In an effort to stop the double dip from getting worse, lenders are slowing foreclosure activity nationwide. Their efforts will delay the market bottom and extend squatting benefits.

Irvine Home Address … 219 TALL OAK Irvine, CA 92603

Resale Home Price …… $550,525

Now if you're feelin' kinda low 'bout the dues you've been paying

Future's coming much too slow

And you wanna run but somehow you just keep on stayin'

Can't decide on which way to go

I understand about indecision

But I don't care if I get behind

People livin' in competition

All I want is to have my peace of mind.

Boston — Peace of Mind

Do you ever find yourself getting impatient with the way lenders have dragged out the housing crash? I do. It isn't merely that I want to see lower house prices as those are prevalent across most of the country. I want to see the economic wounds heal. That isn't going to happen until lenders foreclose on all the delinquent mortgage squatters and resell the resulting REO.

Do you ever find yourself getting impatient with the way lenders have dragged out the housing crash? I do. It isn't merely that I want to see lower house prices as those are prevalent across most of the country. I want to see the economic wounds heal. That isn't going to happen until lenders foreclose on all the delinquent mortgage squatters and resell the resulting REO.

While we wait for lenders to do what needs to be done, the homebuilding industry remains in the doldrums, lending remains at anemic levels, and overall economic activity is feeble. None of that will change until our zombie banks are put out of their misery and recapitalized. In the meantime, lenders are slowing foreclosures and dragging out the economic morass. Academics in the United States used to criticize Japan for the way they dealt with this same problem in the 1990s. We are going down the same path.

U.S. Foreclosure Activity Falls to 44-Month Lows in July; Artificially Slowed by Banks

Posted by Michael Gerrity 08/11/11 8:00 AM EST

According to RealtyTrac's U.S. Foreclosure Market Report for July 2011, foreclosure filings — default notices, scheduled auctions and bank repossessions — were reported on 212,764 U.S. properties in July, a 4 percent decrease from June and a 35 percent decrease from July 2010. The report also shows one in every 611 U.S. housing units with a foreclosure filing during the month of July.

Foreclosures are essential to the economic recovery. There is little debate that the housing market will not clear and house prices will not enjoy sustained appreciation until the foreclosure backlog is cleared out. As long as shadow inventory or REO inventory is present, lenders will sell into any rally thus stopping it cold.

The fact that lenders are slowing the rate of foreclosure simply means the bottom is being pushed back further in time. Also, since the delinquency rate is still very high, a slowdown in foreclosure rates means more and more people are squatting for longer periods of time.

“July foreclosure activity dropped 35 percent from a year ago, marking the 10th straight month of year-over-year decreases in foreclosure activity and the lowest monthly total since November 2007,” said James J. Saccacio, chief executive officer of RealtyTrac.

“This string of decreases was initially triggered by the robo-signing controversy back in October 2010, which forced lenders to substantially slow the pace of foreclosing, but the downward trend in foreclosure activity has now taken on a life of its own.

This should be no surprise to IHB readers. I have long contended that robo-signer was merely a ruse, the excuse-of-the-day, to delay foreclosures and avoid writing down more bad loans. Lenders will continue this behavior as long as they believe there is no buyer demand to sell into. Eventually, lenders will realize the buyer demand they are waiting for will never materialize. When they do, they will capitulate and sell for whatever they can get.

This should be no surprise to IHB readers. I have long contended that robo-signer was merely a ruse, the excuse-of-the-day, to delay foreclosures and avoid writing down more bad loans. Lenders will continue this behavior as long as they believe there is no buyer demand to sell into. Eventually, lenders will realize the buyer demand they are waiting for will never materialize. When they do, they will capitulate and sell for whatever they can get.

It appears that the foreclosure processing delays, combined with the smorgasbord of national and state-level foreclosure prevention efforts — including loan modifications, lender-borrower mediations and mortgage payment assistance for the unemployed —may be allowing more distressed homeowners to stave off foreclosure.

No, it is allowing more delinquent mortgage squatters to stay in homes that should be resold to those who are willing and able to pay for them.

“Unfortunately, the falloff in foreclosures is not based on a robust recovery in the housing market but on short-term interventions and delays that will extend the current housing market woes into 2012 and beyond,” Saccacio continued.

Yes, the slowdown in foreclosure activity will delay the bottom and allow more squatting.

“A stabilizing economy and improving job market are the long-term keys to a housing market recovery.”

Persistent unemployment is an ongoing drain to the economy and to the housing market.

Foreclosure Activity by Type

Default notices (NOD, LIS) were filed for the first time on a total of 59,516 U.S. properties in July, a 7 percent decrease from the previous month and a 39 percent decrease from July 2010. July's default notice total was 58 percent below the monthly peak of 142,064 default notices in April 2009.

