Today’s featured song was sent by a local musician who is an avid reader of the blog. I bet you can guess his name…

The crash at the end of a speculative bubble can be brutal. So far, the price decline in Irvine has been measured and orderly compared to the drops in less desirable markets. I was recently looking at properties in the Palm Springs market, and I found some of the new neighborhoods that were the carnage is simply breathtaking. Check out some of these listings at around 50% off their new home sales price of 2 years ago:

I could list more, but I think you get the point. The Palm Springs market may have some chance of recovery as baby boomers may want to go here when they begin to retire soon. If you want to see carnage in a market that is not likely to recover any time soon, take a look at Hemet/San Jacinto:

The interesting thing about all of these properties is that they are selling for less than replacement cost. With asking prices around $85/SF, that is the cost of construction of the box itself. Even if the lots were free, a builder could not build and sell a house on it and make any money. There will be no new construction in these markets until prices rise above replacement costs, and then it will only occur on already finished lots selling at an extreme discount. There will be no new development or construction of finished lots until prices rise back above $130/SF. That is about 50% above current values. As you can see, replacement cost does not put a floor below prices. Ultimately, the lack of new construction will create a shortage, and prices will rise due to supply constraints (assuming the financing is available). However, since we overbuilt in many of these fringe markets, it will take some time to absorb all the existing inventory.

.

stacked behind the door are the photographs of yours. in the basket

down the hall there’s a soccer shirt that i borrowed.

the end isn’t the

end. the end isn’t the end of this.

picking out the darkened hair from

each and every happy moment. i’ve come to terms that have been laid

bare, quiet sleeping angels in my bed.

the end isn’t the

end. the end isn’t the end of this.

so don’t you disappoint yourself

again, you’ll be back home.. you disappoint yourself

again, you’ll be back home.. you disappoint yourself

again, you’ll be back home.. before too long..

these discussions with

myself, the kinds of things that don’t tend to help. pacing back and

forth with my guitar, looking way up high on a shelf.

This week in the comments, we joked about new lending programs for the next real estate bubble. MalibuRenter, the gentlemen who helped with the content editing of my upcoming book, makes a living patenting financial products (among other things). The following is an idea for a new patent (tongue in cheek).

Lending during the Great Housing Bubble was too messy. There were too many loan programs. Since real estate always goes up, and since people want immediate access to this appreciation to spend it like income, a new loan product which readily provides this money is in order. The Option ARM was a major innovation. By allowing for negative amortization, people were able to add to their loan balance and effectively “cash out” their equity. The problem with this loan program is that it didn’t go far enough — people still had to make payments, and they had to get HELOCs to extract the remainder.

The new loan program I am proposing is called the “Pay You” loan, or PU for short. The PU loan has no payment of any kind. The total amount of interest each month is added to the loan balance. Further, appreciation in excess of this monthly interest is sent to the borrower each month. Rather than pay for an updated appraisal each month to determine value, an automated reappraisal system which looks at the current pricing of comps can accurately determine the current market value. Since homes now pay cash to owners each month, home ownership would be very desirable, and home prices should rise steadily far in excess of the monthly interest cost. With automated appraisals, little additional servicing costs would be required. Also, lenders would find the monthly service fees an attractive feature, so they would readily peddle the PU loan to any borrower who wanted it, and since borrowers are actually being paid to own their home, everyone would want to enroll in the program.

These loan programs would be very attractive to investors because the interest income would be booked as profits, and since the balance is growing each month, the interest income gets compounded. The main problems investors in mortgage loans have is that borrowers often pay back these loans early, and the balanced decline over time. Therefore, they do not receive the rate of return reflective of the stated interest rate. With the PU loan, investors actually get a greater return due to the compounding effect. The early payback is not a problem because even if a borrower sells a home, they will quickly buy a new one to get back on the home appreciation gravy train. The PU loans may even allow for assumability and portability so the loan doesn’t need to be closed out when a buyer wants to move up or sells. It is a panacea.

Now we just need home prices to always go up…

.

