NOT A SHORT SALE!!! Single level home with no one above or below. Situated in one of Irvines most sought after communities; the Terrace. Home is at the end of a cul de sac with an oversized driveway and a two car attached garage with direct access to the house. There are three large bedrooms and one has a secluded small patio/atrium. There is a large patio off the living area with plenty of room to entertain. The kitchen has an eat-in area and plenty of counter and cabinet space. This lovely home is surrounded by greenbelts and this family community has two pools, a club house, lots of walking trails and tot lots for the little ones to play in. Walking distance to Irvines award winning schools (Uni High is also very close), stores and parks. Also close to the 405 and 5 and toll roads. The beautiful beaches of Orange County are a few minutes drive away. Hurry, this one will not last.

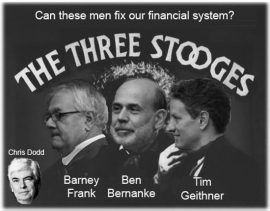

Back in 2009, I posed the question: Who will fix the System? The balance of power in Washington shifted in the last election. A new debate over the future of the GSEs and the housing market is just beginning. Let's take a fresh look at the gentlemen who will be deciding the fate of the housing market.

Obviously, those guys didn't get it done. Who's next?

Wed Jan 5, 2011 4:31pm EST — Reporting by Corbett B. Daly; Editing by Leslie Adler

{To avoid giving you pages of italics to read, the remainder is from the article}

(Reuters) – The Obama administration is set to unveil its proposal for an overhauled system of U.S. housing finance by the end of this month.

The administration's plan will just be a starting point. Congress is expected to debate the issue thoroughly before making changes to the current system, centered around ailing mortgage finance giants Fannie Mae and Freddie Mac.

Differing views on the merits of the current system among Republican and Democrats suggest the debate will be lively.

The following is a list of some of the key players in the debate:

U.S. Treasury Secretary Timothy Geithner:

Geithner, a former president of the New York Federal Reserve Bank, played a key role orchestrating bank bailouts during the financial crisis

He also was instrumental in the administration's push for sweeping Wall Street reforms last year, which did not address Fannie Mae and Freddie Mac. The mortgage finance companies have received more than $150 billion in direct taxpayer support since being placed in a government conservatorship in 2008.

At an event on the future of housing finance last August, Geithner sketched out some basic tenets of the administration's likely approach, but offered no details.

“It is not tenable to leave in place the system we have today. We will not support returning Fannie and Freddie to the role they played before conservatorship, where they fought to take market share from private competitors while enjoying the privilege of government support,” he said.

“I believe there is a strong case to be made for a carefully designed guarantee in a reformed system with the objective of providing a measure of stability in access to mortgage finance even in future economic downturns.”

Treasury Undersecretary Jeffrey Goldstein:

Goldstein is a former private equity executive tasked with being the administration's liaison to Wall Street. Goldstein has kept a low profile since taking office in 2010, though housing finance reform is expected to be a key component of his portfolio. In a July blog post on the White House website, Goldstein stressed “the vital importance” of the housing market to “our country's future,” but steered clear of any specifics.

Federal Housing Administration Commissioner David Stevens:

Stevens is a former executive with Long and Foster, the largest independently held residential real estate company in the United States, and has worked in top positions at Wells Fargo and Freddie Mac. Stevens is credited with shoring up the finances of the FHA by hiring the agency's first chief risk officer and tightening lending standards. Loans backed by the FHA account for close to 20 percent of new mortgage originations. Stevens wants to reduce the FHA's role in the mortgage market from those elevated levels.

Treasury counselor Gene Sperling

Sperling is currently a counselor to Geithner, but is in the running to be named as President Barack Obama's chief White House economic adviser, a post he held in the 1990s under President Bill Clinton. Sperling is known as a capable coordinator for economic policy. He spent a significant amount of his time at Treasury on initiatives aimed at boosting small business lending, though the programs had limited success.

House Financial Services Committee Chairman Spencer Bachus:

The soft-spoken Alabama Republican is quite a change, in both style and substance, from his predecessor, the outspoken liberal Barney Frank. Bachus believes the United States needs to be weaned from its reliance on government funding of mortgages. “What we now have is an addiction to government funding of mortgages,” Bachus told Reuters late last year. He has also said the two firms should be in “liquidation,” not “conservatorship.”

House Republican Conference Chairman Jeb Hensarling:

Hensarling, from Texas, is a conservative Republican who has been a vocal critic not only of Fannie Mae and Freddie Mac, but of any government support for the U.S. housing market. He holds the No. 4 Republican leadership post in the House of Representatives.

“Fannie and Freddie were not born of a competitive marketplace, but in a government laboratory. They were allowed to exploit their implicit government guarantee to take on enormous risks. These two entities expose the taxpayer to unlimited risk and will likely end up receiving the mother of all bailouts,” Hensarling said in a statement on his website.

Rep. Scott Garrett, chairman of the House Financial Services subcommittee on capital markets and government-sponsored enterprises:

Garrett, a New Jersey conservative Republican, this year takes the helm of the subcommittee responsible for oversight of Fannie Mae and Freddie Mac. He wants to wind down the firms within two years, a more radical position than even many of his Republican colleagues hold.

