Mortgage brokers and realtors are united: the end of the Federal tax credit was the end of the world.

Irvine Home Address … 14541 GUAMA Ave Irvine, CA 92606

Resale Home Price …… $749,000

{book1}

Bones, sinking like stones,

All that we fought for,

And homes, places we've grown,

All of us are done for.

Coldplay — Don't Panic

One of the hallmarks of an economic recession is the ongoing stress and periodic panic of the citizenry, particularly when there is no light at the end of the tunnel. The mainstream media becomes littered with feel-good stories about this statistic or that trend that is supposed to signal the end of the recession and the return to properity. Of course, each one turns out to be false, but the accuracy of the story was never the point; the story was written to provide emotional comfort.

It's rare to find a real sense of panic in news stories, and it is even more rare when the permanently bullish realtors lose their veneer of positivity and show their frightened inner selves. Today, I have a story of panic from the Mortgage News Daily and a freak out from a local realtor. Enjoy.

Purchase Demand In Freefall. Housing Industry Unraveling

The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending May 28, 2010.

"With another week of historically low mortgage rates, the trend from the prior three weeks continued, as refinance applications increased while purchase applications dropped. Purchase applications are now almost 40 percent below their level four weeks ago, while the refinance share, at 74 percent, is at its highest level since December," said Michael Fratantoni, MBA's Vice President of Research and Economics. "In addition, the ARM share dropped last week to its lowest level since March of this year, as borrowers took the opportunity to lock in at historically low fixed mortgage rates."

The Mortgage Bankers Association application survey covers over 50% of all US residential mortgage loan applications taken by mortgage bankers, commercial banks, and thrifts. The data gives economists a look into consumer demand for mortgage loans. In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment which can increase disposable income and consumer spending (or give consumers a chance to pay down other debts like credit cards). A falling trend of purchase applications indicates a decline in home buying interest, a negative for the housing industry and the economy as a whole.

Everyone knew purchases would drop off when the Federal tax credit expired, but few expected the drop to be as severe as it has been. I had the following data forwarded to me. It was written by Mark Raymond Godleski, a realtor with Altera Real Estate:

There has been a huge drop in Demand for Orange County residential Real Estate — 12% in just two weeks, and 17% in four weeks, to only 3303 new escrows within the past 30 days! Looks like the expiration of the first time Home Buyer tax credit has had a bigger effect than we thought. We are now 10% Below 2009 Demand for May! Where we go from here is anybody's guess.

Inventory has slowly increased, unabated since the beginning of the year to 9839 residences for sale in OC — an increase of 2674 homes, 37%! And an increase of 3% in just the last 2 weeks! CAUTION TO SELLERS: current Buyers just are not ready to pay more than the most recent comparable sale. They are very price conscious.

Market Time has increased from 2.53 months to 2.98 months, a 18% increase in just 2 weeks! When Demand drops and Inventory rises, this is what happens. It is Great News for Buyers as this will reduce the fierce competition for Homes. This is still a Sellers' Market, just less so.

When the positive spinmeisters start freaking out, you know something bad is brewing.

Back to Purchase Demand In Freefall. Housing Industry Unraveling

Excerpts Taken From The Release…

The Market Composite Index, a measure of mortgage loan application volume, increased 0.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 0.3 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is up 3.5 percent.

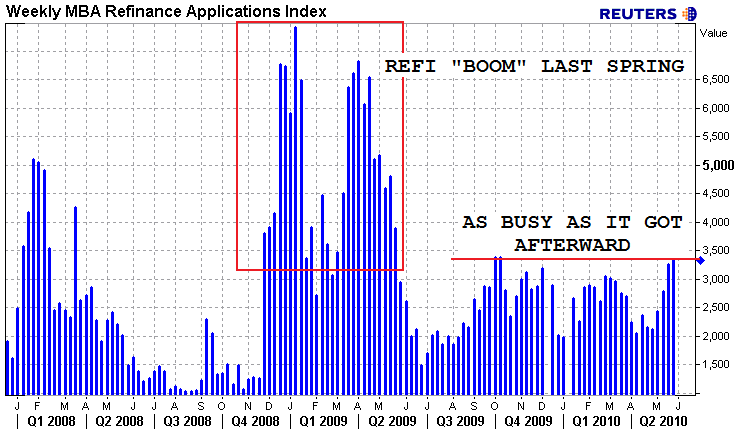

The Refinance Index increased 2.4 percent from the previous week. This was a smaller increase than in previous weeks, but was still the fourth consecutive weekly increase for the Refinance Index and it remains at its highest level since October 2009. The four week moving average is up 11.5 percent for the Refinance Index. The refinance share of mortgage activity increased to 73.8 percent of total applications from 72.2 percent the previous week.

