The political pressure to balance the federal budget may force politicians to curtail or even eliminate the home mortgage interest deduction. Momentum is growing toward this end.

Irvine Home Address … 402 FALCON Crk Irvine, CA 92618

Resale Home Price …… $250,000

I feel so good come payday

I think of all the things I'm gonna buy

when I pick up my pay

Don't you know

but then they hand me that little brown envelope

I peep inside Lord I lose all hope

Cause from those total wages earned

down to that net amount that's due

I feel the painful sense of loss between the two

Johnny Cash — After Taxes

The home mortgage interest deduction is a very important tax policy to most Irvine homeowners. The primary beneficiaries of the home mortgage interest deduction are high wage earners with large mortgages — Irvine residents. People with small mortgages don't pay enough interest to itemize. The wealthy don't have large mortgages. If there is any political issue Irvine residents will have an opinion about, it is the home mortgage interest deduction.

I wrote a detailed analysis of the home mortgage interest deduction in Tax Policy and Housing:

Debt subsidies, in particular the home mortgage interest deduction, are seen as a great benefit to home ownership. The benefit is widely overestimated and misunderstood.

First, people fail to understand that to obtain a debt subsidy, you must have debt. You must be making an interest payment on this debt in order to qualify, and you get to reduce your tax burden by a small percentage of the interest amount. In short, you are paying a dollar to save a quarter. There are people who actually seek to maximize their interest payments in order to increase this subsidy. This is really, really foolish. Anyone out there who believes it is a good idea to spend $1 to receive $0.25 in return, please send me as much money as you wish, and I promise to send back 25% of it.

Realtors try to con people with the “throwing your money away on rent” argument. Homeowners buy into the fallacy. Interest is the rent on money. You throw away money on interest just like you throw it away on rent. In fact, people who overpay for housing throw away more money on interest than renters do to obtain the same property, even after the tax subsidy. The only argument one can make for paying extra interest is if you are receiving a return on that investment through property appreciation. We all see how that is turning out.

The main reason the benefits of the home mortgage interest deduction are overestimated is because people forget they must give up the standard deduction in order to obtain it. This is one area where tax policy can have hidden and indirect impact on housing. Changes in the standard deduction greatly impact the benefit of the home mortgage interest deduction. As the standard deduction is increased, the positive impact of the HMID is decreased. In fact, if the standard deduction were doubled, the average American holding a $150,000 mortgage probably would not bother itemizing to obtain the HMID because it would be of no tax benefit at all. This would certainly simplify people's tax returns. A higher standard deduction is also a boon to renters who do not have the option of obtaining the HMID.

When we set up the RentVsOwnulator, we put in a 25% tax benefit from the HMID. Some people have commented that this is too small a number. It is not. Several people have run the calculations both with and without the HMID, and the net difference is only 25% even at the highest tax brackets. Basically, if you want to figure out your real tax benefit, take your highest marginal tax rate and subtract 10%. That will be a much closer estimate to reality. This reduction is caused by losing the standard deduction.

Another facet to the HMID is the cap level. Currently mortgages up to $1,000,000 are eligible for the deduction. Does anyone think this is right? Do you realize you as a taxpayer are subsidizing $1,000,000 mortgages? When the GSEs were set up, they established a conforming loan limit. The reason they did this is because they are mandated to subsidize mid and low income housing. Why is the limit on the HMID any higher than the conforming loan limit from the GSEs? Why are we subsidizing high income borrowers?

If we were to reduce the HMID cap level to $500,000 and adjust it by the CPI going forward, we are still subsidizing relatively high income borrowers ($500,000 is still almost triple the median home price in the US). A reduction in this cap would have the same impact as the lower GSE conforming limit is having: it would lower prices at the high end by eliminating the subsidies.

IMO, the government has no place in subsidizing house prices that are well above the median. One can argue that the government should not be subsidizing anything in housing, but the low and middle income subsidies are here to stay. If we raise the standard deduction and lower the HMID caps, we can greatly reduce the impact of the HMID and the cost we pay for it as taxpayers. This would have the effect of lowering prices on more expensive homes, but it would help stabilize the lower end of the market. That is what the market needs right now.