Senate Banking Committee Chairman Tim Johnson:

The Democratic lawyer from bank-friendly South Dakota is more conservative than his predecessor, Christopher Dodd, who retired last year. Johnson underwent brain surgery in 2006 and came away healthy, but with impeded speech. He has recovered and was present through the all-night talks leading to passage of the Dodd-Frank revamp of Wall Street regulation. Johnson is expected to take a go-slow approach to Fannie Mae and Freddie Mac, holding a number of hearings to gain a thorough understanding of their complexity before putting forth any specific Senate proposals. Keywords: USA HOUSING/PLAYERS

Senate Banking Committee top Republican Richard Shelby:

Another conservative Republican, Shelby has been a vocal critic of Fannie Mae and Freddie Mac. Late last year, he blocked Obama's pick to be the regulator of the two government-sponsored enterprises. Shelby accused the nominee, North Carolina's commissioner of banks, Joseph Smith, of being a “tool” of the Obama administration who would throw government money at the mortgage market and send the bill to taxpayers.

Fannie, Freddie acting regulator Edward DeMarco:

DeMarco is a career civil servant who has been acting director of the Federal Housing Finance Agency since August 2009. He had been expected to be replaced by Smith, but with the nomination blocked, he could stay in the acting role for some time. DeMarco is very focused on limiting taxpayer losses from Fannie Mae and Freddie Mac and has the power to exert substantial influence over how the two firms conduct their business.

House Financial Services Committee top Democrat Barney Frank:

Frank, a key architect of the financial regulation law that bears his name, lost the gavel of the House Financial Services Committee when Republicans took control of the House. However, as the panel's top Democrat on the key House committee responsible for Fannie Mae and Freddie Mac, he is likely to still wield considerable influence. He is a key ally of the Obama administration.

Frank has said the GSEs should be “abolished” in “current form” and a new housing finance system should be created. At the same time, he has stressed the importance of developing a new system before shutting the two firms down. “You can't really tear down the old jail until you've built the new one,” he has said.

{End of article}

I know this stuff is a bit wonkish, but it is good information to know. We will see these guys pontificate in debates over the next 18 months on the fate of the GSEs. Don't underestimate the importance of the GSEs to the housing market. Most middle-class mortgages are GSE insured. High wage earners often borrow from a jumbo loan lender because their loans exceed the $729,750 loan limit at the GSEs and FHA.

Whatever happens to the GSEs matters to Irvine.

If they are dismantled, and if the home mortgage interest deduction is scaled back, the cost of borrowing will rise and the amounts borrowed will go down. That will put continued pressures on pricing. House price increases require greater borrowing, and with interest rates and other costs working against borrowing, house prices will likely stagnate for a very long time as these subsidies unwind.

Japan had more than 20 years of real estate deflation. What if we had 20 years of real estate stagnation?

Don't worry. We will probably print enough money to create all kinds of inflation including wage inflation. That will put house prices back on a steady upward march in 2 to 5 years. Hopefully, in order to save house prices, you aren't paying $14 per gallon for gas and gold is selling for $3,200 an ounce. My guess is Bernanke will error on the side of over-printing.

It was a great bull run

I do feel a hint of jealousy when I see homeowners like today's. They bought at the bottom of the last real estate recession on 7/31/1997 and paid $283,000 for this house. They borrowed $226,400. A few months later they borrowed $28,000 of their equity, probably to do some necessary renovations. On 9/10/2001 they had $247,000 in debt in a new first mortgage. The refinanced two more times, but the final mortgage is for $238,500 which puts them near their entry point.

They did not borrow anything extra when given plenty of opportunities.

Great job.

I can't give them an A because their mortgage balance is larger than when they started. I am giving them a B instead of a C because I believe the increase was a modest renovation cost. After their mortgage increased initially, it went downward to where it is now.

When they sell this house at bubblish prices, they stand to get a check from escrow for nearly $450,000.

Wouldn't that be a cool check to cash?

These owners obtained significant wealth advantage from fortuitous timing in the housing market. They missed the peak for maximum sale, but with their diligence to pay down the mortgage and the huge run up in prices, they get the pot of gold.

We have seen plenty go the other way….

They passed on all temptations and diligently paid down their mortgage at a time when everyone else was seeking ways to maximize borrowing to obtain free money to spend.

AWESOME REMODEL….NO STONE LEFT UNTURNED! Walk into this home and feel the rich, warm welcome! Remodel just completed includes gourmet kitchen with granite counters, rich, dark wood cabinetry, gas cooktop, electric oven, microwave/convection oven and roll out center island. All baths have been remodeled with granite counters, new sinks, faucets, lighting, etc. Walk behind wet bar in family room for entertaining features granite counter too. Great floorplan with breakfast nook and large family room off of kitchen. Rich wood and tile floors, chair rails, crown molding, wainscotting, custom paint and more. Master bedroom has walls of bookshelves and storage space with walk in closet, master bathroom with granite counters, double sinks and more. Very private backyard with tons of color, potting shed, patio area AND secluded spa with sitting area. All of this and Northwood High School too!!!

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

Over the last couple of years, a few academics have been making the case that land-use regulation is the cause of the housing bubble. Most of the post that follows summarizes their argument.