I call you,when I need you my hearts on fire You come to me, come to me, wild and wild

You come to me, give me everything I need Give me a lifetime of promises and a world of dreams Speak the language of love like you know what it means And it cant be wrong, take my heart and make it strong, baby

Chorus: Youre simply the best, better than all the rest, better than anyone, anyone Ive ever met! Im stuck on your heart, I hang on every word you say Tear us apart, baby I would rather be dead

In your heart I see the start of every night and every day In your eyes, I get lost, I gte washed away Just as long as Im here in your arms I could be in no better place…

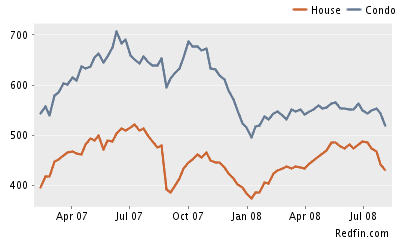

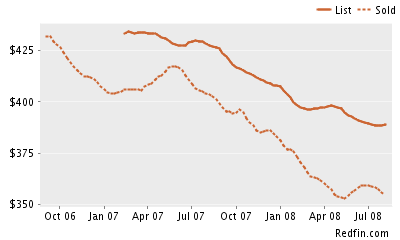

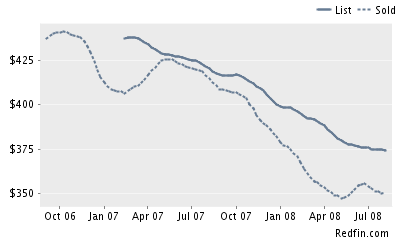

Detailed stats on the Irvine housing market are something we are always

interested in. The Inventory number in the sidebar comes from

ZipRealty. A chart of those numbers shows some interesting trends. We also have some great resources provided by ipoplaya and IrvineRealtor.

A new resource we just learned about are the Neighborhood Analytics that Redfin launched. Irvine charts available after the jump…

Irvine: Number of Homes for Sale

Irvine Homes: $/Sq. Ft.

{adsense}

Irvine Condos: $/Sq. Ft.

All of these charts can be found on the Irvine page at Redfin. Another cool thing about these charts is that they are also available by neighborhood (ie Northwood, Oak Creek, etc) and by zip. Take a look and let us know if you see anything interesting.

Sometimes you see a property where the asking price simply cannot be explained as anything other than greed. This weekend’s featured property falls in this category. It has been on the market for 580 days! Do you think they might have been able to lower the price and move it by now? These owners have been very conservative with their mortgage, they have paid it down, and there are no HELOCs. Their asking price gyrations have nothing to do with mortgage conditions or anything other than their desire to double their money in 5-6 years. Their inability to grasp the reality of the market has left them changing their asking price frequently and woefully missing the market. I hope they and their realtor are having a good time because they certainly haven’t done much to sell their house.

Listing Price History

Date

Price

Feb 03, 2007

$939,900

Feb 12, 2007

$924,900

Mar 06, 2007

$919,900

May 02, 2007

$914,900

May 04, 2007

$912,000

Jul 21, 2007

$899,900

Jul 25, 2007

$912,000

Aug 18, 2007

$899,000

Jan 27, 2008

$849,900

Mar 03, 2008

$824,900

Mar 08, 2008

$799,900

Apr 30, 2008

$849,900

Jun 30, 2008

$824,900

Source: SoCalMLS

Their listing price activity reminds me of the Curly Shuffle — two steps forward and one step back.

Beautiful Fieldstone Barrington home located on a cul-de-sac. Nice size

yard w/patio cover/dramatic slate hardscape in back & front

yard/ceiling fans/built-in cabinets in garage/french doors/beautiful

tile floors/full splash in kitchen. Do not miss seeing this home!

Yesterday’s post stirred up quite a controversy, and today’s probably will as well. It is politically incorrect and full of stereotypes that will make many cringe. There is a reason we have those politically incorrect stereotypes — they describe large groups of real people who exhibit stereotypical traits and behaviors. The Political Correctness crowd may not like it, and they may pressure people from expressing these stereotypes (at least to the degree that people fear the vengeful wrath of the PC police.) However, if people fit a profile, then there must be some validity to it.