Foreclosure auctions (NTS, NFS) were scheduled for 85,419 U.S. properties in July, a decrease of 5 percent from June and a decrease of 37 percent from July 2010. July's foreclosure auction total hit a 36-month low and was 46 percent below the monthly peak of 158,105 scheduled auctions in March 2010.

Lenders repossessed a total of 67,829 properties (REO) in July, a 1 percent decrease from the previous month and a 27 percent decrease from July 2010. The July REO total was 34 percent below the monthly peak of 102,134 bank repossessions in September 2010.

As i noted in a previous post, the dramatic declines are almost exclusively in judicial foreclosure states.

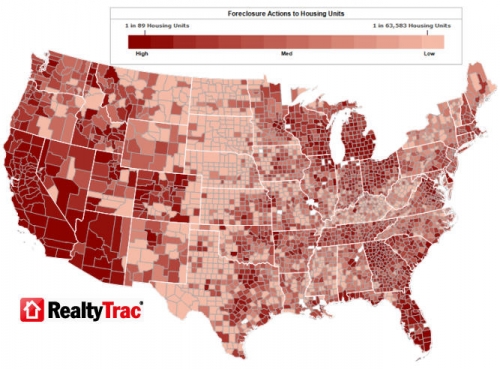

Nevada, California, Arizona post top state foreclosure rates

Nevada posted the nation's highest state foreclosure rate for the 55th straight month in July, with one in every 115 housing units receiving a foreclosure filing during the month. A total of 9,930 Nevada properties had a foreclosure filing in July, a 1 percent decrease from the previous month and a 28 percent decrease from July 2010.

Nevada also boasts one of the largest action postponement and cancelation percentages of any state. Locally, about 87% of auctions are delayed or canceled, but in Nevada the number is closer to 95%. It's a classic example of kicking the can down the road.

Despite a 16 percent year-over-year decrease in foreclosure activity, California registered the nation's second highest state foreclosure rate in July, with one in every 239 housing units with a foreclosure filing during the month.

With one in every 273 housing units with a foreclosure filing, Arizona posted the nation's third highest state foreclosure rate, after holding the No. 2 spot for seven straight months ending in June. A 39 percent month-over-month drop in REO activity pulled Arizona's total foreclosure activity in July down 25 percent from the previous month and down 38 percent from July 2010.

Other states with foreclosure rates ranking among the top 10 were Georgia, Utah, Florida, Michigan, Idaho, Illinois and Wisconsin.

10 states account for more than 70 percent of U.S. total

10 states accounted for 73 percent of U.S. foreclosure activity in July, led by California, where 56,193 properties had a foreclosure filing during the month — up 4 percent from the previous month but still down 16 percent from July 2010. Initial default notices in California were down 6 percent from the previous month, but REOs increased on a month-over-month basis for the second straight month and scheduled auctions were up 11 percent from the previous month. …

Foreclosure activity spikes in some hard-hit cities

Las Vegas continued to post the nation's highest foreclosure rate among metropolitan areas with a population of 200,000 or more, with one in every 99 housing units with a foreclosure filing in July.

But spiking foreclosure activity in some of the other cities with foreclosure rates in the top 20 narrowed the gap between those cities and Las Vegas. Seven of the cities in the top 10 and 14 of the cities in the top 20 posted monthly increases in foreclosure activity.

.jpg)

Foreclosure activity in the Stockton, California metro area increased 57 percent from June to July, giving it the nation's second highest metro foreclosure rate — one in every 124 housing units with a foreclosure filing during the month. Stockton foreclosure activity in July was still down 7 percent from July 2010.

With one in every 140 housing units with a foreclosure filing, the Vallejo-Fairfield, Calif., metro area posted the nation's fourth highest metro foreclosure rate in July thanks in part to a 33 percent month-over-month increase in foreclosure activity.

Foreclosure activity increased 83 percent on a month-over-month basis in the Naples-Marco Island, Fla., metro area, which posted the nation's 15th highest metro foreclosure rage, and foreclosure activity was up 60 percent on a month-over-month basis in the Ocala, Fla., metro area, which posted the nation's 17th highest metro foreclosure rate.

I find it interesting that lenders are continuing to push through foreclosures at a high rate in the hardest hit areas. To me this is a clear sign of capitulation. In Las Vegas, they have given up on trying to support prices. They are selling for whatever they can get for their properties — which isn't very much.

In over their heads from the start

There were a whole group of borrowers during the housing bubble who bought houses they had no business being in. Many imported down payments from a previous bubble property sale, and many used 100% financing. Most of these borrowers could never afford the property with the sane underwriting standards we require today.

- The previous owners of today's featured REO paid $627,000 on 9/15/2004. They used a $500,000 first mortgage and a $127,000 down payment.