I think they are only partially correct. Land use regulations do restrict supply, and therefore they do impact prices. As I noted in The Great Housing Bubble:

Speculative bubbles are caused by precipitating factors.[1] Like a spark igniting a flame, a precipitating factor serves as a catalyst to begin the initial price increases that change the psychology of market participants and activates the beliefs listed above. There is usually no single factor but rather a combination of factors that stimulates prices to begin a speculative mania. The Great Housing Bubble was precipitated by innovation in structured finance and the expansion of the secondary mortgage market, the lowering of lending standards and the growth of subprime lending, and to a lesser degree the lowering of the Federal Funds Rate.

Supply shortages caused by land use regulations can cause short-term volatility in prices. The perception of a chronic real estate supply shortage in California helps sustain prices at the high levels of income debt support. The initial price rally caused by the shortage can serve as the precipitating factor causing the irrational exuberance to take over. It is the irrational exuberance and creative financing that causes the housing bubble.

So when these academics proclaim that land use regulations cause housing bubbles, they are as correct as saying matches cause forest fires. The match may start the flame, but the flame consumes the forest for a variety of other reasons not explained by the initial spark. Similarly, housing bubbles may be precipitated by a supply shortage causing a price rally, but it is the irrational exuberance of buyers thinking prices will go up forever that gives housing bubbles their strength. The full rise and fall of bubble pricing is not explained by the supply shortage alone.

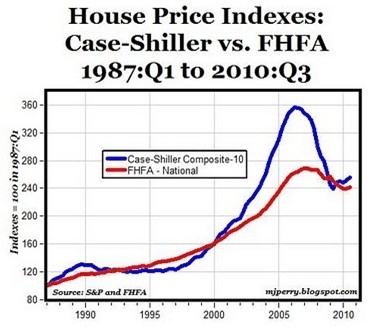

As bad as last week's housing data was, the 20 cities that comprise the Case-Shiller Composite Index are not representative of the entire United States housing market. In fact, the United States housing bubble/bust was confined to only a minority of cities. To illustrate this point, first consider the below chart (courtesy of Carpe Diem), which compares the 10-City Case-Shiller Composite Index against the FHFA House Price Index based on 50 states:

As you can see, the United States housing bubble/bust was confined, to a large extent, to the 10 cities making up the Case-Shiller 10-City Composite Index: Boston, Chicago, Denver, Las Vegas, Los Angeles, Miami, New York City, San Diego, San Francisco, and Washington, D.C.

So why was there so much variability in house price performance between United States cities, with some cities booming then busting while other cities remained relatively stable? It certainly wasn't due to liberal lending policies (easy credit), since essentially the same lending conditions were available across the United States. It wasn't because of differences in population growth, since states like Texas, which has experienced the highest population growth over the past 10 years, never had a housing bubble/bust. Rather, the differences in house price performance are accounted for by the way in which these markets regulate land use.

No. His conclusions are completely wrong. The key difference that made Texas stand out was not its less restrictive land use, it was the difference in laws pertaining to HELOCs and cash-out refinancing. Read my detailed argument here: Desire for Mortgage Equity Withdrawal Inflated the Housing Bubble.

The below table, which comes from Demographia's 6th Annual International Housing Affordability Survey, shows the extent to which the various housing markets employ restrictive land use regulations.

Restrictive land use regulation, often referred to as “smart growth,” “growth management,” or “new urbanism,” refers to policies that force people to live in higher densities while significantly restricting the expansion of suburban residential development. Measures include, but are not limited to, urban growth boundaries, areas declared off-limits to development, building moratoria, development fees and charges, and excessively large minimum lot sizes.

These academics are making themselves correct by how they define “restrictive” land use. The devil is in the details and the definitions. How should we compare the land use regulations of Texas and California? How do we determine if one place is restrictive and another permissive? How much of the data is subjective evaluations of regulatory effects subject to a wide degree of interpretation?

The data gathered by these researchers presented in different forms all boil down to the same subjective evaluations of land use regulations. If you agree with their assessment, then you will agree with their conclusions.

Cities that have adopted liberal market-based approaches (“more responsive land regulation”) have experienced relatively stable housing markets, whereas those that have implemented prescriptive land use regulations have experienced volatile boom/bust cycles.

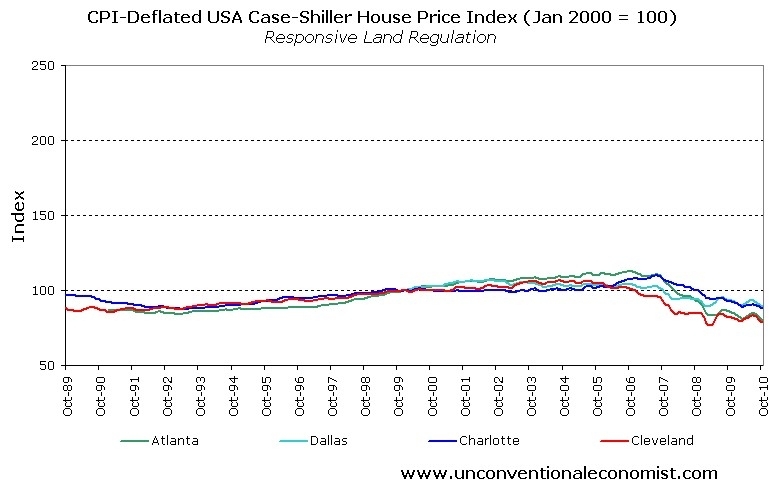

To illustrate this point, first consider the below chart, which plots the CPI-adjusted house price performance of the cities included in the 20-City Case-Shiller Composite index and deemed by Demographia as having “more prescriptive land regulations.”