I also wrote about the home mortgage interest deduction when Shelia Bair noted the home mortgage interest deduction inflates home prices:

There is a much easier way to figure out how much eliminating the home-mortgage interest deduction would cause prices to drop. What is the marginal tax rate of the borrower? Assume that most buyers borrow the most they can afford on a monthly payment basis, and further assume intelligent ones have already factored in the tax savings. If you eliminate the tax savings, people will need to bring their payment down accordingly. This won't have much effect on the lower priced homes because many of those borrowers don't itemize, but in cities like Irvine, elimination of this deduction would cause loan balances to shrink by 25% to 40% to keep the same payment. Since about 80% of the house price is usually financed, this will lower prices 20% or more.

There is a related issue which isn't often discussed but very important to the housing market. If the home mortgage interest deduction were eliminated, many high wage earners who are underwater would strategically default. First, it would eliminate one of the financial benefits that prompts many to hang on. Second, since most high wager earners who are underwater would realize this will depress home prices in their price range, many more will abandon hope of a recovery and also strategically default.

When this issue was being discussed last year, it really worried the realtor community. In what can best be termed hysterical, California realtors claimed eliminating the mortgage interest deduction would devastate the nation.

The issue is back in the news again, and due to the large federal government budget deficits, some changes to the provisions of this deduction may actually come to pass.

A Taxing Debate: The Mortgage-Interest Deduction

By Ben Steverman – Oct 18, 2011 8:13 AM PT

The mortgage-interest deduction may be your favorite tax break, but be aware that it has some impressive enemies. The fiscal commissions of two different Presidents proposed eliminating it, first in 2005 and then in 2010. There's also a steady stream of research from such places as the London School of Economics and the Brookings Institution arguing that the deduction doesn't boost homeownership, but instead provides incentives for wealthier Americans to buy big houses and take on more debt.

That is exactly what it does.

The home mortgage interest deduction does not boost home ownership because the fringe of home ownership is low wage earners who do not itemize and take advantage of it. If the home mortgage interest deduction were eliminated, it would not impact the home ownership rate in any way.

The deduction does encourage high wage earners to take on extra debt because they are compensated with a tax break. This enables them to increase their bids for real estate and bid up prices higher than they otherwise could and would. In other words, the home mortgage interest deduction inflates home prices in places like Irvine, but it does nothing of value for the rest of society who pays for it.

The people who will argue most vociferously to keep this deduction are existing loan owners who take advantage of it in places like Irvine (don't let me down in the astute observations).

Nevertheless, the mortgage-interest tax deduction survives, fortified in Washington by strong housing industry support and its presumed popularity with voters. Now, according to a recent Bloomberg Poll, a growing number of Americans may be willing to end the mortgage tax deduction — as long as they get something in return. Forty-eight percent of respondents said they were willing to give up all tax deductions, including the home mortgage deduction, in return for lower tax rates for every tax bracket. Forty-five percent were opposed in the survey of 997 adults, conducted for Bloomberg by Selzer & Company.

The results represent a significant shift from a December 2010 Bloomberg survey that asked the same question. That poll showed a majority, 51 percent, opposed to giving up tax deductions, with 41 percent in favor. Given the pressure to lower the federal deficit, “everything is on the table,” says Richard K. Green, director of the University of Southern California Lusk Center for Real Estate. “People are so desperate to figure something out that they're willing to consider anything.”

If politicians believe they have political cover, the home mortgage interest deduction may really be in danger. This is the most momentum I have seen for curbing or eliminating the deduction so far.

Lobbyists versus Academics

The mortgage-interest deduction allows homeowners to lower tax bills by deducting interest on home mortgages from their taxable income. Interest on up to $1 million in mortgages on first and second homes is deductible, along with interest on up to $100,000 in home equity debt.

Lobbyists for homebuilders and realtors vigorously defend the usefulness and popularity of the tax break. Lawrence Yun, chief economist at the National Association of Realtors, says the deduction has “lowered the cost of ownership” and boosted the homeownership rate, which he describes as “the foundation for a very stable, democratic country.” As recently as April, a USA Today/Gallup Poll found that 62 percent of respondents opposed eliminating the tax break.

