financial trouble are walking away from vacation homes in the town, where real estate sells for about 30 percent more than surrounding communities, said Olenick. Before the recession, people were willing to pay more for living in a Disney “fantasyland,” he said.

“The harsh reality is, bad things happen in Celebration too, both in real estate and in life,” Olenick said.

It's a good thing those bad things don't happen here.

… Disney started building Celebration in 1994, and the first residents arrived in 1996. Located on the southern border of Disney World, 25 miles south of Orlando, it was designed by Robert A.M. Stern, dean of the Yale University School of Architecture, and Jaquelin Robertson, a founding partner at Cooper, Robertson & Partners in New York. The style of the development is called New Urbanism, also known as neotraditionalism, emulating 1950s mixed-use neighborhoods where it was easier to walk than to drive.

Kilwin’s, Woof Gang

In the center of town, bordering a lake constructed by Disney, stores include Kilwin’s, a seller of ice cream and fudge, and the Woof Gang Bakery, where dog owners buy gourmet treats. At the Market Street Cafe, there’s an old-fashioned soda counter where diners can order the restaurant’s specials: meat loaf and chicken pot pie, followed by apple or pecan pie.

Lexin Capital, a New York-based private real estate investment firm, bought the 18-acre Celebration downtown from Disney in 2004. Mike Nunez, a spokesman for the company, didn’t return calls seeking comment. Disney still owns some commercial property in the town, according to Marilyn Waters, a spokeswoman for the Burbank, California-based company.

I find it interesting that Disney sold the downtown. It was not a great commercial center when I was there prior to the bubble, but the lack of foot traffic was likely due to the shortage of households in the early stages. Disney took a risk developing the commercial before the residential was there to support it.

Twice the Value

Living 12 minutes from Disney World’s Magic Kingdom, with a backdoor access road, comes at a price. Buying in the 10,000- person town requires paying what locals call the “Celebration Premium.” The median home value, including single-family properties and condominiums, was $250,800 in October, almost twice the $127,300 for the entire state, according to Zillow.

Sounds like Irvine and the "Irvine Premium," doesn't it?

Properties in Celebration are priced as high as $3.9 million for a six-bedroom, 8,000-square-foot (743 square-meter) mansion on a three-quarter-acre lot, according to Realtor.com. At $529,000, buyers could get a four-bedroom, 2,800-square-foot home with a wrap-around porch on about a sixth of an acre.

For condominiums, $90,000 will buy a two-bedroom, 1,000- square-foot unit, according to Realtor.com. At the top of the market, a five-bedroom, 3,400-square-foot, townhouse-style condo is priced at $675,000.

Four years ago, at the height of the real estate boom, the least expensive single-family house in the June to December period sold for $350,000, according to Kathleen Carlson, owner of Imagination Realty in the town’s center. In the same period this year, it was $210,000, she said.

The lowest condominium sale in the boom was $193,000, compared with a sale at $70,000 for the 2010 period, she said.

On a percentage basis, condos rose more and fell more than larger single-family detached properties. Of course, many of the mid to high end properties have not hit bottom yet either.

Town Maintenance

All owners pay about $860 a year for private trash pickup and recreational facilities, including parks, community pools and baseball fields. Condo owners pay an additional maintenance fee that varies depending on location.

The town’s Architectural Review Committee maintains strict control over the appearance of properties, dictating paint colors, regulating holiday decorations and overseeing the size of political signs that can only be posted in the 45 days leading up to an election.

Most residents see the rules as “protection,” said Carlson, who lives in a Celebration home with a wide front porch where she drinks coffee with neighbors on Sunday mornings.

“Most of us came here not because of Disney — we came because we wanted that type of control over our neighborhood,” Carlson said, “You don’t have to worry that your neighbor will suddenly start parking an old pickup on his front lawn.”

Isn't that Irvine? People don't come to Irvine to seek freedom to do whatever they want with their properties. People buy here because they know they aren't going to devalue their property, and they want neighbors that won't hurt values either. The HOAs get larger, take on more maintenance responsibilities, and stop homeowners from painting garish colors or parking cars up on blocks in the front yard.

Six Acceptable Styles

Like Carlson’s house, most properties have front porches that encourage neighborliness. There are six accepted historical architectural styles for homes: Victorian, Classical, Colonial Revival, Mediterranean, French, and Coastal.

While white picket fences outline most front yards, not everyone is allowed to have them. That would look too fake, said Laura Poe, a spokeswoman for the town. The architectural committee decides who can have the old-fashioned fences and who must have short, trimmed hedges.

The town shows its Disney heritage in annual seasonal shows, each with special effects originally designed by the entertainment company. In October, leaf-shaped confetti shoots out of lamp posts in the village center to simulate colorful falling foliage. During the month of December, the posts emit what locals call snoap — soap suds that look like snow.

Unlike in real life, the snow falls four times a night, on schedule, and dissipates without shoveling.

“Two of my grandchildren think we live inside Disney World, with Mickey Mouse,” said Celebration resident Sessoms, referring to a four-year-old and a five-year-old. “Except for the recent violence, I can understand why they would think that.”

Irvine is Celebration, minus the price crash. Will Irvine continue to escape the carnage? Perhaps we have less debt and fewer debtors here?

She borrowed and spent every penny she could get

The owner of today's featured property really became adept at raiding the housing ATM. She stopped paying about two years ago, but the property is only now making it to market. This one only hid in shadow inventory for about six months after the bank bought it. They probably couldn't find the right renter and decided to sell.

This property was purchased at the bottom of the last housing bubble. She paid $241,000 on 9/12/1997. She used a $202,000 first mortgage and a $39,000 down payment. She didn't want to wait long to get back that down payment money.

On 1/15/1998 she obtained two a stand-alone second mortgages for $25,000 and $16,000 respectively.

On 8/12/1999 she refinanced with a $294,000 first mortgage. Less than a year into the house, and she managed to withdraw her down payment plus $53,000.

On 2/21/2001 she obtained a stand-alone second for $75,000.

On 10/10/2002 she refinanced the first mortgage for $374,000.

On 7/3/2003 she refinanced again with a $454,500 first mortgage.

On 8/29/2003 she refinanced with a $456,000 first mortgage.

On 12/18/2003 she obtained a $100,000 HELOC.

On 1/4/2005 she refinanced with a $600,000 first mortgage and a $150,000 stand-alone second.

On 12/9/2005 she refinanced with a $680,000 first mortgage and a $170,000 stand-alone second.

Total property debt was $850,000.

Total mortgage equity withdrawal was $648,000.

She squatted for about 15 months.

Foreclosure Record

Recording Date: 10/02/2009

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 05/04/2009

Document Type: Notice of Default

She quit paying in late 2008 or early 2009, probably when she saw the housing ATM was turned off for a while. The bank foreclosed on 5/10/2010 for $749,912. For the last 6 months, they have been "processing" this REO.

According to the listing agent, this listing is a bank owned (foreclosed) property.

BACK ON THE MARKET!!! Don't miss out on this beautiful home located in the Westpark area features 3 bedrooms plus a bonus room, large master bedroom with walk in closet, upstairs laundry room, fireplace in living room, 2 car attached garage, and much more! .

.jpg)

.jpg)