As you can see, prices have been highly volatile, with all cities experiencing wild boom/bust conditions.

Now consider prices in the cities within the 20-City Case-Shiller Composite Index with “more responsive land regulations.”

As you can see, real house prices have remained relatively stable in the supply-responsive cities.

The situation is similar at the state level using FHFA housing data. First, consider the states with “more prescriptive land regulations”:

Now consider states with “more responsive land regulations”:

Again, it's the same story, with the highly regulated states experiencing wild boom/bust cycles whilst prices in the market-oriented states remained relatively stable.

If you accept their methods of classifying land use regulations, then you will agree with their findings. If not, you won't. Garbage in, garbage out.

Economics 101

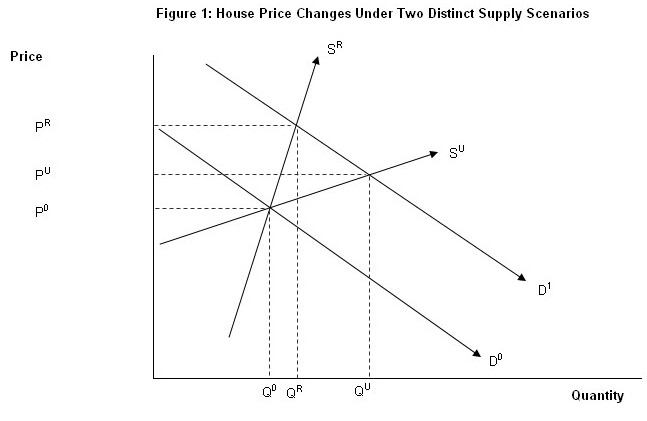

The economic forces underpinning the above findings are perhaps best explained through basic supply and demand analysis. Consider the below chart taken from an earlier article on this issue.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU (unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as that brought about by a significant relaxation of lending standards, the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0 to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp rise in unemployment, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

The key point is that increases (declines) in demand can bring sharply rising (falling) house prices when supply is constrained. However, when land supply is not regulated, it adjusts to demand and house price volatility is reduced.

The effect on markets in the short term is how they describe above. However, that only explains the first stages of a market rally. Once prices are high, and they have been rising long enough for people to take interest, the market needs help in order to keep going higher. It is financial innovation folly that must take over to build a significant real estate bubble.

These observations are consistent with those of Glaeser and Gyourko, who summarised the findings of a number of studies in this area:

Recent research also indicates that house prices are more volatile, not just higher, in tightly regulated markets …. price bubbles are more likely to form in tightly regulated places, because the inelastic supply conditions that are created in part from strict local land-use regulation are an important factor in supporting ever larger price increases whenever demand is increasing.

…. It is more difficult for house prices to become too disconnected from their fundamental production costs in lightly regulated markets because significant new supply quickly dampens prices, thereby busting any illusions market participants might have about the potential for ever larger price increases.

Learning history's lessons

As long as commentators focus primarily on the demand side of the housing market, whilst ignoring supply-side constraints, they will never fully understand the drivers of housing bubbles and busts. The resulting incorrect diagnosis will inevitably lead to poor policy prescriptions and outcomes.

By all means, let's crack down on the destructive speculation, predatory financing and financial alchemy that have fuelled the world's housing bubbles. At the same time, let's not ignore the supply-side barriers that have enabled the credit-fuelled demand to feed into skyrocketing house prices which, in the case of the United States, later collapsed once the artificial demand evaporated.

Readers seeking detailed information on issues pertaining to the supply-side of the housing market are encouraged to visit the Demographia and Performance Urban Planning websites. Also, please be advised that the 7th Annual Demograhia International Housing Affordability Survey will be released on 24 January 2011. It's sure to be another great read.

Having worked most of my career in the land development industry, I understand the desire to reduce land use regulations which hinder our ability to deliver housing. When we can't deliver housing, there are shortages and short-term price rallies. However, much of our land use regulation is good and should not be abandoned, and the likelihood of the regulations rolling back to some more permissive era is slim to none.

How to ruin a good cashflow investment with excessive borrowing

There was a time when banks were smarter about loaning money on cashflow properties. Besides an appraisal showing comparable sales, a process prone to bouts of irrational exuberance, lenders on rental properties also look at stabilized cashflow to determine if the cashflow from the property can cover the loan payments in the event of foreclosure.

During the Great Housing Bubble, lenders did not bother to check actual cashflow. During the savings and loan disaster, developers had to make up rosy financial projections to demonstrate income in order to get lenders to approve the loan. During the bubble, since lenders thought they were passing the risk on to others in mortgage-backed securities, lenders did not care about whether or not the cashflow covered the income.

At some point after this property was purchased and before the owner went Ponzi, rents rose enough to make this property cashflow positive. By 2002, this was finally a profitable rental. At least until the owner started his borrowing spree which culminated in a $450,000 ARM.

The owner quit paying the ARM in mid 2008, and he is probably still skimming rent from whoever lives there.