As usual Lawrence Yun is completely wrong. The home mortgage interest deduction has done nothing to boost the home ownership rate for reasons I outlined above. Further evidence of this comes from countries like Canada which have a higher home ownership rate than the United States without having a home mortgage interest deduction.

If the sentiment in previous polls is an accurate reflection of attitudes, many Americans support the deduction without getting a benefit from it. The deduction has a definite high-income tilt: Only about one in four Americans includes mortgage interest on taxes. Renters and homeowners without mortgages have no interest to deduct, while many lower- and middle-class homeowners receive a standard tax deduction and don't itemize.

Dennis J. Ventry Jr., a professor specializing in tax law at the University of California-Davis School of Law, calls the provision, which costs nearly $100 billion a year, “the most inequitable and inefficient provision in the Internal Revenue Code.” The benefits of deducting interest from income increase with a homeowner's tax rate, he notes. Thus, according to a 2011 study co-authored by Green, 46 percent of the deduction's tax benefit goes to households earnings more than $100,000 per year.

Conservatives always decry the progressive nature of the tax code. Well, the home mortgage interest deduction is the most regressive tax break possible. The more the borrower makes, the more the tax deduction increases. Low and middle income Americans don't gain much if any benefit from this tax break, and of course, renters get none at all.

Conservatives always decry the progressive nature of the tax code. Well, the home mortgage interest deduction is the most regressive tax break possible. The more the borrower makes, the more the tax deduction increases. Low and middle income Americans don't gain much if any benefit from this tax break, and of course, renters get none at all.

Unpredictable Effects

Criticizing the mortgage-interest deduction is far easier than calculating the impact of getting rid of it. If, as many argue, the deduction has spurred “overinvestment” in housing, ending the incentive may have negative and unpredictable effects.

The potential hit to the housing economy is a big unknown. Dean Stansel, an economics professor at Florida Gulf Coast University who has studied the deduction for the Reason Foundation, estimates that the tax break inflates housing prices by less than 1 percent; a separate study calculates that it raises prices by 3 percent to 6 percent.

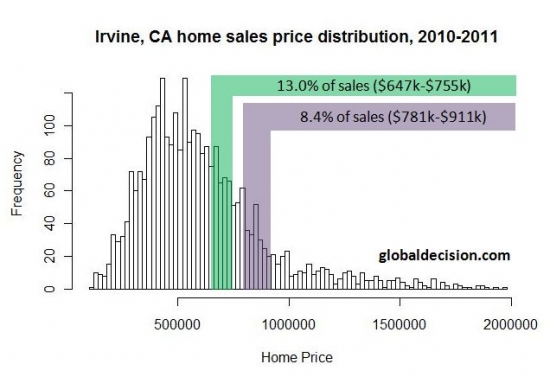

One research paper forecasts serious trouble if the deduction should disappear, predicting that prices could fall from 2 percent to as much as 13 percent, depending on the metropolitan area. Most vulnerable would be parts of the country with higher incomes and higher home prices, which typically benefit most from the mortgage-interest deduction. For example, according to a March 2011 analysis in Tax Notes, residents of Beverly Hills, California, get a $1,873 per person benefit from the deduction, while residents of Clarksville, Mississippi, gain an average of $45 per person.

The research paper mentioned above is probably right. Depending on the area, prices will drop somewhere between 2% and 13%. Locally in Irvine, prices will drop much closer to 13% than 2% because Irvine is much more dependent on the deduction to maintain home values than other areas.

On a personal level, the deduction's biggest beneficiaries will feel the greatest pain if it disappears. Green, of the University of Southern California Lusk Center for Real Estate, estimates that households earning more than $160,000 would pay an average of $2,577 in additional taxes, even after benefiting from a proposed 15 percent tax credit. Places with pricy real estate would bear the brunt of a repeal. “The city of San Francisco would just get whacked,” Green says.

Add Irvine to that list.