One of the unique characteristics of the Great Housing Bubble was the large increase in market participation among women — sometimes single women and sometimes as married women buying property on their own. Some amount of this is to be expected as single women establish careers and put off marriage. In the past, most single women rented as did most men in their 20s. Men would often buy a house even if they were single. I suspect many viewed this as proof of their ability to be a provider and to attract a mate (I know I did.) Women more often would not buy a home when they were single. I suspect many did not because they knew they would have to deal with two houses when they got married, and the property would be a hindrance. Also, when you look at consumer demographics and personal savings, single women have not historically been big savers. Sure there are always some who are responsible from a young age, but many single women prefer to run up big credit card bills obtaining the latest fashion trends than worry about saving money (and yes, single men spend a lot on beer too.) The trend toward married women buying property as “her sole and separate property” was also a new phenomenon.

So what changed during the Great Housing Bubble? First, since saving was eliminated as a condition of ownership, many single women decided to buy and have a home of their own. Rather than a property being a hindrance, it became a great speculative asset that provided huge amounts of extra spending money. Several of the properties I have profiled with excessive HELOC abuse have been solely owned by women (not that men were any more responsible.) With the large number of women working as mortgage brokers and

realtors, it is likely that many of the purchases by married women as their sole and separate property were by those in

the business. It was all part of making a living.

Why did I pick the song Stupid Girl? Well, these purchases did not turn out to well for many. Was it stupid? I guess if you got to “live large” in your 20s from the HELOC on your house, perhaps not. The memories are great, and you still have time to recover financially. For the older singles and married women who speculated in the real estate market, there will be more serious ramifications. I don’t think anyone is going to label these purchases as a work of genius. Today’s featured property was purchased by a married woman as her sole and separate property, and now, after the foreclosure she has bad credit. Do you think this has impacted the family? It can’t be a plus.

French doors in living room & kitchen. Oak crown molding. Tile in

family room and kitchen. Great community & schools. Low

association.

The lender has been lowering price to move this one.

Listing Price History

Date

Price

Mar 19, 2008

$649,900

May 05, 2008

$609,900

Jun 02, 2008

$594,900

Jul 24, 2008

$559,000

This property was purchased on 11/15/2006 for $689,000. The buyer, a $551,200 first mortgage, a $137,800 second mortgage and a $0 downpayment. It went back to the bank for $560,000 on 11/14/2007, almost a year to the day. I usually smell fraud when I see them go back this quick. People will make the first two payments to get around being prosecuted for fraud, then stop payment and let it go back to the lender. The one-year timeline is just about right given the amount of time a foreclosure takes. If this had been purchased as a speculative flip (we should give the benefit of the doubt,) then this woman is really stupid. Or perhaps we should view her as a hapless victim of the unpredictable housing market? That might be an easier sell if there weren’t many people already predicting a crash by then.

If this property sells for its asking price, the total loss to the lender will be $163,540 after a 6% commission. Personally, I think this property is ugly inside and out, but then again I will not be buying for a couple more years, so my opinion doesn’t matter much right now. Perhaps someone will step up and pay that much, or perhaps they will keep renting and save their money. That wouldn’t be stupid…

.

Stupid girl, stupid girls, stupid girls Maybe if I act like that, that guy will call me back Porno Paparazzi girl, I don’t wanna be a stupid girl

Go to Fred Segal, you’ll find them there Laughing loud so all the little people stare Looking for a daddy to pay for the champagne (Drop a name) What happened to the dreams of a girl president She’s dancing in the video next to 50 Cent They travel in packs of two or three With their itsy bitsy doggies and their teeny-weeny tees Where, oh where, have the smart people gone? Oh where, oh where could they be?

Maybe if I act like that, that guy will call me back Porno Paparazzi girl, I don’t wanna be a stupid girl Baby if I act like that, flipping my blond hair back Push up my bra like that, I don’t wanna be a stupid girl

(Break it down now) Disease’s growing, it’s epidemic I’m scared that there ain’t a cure The world believes it and I’m going crazy I cannot take any more I’m so glad that I’ll never fit in That will never be me Outcasts and girls with ambition That’s what I wanna see Disasters all around World despaired Their only concern Will they **** up my hair

Maybe if I act like that, that guy will call me back Porno Paparazzi girl, I don’t wanna be a stupid girl Baby if I act like that, flipping my blond hair back Push up my bra like that, I don’t wanna be a stupid girl

Stupid girl, stupid girls, stupid girls

Stupid girl, stupid girls, stupid girls