According to the listing agent, this listing may be a pre-foreclosure or short sale.

This is an Approved Shortsale at $462,000 (was appraised at this price 2 weeks ago)we have until the 20th of January to close we wont accept anything less then $462,000, This is a Beautiful 3+3 Townhome, w one car garage and one covered carport.Last time we had 4 offers in 2 days, Previous Buyer paid for inspection an appraisel last minute decided to stay over sea's and not move to the U.SWe might need to use their lender since they have all paperwork and can close in 12 days approx. to make an offer or any questions please look at privete remarks.

we wont accept anything less then $462,000? Don't hold your breath waiting for my offer of $461,500.

Last time we had 4 offers in 2 days. Wow! What a great realtor….

By Al Yoon and Tom Hals — Mon Jan 3, 2011 3:51pm EST

NEW YORK/WILMINGTON, Del (Reuters) – Bank of America Corp's $3 billion settlement with Fannie Mae and Freddie Mac may have brought New Year cheer to the bank's stockholders, but now comes the hard part: settling far larger and thornier claims made by private mortgage investors.

After Monday's announcement, Bank of America still faces lawsuits stemming from $375 billion of mortgage-backed bonds.

Compared with the deal with government-backed Fannie Mae and Freddie Mac, those legal claims will be far more difficult and costly and the latest settlement does not change that, according to legal experts and lawyers representing investors.

“It's much more difficult to settle,” Jack Williams, a professor at Georgia State University College of Law, said of the investor lawsuits. “It's going to take a long time and it's going to take a lot of information.”

In other words, investors won't tolerate being ripped off if they have to lose money. If the losses are legitimate market losses, investors may have little grounds for recovery, but if the losses can be demonstrated as stemming from problems in the banks origination pipelines, then perhaps a few lawsuits will prevail. Its an uphill battle for investors to recover anything.

The banks were able to cut a favorable deal with the government because the banking lobby pays off everyone in congress through large donations. They have significant sway with key legislation with their lobbying might. Similar to the NAR.

The deal has little to do with justice or equity. It's looting government reserves by the banks.

The Federal Reserve is the supreme example of regulatory capture. The banks got together and created their own bank and said its edicts are not subject to government pressure. Governments controlling central banks has blown up before. But the banks are now their own regulator answerable to no one, not even Congress (unless Congress revokes their charter).

Talcott Franklin, a Dallas-based lawyer representing asset managers, hedge funds and other investors who have stakes in at least $600 billion of residential mortgage bonds, said the deal might be encouraging because it shows a willingness to resolve claims.

However, he noted Bank of America was particularly eager to settle with the two government entities, which purchase nearly all home loans currently sold by mortgage originators. Investors, in contrast, do not have the same profitable relationship with the bank or its rivals, he said.

Bank of America's stock jumped 5 percent on Monday as investors greeted the settlement as a sign the company would be able to contain demands that it buy back billions of dollars in soured home loans.

I never saw this as a real problem. The contracts for origination would have contained clauses with protections to prevent buybacks. The plantiff will have a high bar to hurdle to force the banking defendant to buy back the loans. The government was never going to force this issue, and the private investors may successfully sue in some instances, but a mass bailout of investors though bank buy-backs is not forthcoming.

In fact, if you look at the subprime lending model, the main reason risky lending was done through companies like New Century Financial instead of by the major investment banks was so that the investment banks could insulate themselves from the liabilities of loan buybacks. New Century went bankrupt facing billions in loan buyback obligations it could never hope to make good on. Goldman Sachs didn't want to face that risk.

Those loans were packaged into bonds sold as top-rated investments, but their shoddy construction became apparent when the U.S. real estate market suffered its worst crash since the Great Depression.

Investors ranging from hedge fund managers to several Federal Home Loan Banks have sued Bank of America and its Wall Street rivals and most want the banks to buy back the securities or loans backing them.

Money manager BlackRock Inc and bond fund Pimco are in talks with Bank of America over $16.5 billion of mortgage bonds they purchased.

Legal experts said the investor litigation will be tougher to resolve in part because the claims stemming from the loans sold to Fannie and Freddie may have been easier to settle.

The government-sponsored enterprises often had higher standards and well-understood eligibility guidelines for the mortgages they purchased. As a result, the lower quality loans were shipped off to other investors.

The people who bought GSE debt will be covered by the government, but investors who wanted an extra fraction in their returns opted for uninsured mortgage-backed securities. The risk was underpriced. The GSE investors will lose little or nothing. The private label investors are not merely enduring a lower return, they are often losing signficant percentages of their asset valuation. They are getting hit hard.

Williams, who has been researching legal issues surrounding mortgage securities, said Monday's deal may even wear down some of the resistance of bond trustees, who have been a hurdle to investor lawsuits.

That could lead to an increase in new complaints against the Wall Street banks, but he did not think Monday's settlement would expand the range of investors considering a lawsuit.

Investors also have a bit of momentum on their side, thanks to some recent court rulings.

MBIA, a bond insurer, recently overcame objections by Bank of America to the use of sampling from loan portfolios to prove the bank breached promises about the quality of its mortgage underwriting.

Bank of America had wanted MBIA to prove its case on a loan-by-loan basis, an incredibly expensive task in a lawsuit covering more than 375,000 mortgages.