- A scant four months later, they refinanced with a $510,000 Option ARM and obtained a $197,000 HELOC.

- If they maxed out the HELOC, they regained their down payment plus obtained $80,000 in HELOC booty.

-

The stopped paying in August of 2008 at the latest and managed to squat for over two and one half years.

Foreclosure Record

Recording Date: 05/06/2010

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 03/12/2009

Document Type: Notice of Sale

Foreclosure Record

Recording Date: 12/09/2008

Document Type: Notice of Default

The bank owns this property now, the former owners lost their down payment (or HELOCed and spent it) and now their credit is trashed.

——————————————————————————————————————————————-

This property is available for sale via the MLS.

Please contact Shevy Akason, #01836707

949.769.1599

sales@idealhomebrokers.com

Irvine House Address … 219 TALL OAK Irvine, CA 92603

Resale House Price …… $550,525

Beds: 3

Baths: 3

Sq. Ft.: 1600

$344/SF

Property Type: Residential, Condominium

Style: 3+ Levels, Contemporary

View: City Lights, Hills, Mountain, Peek-A-Boo, Yes

Year Built: 2004

Community: Quail Hill

County: Orange

MLS#: S664118

Source: SoCalMLS

On Redfin: 56 days

——————————————————————————

HUGE REDUCTION! Excellent corner location across from the park and pool. Vantage point views – panoramic of city lights and mountains. Modern style Tri Level with 3 bedrooms (one lower level and two on third level) with 3.5 baths. Each bedroom has access to full bath, while guests have access to 1/2 bath on main floor (2nd). Balcony with BBQ gas line, large wrap around side yard for entertaining. Walking distance to Alderwood Basics Plus school and Association Amenities – Pools, gym, parks, etc.

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis ![]()

Resale Home Price …… $550,525

House Purchase Price … $627,000

House Purchase Date …. 9/15/2004

Net Gain (Loss) ………. ($109,507)

Percent Change ………. -17.5%

Annual Appreciation … -1.9%

Cost of Home Ownership

————————————————-

$550,525 ………. Asking Price

$110,105 ………. 20% Down Conventional

4.19% …………… Mortgage Interest Rate

$440,420 ………. 30-Year Mortgage

$120,515 ………. Income Requirement

$2,151 ………. Monthly Mortgage Payment

$477 ………. Property Tax (@1.04%)

$183 ………. Special Taxes and Levies (Mello Roos)

$115 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$187 ………. Homeowners Association Fees

============================================

$3,113 ………. Monthly Cash Outlays

-$353 ………. Tax Savings (% of Interest and Property Tax)

-$613 ………. Equity Hidden in Payment (Amortization)

$165 ………. Lost Income to Down Payment (net of taxes)

$89 ………. Maintenance and Replacement Reserves

============================================

$2,401 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$5,505 ………. Furnishing and Move In @1%

$5,505 ………. Closing Costs @1%

$4,404 ………… Interest Points @1% of Loan

$110,105 ………. Down Payment

============================================

$125,520 ………. Total Cash Costs

$36,800 ………… Emergency Cash Reserves

============================================

$162,320 ………. Total Savings Needed

——————————————————————————————————————————————————-

The longer this foreclosure process draws out, the longer architects like myself have to fight over the few scraps that are new design projects. And the fee-cutting is breathtaking! Might as well get a blue collar job doing something in any other industry, because you’ll make more money doing that!

Architecture has been particularly hard hit. I worked with engineers doing land planning, so we were the beginning of the development cycle. Engineers have been idle for 4 years now. It isn’t until engineers go back to work that the pipeline gets refilled to provide any work to architects.

I had lunch with an architect recently who told me he bid $49,000 on a project only to find someone bid $18,0000. He said there was no way to produce a decent set of documents for $18,000 even for one guy working out of his garage. Many firms are buying jobs just to help cover some overhead. It is really a tough time out there.

As I watch the entire real estate development industry sit idle, it pains me to watch my friends and acquaintances struggle to get by.

I know real estate agents that are barely surviving. No business, no commissions.

Seller’s not wanting to sell at market prices and a buyer’s strike. Buyers not buying the RE & government’s lies. Add to this banks propped up by the government bailout not foreclosing on homes not being paid for. It’s a mess wrought by only the best of intentions (perhaps).

Best thing for everyone would be for the market to find the natural bottom. I’ve been waiting and renting for years, waiting for what I thought would be the inevitable correction. Alas, I wait some more.

Kelja,

The best thing isn’t going to happen soon. The grasshoppers are with the queen ant to enslave the working ants. Since we are a nation of law, the laws have been made to benefit the grasshopper or locust. They have the congress, courts, police and military to back it up. Just try to do a Jim G and not pay your taxes and see what happens. I guarantee that you will not become the Sec. of T.