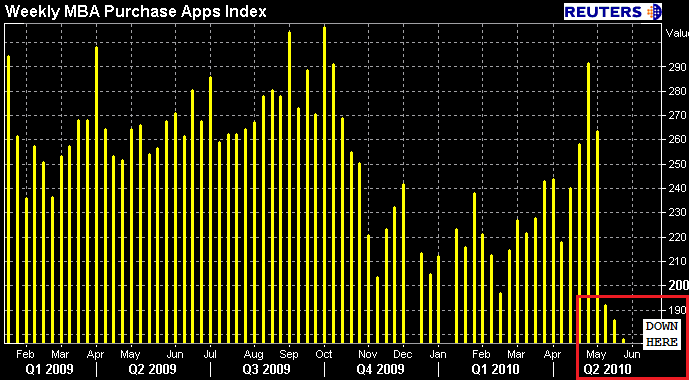

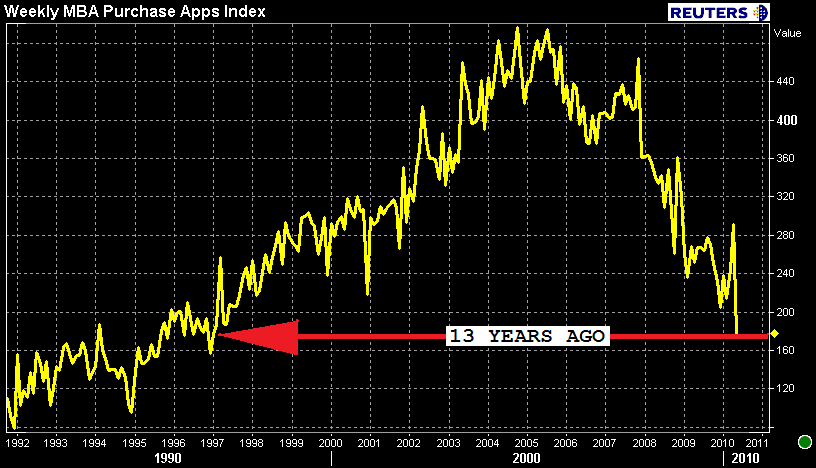

The seasonally adjusted Purchase Index decreased 4.1 percent from one week earlier. The Purchase Index decreased for the fourth consecutive week and is currently at the lowest level since April 1997. The unadjusted Purchase Index decreased 5.2 percent compared with the previous week and was 16.8 percent lower than the same week one year ago. The four week moving average is down 12.1 percent for the seasonally adjusted Purchase Index.

That chart doesn't really put things in the proper perspective, but this one does…

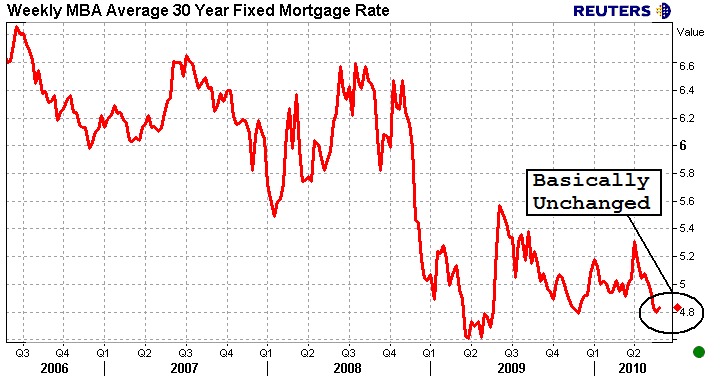

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.83 percent from 4.80 percent, with points decreasing to 1.05 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The effective rate also increased slightly from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 4.24 percent from 4.25 percent, with points increasing to 1.11 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week due to the increase in points.

The average contract interest rate for one-year ARMs increased to 6.96 percent from 6.83 percent, with points decreasing to 0.27 (including the origination fee) for 80 percent LTV loans. The adjustable-rate mortgage (ARM) share of activity decreased to 5.2 percent from 6.0 percent of total applications from the previous week.

Ugh. This morning I talked about how all the optimistic data we've been hearing on housing is just "fine and dandy"…but was nothing unexpected. Homebuyer demand spiked at the end of the original tax credit in early November and it did the same thing at the expiration of the extended version of the homebuyer tax credit this April. No surprises!

The true barometer of the health of housing rests in May housing data..not April. If the recent downtrend in purchase apps holds any clue as to what sort of results we'll see in May, it won't be pretty. Anecdotal evidence is highly supportive of this theory. Heck, besides the drastic decline in purchase demand we've seen, pull-through on refi apps is poor thanks to the vast variety of hoops that must be jumped through before a loan can be cleared to close.