Interesting legal posturing on both sides. MBIA wants to find the least expensive way to prove its claims, and the bank counters with the most expensive way to bog down the process.

In addition, the Federal Home Loan Bank of Pittsburgh recently overcame a motion to dismiss its case against several banks, including JPMorgan Chase & Co

Bank of America stockholders probably should not expect a settlement with private investors any time soon.

“It's going to take a long time, it's going to take a lot of information” to settle investor claims, said Williams.

And it will be handled one case at a time. The attorneys will be busy.

5 January 2011 — Greg Hunter, Creator of USAWatchdog

In case you have not heard, Fannie and Freddie (also known as Government-Sponsored Enterprises or GSE’s) settled a big lawsuit with Bank of America Monday. The case was settled for cents on the dollar, even though the GSE’s had had a strong case to force B of A to buy back billions in sour mortgage-backed securities (MBS.) I wrote about some of this in a December 1 post called “Foreclosure Bombshell.” The post was about some of the legal trouble Bank of America was having with the mortgage debacle and the possibility of the banks being forced to buy back billions in sour MBS. Here’s part of what I wrote back then, “Mortgage-backed securities have to meet what is called “contractual representation and warranties.” That basically means the MBS are required to be free of fraud and be exactly what the seller says they are. Do you think mortgage-backed securities are free of fraud? Do you think these securities are the triple-A rated risk free investment the big Wall Street banks claim?—NO WAY! The banks are going to be forced to buy back all the toxic mortgage junk they sold.(Click here to read the entire post.)

Unfortunately, the “fraud” in these mortgage-backed securities pools was the underwriting standards often printed in bold on the front cover. The fraud was on its face. The real hurdle investors have to overcome is whether or not the losses were from loans that should not have been in an already tainted pool. A huge number of loans were going bad anyway, the lawsuit would be about the difference created by fraud.

On Monday, after news of the Fannie and Freddie settlement, I got a gloating comment from a reader named “Rick.” Rick tells me he’s retired from the “finance industry.” Here’s some of what he wrote, “I told this would be nowhere as bad as most made out. Hope you read about the settlement with the GSE’s With BofA, 1.3b, this makes BofA total exposure probably around 3b going forward, not the 50B+, everyone thought. Additionally, B of A audit by Moody’s and others has been complete and found that Loan doc’s were delivered. PIMCO will settle for very little in the coming weeks and AG’s to follow. NO Conspiracy and Fraud as you have promoted on your blogs, just very bad process. As stated in our last exchange, I hope you man up and write a new blog retracted and admitting you got a little carried away with you statements. This is what happens when you repeat from others and do not do your own homework. Just remember the fraud was committed buy the rating agencies not the Banks.” (You can read the entire exchange at the end of the Foreclosure Bombshell post.)

I’ll “man up”alright. Yes, Rick you were right, the American taxpayer got ripped-off once again. It was not that bad for B of A because it is another back door bailout for the banks that caused the mortgage mess in the first place. The headline over at Fortune/ CNNMoney.com says it all “Is Fannie bailing out the banks?” Of course, the answer is YES! The report goes on to say, “Monday’s arrangement, according to this view, will keep the banks standing — but leave taxpayers on the hook for an even bigger tab should a weak economic recovery falter. Sound familiar? ‘The administration is trying to weave a path between two bad alternatives,’ said Edward Pinto, a resident scholar at the American Enterprise Institute. “They want to bail out the big banks without doing apparent damage’ to the sagging U.S. budget position.” (Click here to read the entire Fortune/CNN report.)

By limiting BofAs responsibility, the government has taken the remainder onto itself.

This is an outrage, especially when you consider what kind of a sweet deal B of A got. Investing expert and owner of a blog called The Big Picture, Barry Ritholtz framed the B of A settlement this way, “Bank of America settled numerous claims with Fannie Mae for an astonishingly cheap rate, according to a Bloomberg report. A premium of $1.28 billion was paid to Freddie Mac to resolve $1 billion in claims currently outstanding. But the kicker is that the deal also covers potential future claims on $127 billion in loans sold by Countrywide through 2008. That amounts to 1 cent on the dollar to Freddie Mac. Imagine if you had a $500,000 mortgage, and you got to settle it for $5,000 — that is the deal B of A appears to have gotten from Freddie Mac.” Click here for the complete Ritholtz post.)

Maxine Waters, a senior Democrat on the House Financial Services Committee, also thinks taxpayers got a bad deal. The Congresswoman’s statement was included in a story from the Businessinsider.com. Representative Waters said, “. . . I’m fearful that this settlement may have been both premature and a giveaway. The fact that Bank of America’s stock surged after this deal was announced only serves to fuel my suspicion that this settlement was merely a slap on the wrist that sets a bad example for other negotiations in the future. I understand that the questions raised by fraudulent servicing practices were not addressed in these settlements, and I hope that Fannie Mae and Freddie Mac, along with their conservator, are more aggressive in pursuing banks for the fraud I documented in my Subcommittee during the last Congress.” (Click here for the complete Business Insider post.) The sad thing here is I don’t think this administration or any Republican administration will pursue the “fraud” Congresswoman Waters has documented. I envision every other major Wall Street bank that dumped its toxic mortgage-backed securities onto the GSE’s to also get a sweet deal at the taxpayers’ expense. Many more billions will be poured into the banks to prop them up when some are clearly engaged in malfeasance. Former bank regulator and professor of economics William Black has called for banks such as B of A to be dismantled in receivership. He co-wrote a piece last October called “Foreclose on the Foreclosure Fraudsters,” but what is happening here is just the opposite. Once again, incompetence and alleged crime is being rewarded. (Click here to read the William Black article.)