Kelja,

One huge difference between real estate agents and architects surviving the recession is the fee cutting. Architects are desperate and cut fees drastically (i.e. bad businesspeople in general) on the few jobs that do exist, whereas the Realtard cartel still manages to hold up the standard 3% commission on the sales that do go through. It’s amazing how RE agents can hold that… unless you realize that most novice and johnny-come-lately real estate agents didn’t have much qualification or credentials to begin with and have migrated to other, more appropriately compensating industries to their skill levels. The real estate agents out there making the sales are likely the more savvy, ruthless ones…

Wow… I believe it, Larry! Your friend’s story is common nationwide today, but my instinct tells me it’s even more common in California because there are more existing, established A/E/C firms just looking to survive. At a (albeit low for OC) standard billable rate of $100/hr for an architect, bidding $18,000 on a job means the only way for it to be profitable is to be able to produce all the work in approximately 180-200 man hours. Even the smallest home build projects or renovations take 400-500 man hours for an architects if they’re being done properly and a full scope of an architect’s services. Sounds like the $18,000 bid architect is essentially giving his services away at about a $10/hour salary after you factor in the overhead costs on that job!

One other aspect of the bubble phenomenon we’re going to see is a generation gap of architects/building engineers. Anyone who graduated college between about 2003-present is going to have a hard time establishing themselves in the building industry with credible experience and many will eventually give up and go do other work that can pay the bills adequately. So in about 15-20 years, we’re going to see a knowledge gap when those who currently are the more experienced A/E are retiring/dying off, and there’s about a 10-15 year lull in senior staff in firms. That means lesser experienced A/E doing the work during the next building boom. And the cycle continues…

Two great points above.

We’re seeing the same thing in civil engineering construction. Contractors are taking jobs at way under cost, just to keep their company from dismantling altogether. They’re bleeding money, but figure they’ll have fresher resumes and retain critical staff for “when it gets better”.

The only upside is many public agencies are getting infrastructure built for very cheap.

“The only upside is many public agencies are getting infrastructure built for very cheap.”

Could be even cheaper for the tax payer if there weren’t Davis Bacon prevailing wage requirements.

architectdave: Good point, this is also true in Manufacturing.. Like we always say “You can’t teach experience”

You can complain but I bet you don’t have it as bad as this guy…

http://www.fastcodesign.com/1662870/chinese-architect-builds-egg-house-on-sidewalk-to-escape-insane-rents

I agree with the one comment on that story 🙂

Actually, this won’t be a problem. It just won’t be American archetects and engineers on the job in the United States. Brazil is doing great things in archetecture, and we all know about india’s tech schools. Many teach infrastructure professions as well. They’ll just H1-B visa in and nobody will have to train an inexperienced American, all with the lie we don’t have anough skilled applicants coming from the American population. Many Americans will still get the degrees, just not the experience.

GSE’s, the feds, and the Fed are all complicit in this housing fiasco, and now they are doing everything in their central planning arsenal to alleviate pain that they enabled. The problem with central planning is that it’s always a blunt tool focused on a handful of objectives, ignoring myriad unintended consequences.

In this case, we’re seeing banks supported by Fed giveaways taking their time (because they are subsidized) liquidating homes, pricing above what market would otherwise absorb.

Then there are other plans like the push for GSE’s to rent out foreclosed inventory, rather than put REO’s up for sale. Consequence: If this goes forward, it could destroy rental markets by driving rents down (more supply of rentals + rents being set by subsidized institutions), and hence investment values.

There’s never a free ride in economics, so the sooner markets return to stability via real equilibrium, the better!

…it could destroy rental markets…

Then there is Section 8 subsidies which distort

rental markets in the *opposite* direction, in

that they set a floor under rents.

The government simply needs to keep it paws out

of all aspects of the Real Estate markets.

That’s exactly right! The law of unintended consequences…

Give it a REST already! The entire purpose of your blog has been rendered NULL & VOID. You keep blindly focusing on “when will houses become more affordable” when the BIGGER PICTURE indicates that the United States of America is C-O-L-L-A-P-S-I-N-G. It is I-N-S-O-L-V-E-N-T. There are NO MORE JOBS. There is NO MORE RULE OF LAW. Crime is EXPLODING. Corruption is RAMPANT. Who in their f@cking right mind would want to TIE THEMSELVES to a SINKING SHIP, which is EXACTLY what buying a house represents in present circumstances?

It’s time for you to start a NEW BLOG: the ARGENTINA, BRAZIL (or similar) HOUSING BLOG. After all, THAT’S where most Americans will be buying their next homes.

Mike Mish Shedlock reports that the Foreclosure Pipeline in New York is 693 months (over 57 years) and 621 Months (over 51 years) in New Jersey. This reflects the power of the Banking Cartel and strategic defaulting loan holders living payment free in bank owned homes.