Working in this industry is no fun right now. Borrowers don't trust loan officers. Originators are losing deals for a measly $250 processing fee. Underwriters and appraisers are annoying each other to protect their own behinds. Meanwhile, secondary is fronting the bill and processors (a generally "testy" group to begin with) are stuck in the middle of it all. To make matters worse…Realtors are pointing the finger at mortgage professionals for the slowdown. I feel like my world is unraveling in front of me. Can't we all just get along?

When interest rates are at historic lows, it would be logical to assume mortgage activity would be at an all-time high, particularly refinances. The fact that this activity is near historic lows is very revealing. Basically, everyone who could refinance already has, and the buyer pool is seriously depleted because so many are unemployed, underwater, or recently foreclosed.

This isn't just a disaster for mortgage and real estate professionals, this is part of the ongoing disaster for banks. Who are they going to sell all their distressed property to? The reason we have such a backlog of delinquencies and foreclosures is because lenders know they don't have any buyers to sell to. Lenders are not allowing long-term squatting because they want to; they allow squatting because they have to.

Another typical Irvine home owner HELOC abusing squatter

- The previous owners of today's featured property paid $475,000 on 5/29/2003. The owners used a $322,700 first mortgage, a $100,000 second mortgage and a $52,300 down payment.

- On 3/31/2004 they refinanced with a $450,000 first mortgage.

- On 2/3/2005 they refinanced with a $623,000 first mortgage.

- On 3/16/2006 they obtained a HELOC for $100,000.

- Total property debt is $723,000.

- Total mortgage equity withdrawal is $300,300

-

The squatted off an on for about 2 years.

Foreclosure Record

Recording Date: 03/03/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 11/30/2009

Document Type: Notice of Default

Foreclosure Record

Recording Date: 02/19/2009

Document Type: Notice of Rescission

Foreclosure Record

Recording Date: 11/14/2008

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 08/06/2008

Document Type: Notice of Default

Lemons into lemonade

Someone is making a profit from this property. It was picked up at trustee sale in March. The new owners is looking to flip it for a quick $93K. They will probably get $70K out of the deal.

Irvine Home Address … 14541 GUAMA Ave Irvine, CA 92606 ![]()

Resale Home Price … $749,000

Home Purchase Price … $610,500

Home Purchase Date …. 3/23/2010

Net Gain (Loss) ………. $93,560

Percent Change ………. 22.7%

Annual Appreciation … 84.6%

Cost of Ownership

————————————————-

$749,000 ………. Asking Price

$149,800 ………. 20% Down Conventional

4.87% …………… Mortgage Interest Rate

$599,200 ………. 30-Year Mortgage

$152,801 ………. Income Requirement

$3,169 ………. Monthly Mortgage Payment

$649 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$62 ………. Homeowners Insurance

$43 ………. Homeowners Association Fees

============================================

$3,924 ………. Monthly Cash Outlays

$3,924 ………. Monthly Cash Outlays

-$770 ………. Tax Savings (% of Interest and Property Tax)

-$737 ………. Equity Hidden in Payment

$280 ………. Lost Income to Down Payment (net of taxes)

$94 ………. Maintenance and Replacement Reserves

============================================

$2,790 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$7,490 ………. Furnishing and Move In @1%

$7,490 ………. Closing Costs @1%

$5,992 ………… Interest Points @1% of Loan

$149,800 ………. Down Payment

============================================

$170,772 ………. Total Cash Costs

$42,700 ………… Emergency Cash Reserves

============================================

$213,472 ………. Total Savings Needed

Property Details for 14541 GUAMA Ave Irvine, CA 92606

——————————————————————————

Beds: 4

Baths: 1 full 2 part baths

Home size: 2,327 sq ft

($322 / sq ft)

Lot Size: 5,000 sq ft

Year Built: 1971

Days on Market: 21

Listing Updated: 40305

MLS Number: S616253

Property Type: Single Family, Residential

Community: Walnut

Tract: Cp

——————————————————————————

Gorgeous remodeled home in College Park. Four bedrooms & one spacious bonus room. Recessed lights throughout. Crown moldings & ceiling fans. Granite countertop & stainless steel appliance. Pre-wired surround sound speakers in family room. Newly-built fireplace with BBQ in the backyard. Within walking distance of school & park.

I hope you have enjoyed this week, and thank you for reading the Irvine Housing Blog: astutely observing the Irvine home market and combating California Kool-Aid since 2006.

Have a great weekend,

Irvine Renter

Any borrower so far underwater as to fail to qualify for a government program should default. What are they waiting for? The government basically told them to.

Any borrower so far underwater as to fail to qualify for a government program should default. What are they waiting for? The government basically told them to.