My only question is how long can the bailouts and spending go on? The banks will no doubt get another round of bailouts via the GSE’s, costing hundreds of billions of new dollars. In his most recent post, Jim Willie of Goldenjackass.com sums up the end result of the massive and ongoing bank bailouts in one chilling sentence. Willie writes, “The extraordinary efforts and attempts to save the big US banks will be the precise policy that leads to systemic failure and the US Treasury Bond default, all in time.” (Click here for the complete Willie post.)

Meanwhile, the Fed continues QE2 at a rate of $75 billion a month of pure money printing to finance the country. When QE2 is finished in June of 2011, how difficult will it be to get foreigners to buy our debt? QE3 anyone? I have a novel idea–the U.S will once again raise its debt ceiling. (Currently it stands at $14.3 trillion.) That will be painless for the politicians, and besides, nobody goes bust or gets punished in America anymore. We do not have leadership in this country; we have political hacks taking turns protecting their donors and cashing in—at the expense of the American people.

I think the government will continue to borrow and spend stimulus money, and the federal reserve will print money and hold down interest rates as long as it has to in order to ignite some price inflation. Hopefully, people will get many new, high-paying jobs to cover their increasing cost of living. I think it is more likely that the inevitable price inflation will pick its victims. Some will see wage increases to match the new cost of living, and some will not. What is your COLA?

Another knife catcher trapped by zero appreciation

California real estate is supposed to be a wellspring of unlimited amounts of free money. When prices don't rise and the populace cannot get their HELOC fix, the economy founders, and many borrowers get trapped in their homes.

The previous owners

The owners who went through foreclosure were typical Ponzis living the Irvine home price appreciation fantasy. They bought the property on 7/29/2003 for $399,000 with 100% financing. By 2/17/2005, about 20 months later, they managed to extract $150,000 in free money through continued refinancing.

Think about that: zero down, $150,000 in free money in 20 months. I want one of those… and so did the knife catcher.

The current owners

The bank took the property back from the Ponzis for $473,694 on 9/24/2007, and they sat on it for a full year before selling it to our current knife catcher for $390,500 on 10/1/2008. I imagine the owners thought they were getting a great deal. The house appraised for $550,000 at the peak, so they were getting a 30% discount.

Did they get an under-market steal? Or did they catch a falling knife?

This absolutely charming top level end unit is located in the prestigious golf course community of Rancho San Joaquin and has a large entry foyer that opens into the great room which has high ceilings and a custom fire place. This model has two master suites. Remodeled master bath and floors. For your enjoyment and entertaining this home has two balconies with quiet and serene views of tree lined streets. Near University of Califronia Irvine, Airport, freeways and great shopping. This is a great place to live, why not make it home.

Foreclosure is a painful but necessary part of the real estate cycle. Lenders have tried to delay this process as long as possible, but it is now going forward with renewed vigor.

US mortgage foreclosures jumped in the third quarter as fewer borrowers qualified for loan modifications that would have reduced their monthly payments, bank regulators have said.

The rise in repossessions and decline in loan modifications are further signs that problems in the US housing market are persisting, in spite of forecasts by some analysts of a recovery before the year-end.

The number of homes entering foreclosure rose 31 per cent compared with the second quarter and 3.7 per cent compared with the year-earlier period, according to the Office of the Comptroller of the Currency and the Office of Thrift Supervision.

2011: The Year of Foreclosure? Loan modifications failed. Short sale programs are proving ineffective, and cure rates are near zero. Foreclosure is the only remaining option to clean up this mess.

These newly foreclosed homes will add to a growing backlog of 1.2m properties in some stage of repossession, a 4.5 per cent increase over the second quarter and 10 per cent more than the previous year.

As of the end of the third quarter, 187,000 homes completed the foreclosure process, a 14.7 per cent increase on the second quarter and a 57.5 per cent jump from the same period a year ago.

As these properties come on the market, they are expected to depress home prices by between 5 per cent and 10 per cent during the next year.

That is a widely held position among real estate market watchers.

The regulators also found that home retention actions, such as interest and principal reductions, had fallen 17 per cent from the year earlier, mainly because of a sharp drop in modifications run by the government’s home affordable modification programme (Hamp).

Hamp modifications totalled 504,648 as of November, well short of the government’s 3m target.

Failure. Unqualified, unmitigated failure. Loan modification programs were a bad idea from the start. The only served to give false hope to people for a while and get a few more payments from zombie borrowers.

Even when borrowers receive loan modifications, they are redefaulting at high rates. According to a report by the Congressional Oversight Panel, 40 per cent of borrowers who receive a Hamp modification are expected to redefault over the next five years.

Bruce Krueger, the OCC’s head mortgage expert, said the decline in Hamp modifications was partially caused by the smaller pool of loans eligible for change.

The real problem is that so many people simply don't qualify because they aren't willing to cut back on their entitlements to make a mortgage payment. Remember, for 5 years, the house paid you to live in it. Paid handsomely. People became adjusted to that level of spending and now they must adjust. No fun.

But Mark Zandi, chief economist of Moody’s Analytics, said that explanation told only part of the story. The problem, he said, was the “inadequacy of loan modification programmes”.

Hamp must compete with private modification programmes offered by banks, which tend to provide borrowers with smaller reductions in interest and principal, thus making them more attractive to lenders and less helpful to distressed homeowners.

Competing with private loan mods? Is he kidding? Banks don't want to modify loans. Banks want to get all their money back plus interest. They need to make enough on the good customers to pay off the bad debts of the others. The created many Ponzis who are by definition, bad customers.

Banks want the government to take responsibilty for these bad loans under the HAMP program. The entire program was developed to take the garbage off the lender's books. Lenders are not offering better deals than HAMP except perhaps for a few choice customers. The riff-raff in the MBS pools can fend for themselves.

Another problem, said Mr Zandi, were second-lien holders. Many first mortgage lenders will write down the loan principal only if the balance on the second mortgage is also reduced.

But borrowers continue to make payments on second mortgages, which tend to be smaller and therefore more affordable, even when they fall behind on the first. As a result, second-lien holders had been unwilling to take part in modifications, creating a “big impediment”, Mr Zandi said.

The Treasury Department recently increased cash payments to mortgage servicers and lenders to encourage them to complete more modifications. But analysts said the government had so far done little to address the problems presented by second liens.

by JON PRIOR — Wednesday, December 29th, 2010, 3:34 pm

Large banks and thrifts foreclosed on 382,000 homes in the third quarter, a 31.2% spike from the previous quarter, according to the Office of the Comptroller of the Currency.

Foreclosures increased 3.7% from a year ago, and more are coming. There are 1.2 million homes in the foreclosure process as of the end of the third quarter, up 4.5% from the previous quarter and an increase of 10.1% from a year ago.

The OCC, which oversees the largest banks and absorbs the Office of Thrift Supervision in 2011, said lenders have picked up the pace of foreclosures to get through their backlogs.

The banks are finally picking up the pace to clear their books via foreclosure. Two thousand eleven will be the year of the foreclosure.

Still, 87.4% of the 33.3 million loans in the banks' portfolios were current and performing at the end of the quarter, which held unchanged from the previous quarter. While the amount of borrowers in 60-plus day delinquency dropped 6.4% from the previous quarter, mortgages between 30- and 60-days delinquent increased 4.3%.

The 60-day plus delinquency rate can go down as properties enter foreclosure. This is the backlog. The increase and new 30-day and 60-day delinquencies is troubling. The pipeline is getting larger.

But servicers reported more home retention actions than foreclosures in the third quarter. More than 470,000 borrowers received either a trial modification, permanent modification or shorter-term payment plans.

Of the modifications completed in the third quarter, 88% included a principal reduction to go with the interest-rate decrease, and more than 54% reduced monthly payments by at least 20%.

More recent modifications are performing better than earlier ones, too. For those completed in the fourth quarter of 2009, 20.2% were seriously delinquent after six months. For those made in the second quarter of 2009, 33.5% were seriously delinquent after the same amount of time.

Hurry! Sign up for your loan modification while they are giving away free money! Does is seem plausible to you that 88% of loan modifications had principal reductions?

Appreciation provides mobility

Housing market participants will endure long-term mobility problems as a direct result of the policies enacted in Washington to save the housing market. Rather than letting prices fall to their natural level and then begin to rise, government policy has engineered a false bottom that will delay sustained appreciation for 1 to 3 years trapping every debtor in their properties for an additional one to three years.

Today's featured property was purchased at the false bottom in early 2009. This owner has marked up the property to cover the commissions and pay for a renovation. Do you think they will get it?

Opportunity knocks, better than a brand new model home. Owners just spent $160,000.00 upgrading this gorgeous home and have to relocate. Cul-de-sac location with four bedrooms and 3 bathrooms. Main floor bedroom and bathroom. Private backyard next to the greenbelt. Brand new kitchen with thermador stainless steel appliances, Ceasarstone countertops, custom cabinetry. Brand new millwork windows and sliding doors with custom plantation shutters. New tile roof. Gorgeous hardwood floors. Crown moldings and built in office closet on the main floor bedroom. Brand new custom bathrooms. New Drywalls with bull nosed corners. Brand new water heater. And the list goes on. Just a short walk to shopping and restaurants, close to Northwood high school. No mello roos tax and low monthly association fee.

I know this stuff is a bit wonkish, but it is good information to know. We will see these guys pontificate in debates over the next 18 months on the fate of the GSEs. Don't underestimate the importance of the GSEs to the housing market. Most middle-class mortgages are GSE insured. High wage earners often borrow from a jumbo loan lender because their loans exceed the $729,750 loan limit at the GSEs and FHA.

I know this stuff is a bit wonkish, but it is good information to know. We will see these guys pontificate in debates over the next 18 months on the fate of the GSEs. Don't underestimate the importance of the GSEs to the housing market. Most middle-class mortgages are GSE insured. High wage earners often borrow from a jumbo loan lender because their loans exceed the $729,750 loan limit at the GSEs and FHA.