Tempting Target

To avoid dire scenarios, Washington would likely do away with the mortgage deduction in a gentle fashion. The tax advisory panel convened by President George W. Bush in 2005 suggested replacing the deduction with a tax credit equal to 15 percent of interest paid. In 2009, the Bowles-Simpson Commission proposed an annual tax credit of 12 percent, limiting interest to first homes and mortgages up to $500,000.

Unlike tax deductions, tax credits can be claimed by all taxpayers, including those who do not itemize their taxes. That could help a greater number of lower- and middle-income people afford houses. Green estimates that a 15 percent mortgage-interest tax credit would boost homeownership by 2.5 percentage points.

I would prefer if we eliminated all tax subsidies on home ownership. Why give a tax credit or a tax deduction? The recent decline in the home ownership hasn't caused any civil unrest, unless you count the occupy Wall Street movement.

Not that I want to see it happen, but I believe Richard Green is right that a 15% mortgage interest tax credit would boost home ownership rates because it would impact the low-income buyers on the fringes.

The mortgage deduction could once again be a target for deficit cutters. According to a 2009 Congressional Budget Office analysis, gradually replacing the mortgage deduction with a 15 percent credit would yield $388 billion from 2013 to 2019. Such savings could prove tempting to the Joint Select Committee on Deficit Reduction, which is charged with finding at least $1.5 trillion in deficit savings over the next 10 years.

The inclinations of this “super committee” are, so far, secret, but the mortgage-interest deduction was discussed at a Sept. 22 hearing. Without making any recommendations, Joint Committee on Taxation Chief of Staff Thomas Barthold mentioned the deduction as an example of a “tax expenditure” that could be eliminated as part of an overhaul of the tax code.

The threat of mandatory deep cuts in defense spending and Medicare if the super committee cannot find enough savings may be the only way that the mortgage interest deduction can die. It's tough to end the tax break, says Green, because the costs are widespread and barely noticed, while the benefits are concentrated in a vocal minority that appreciates the deduction. “It's only in the context of overall reform that you might see something happen,” he says. With public opinion turning, that day may be drawing near.

The circumstances are right for eliminating this deduction. When times are good, eliminating a deduction like this is nearly impossible, but with the realities of a budget ballooning out of control, something has to be done. When something has to be done is when changes as controversial as this one are made.

$7,000 down, $246,00 in mortgage equity withdrawal

The owner of today's featured property demonstrates why houses were so popular during the bubble. The lingering memory of so much free money continues to motivate buyers even today. Fortunately, the crash will grind on, and eventually, people will abandon dreams of free money from houses. When they do, the market will finally bottom.

- This property was purchased on 7/23/1999 for $139,000. The owner used a $132,000 first mortgage and a $7,000 down payment.

- On 3/28/2001 the owner refinanced with a $135,000 first mortgage.

-

On 9/7/2001 he obtained a $25,000 HELOC.

- On 2/18/2003 he refinanced with a $192,000 first mortgage.

- On 6/29/2004 he got a $32,600 HELOC.

- On 12/23/2004 he obtained a $60,000 HELOC.

- On 5/3/2005 he refinanced with a $234,600 first mortgage.

- On 8/30/2005 he was given a $75,000 HELOC.

- On 11/29/2005 he refinanced with a $328,000 Option ARM with a 2% teaser rate.

- On 12/11/2006 he received a $50,000 HELOC.

- Total property debt is 378,000.

- Total mortgage equity withdrawal is 246,000.

There have been no notices filed on this property, but since he is selling short, he likely isn't paying the mortgage. This is shadow inventory. It is the kind of borrower which needs to be flushed from the system and the property recycled. The resulting decline in the loan ownership rate will help out this debtor and the rest of the economy.

——————————————————————————————————————————————-

This property is available for sale via the MLS.

Please contact Shevy Akason, #01836707

949.769.1599

sales@idealhomebrokers.com

Irvine House Address … 402 FALCON Crk Irvine, CA 92618

Resale House Price …… $250,000

Beds: 1

Baths: 2

Sq. Ft.: 900

$278/SF

Property Type: Residential, Condominium

Style: 3+ Levels, Traditional

Year Built: 1999

Community: Oak Creek

County: Orange

MLS#: S676279

Source: SoCalMLS

Status: Active

On Redfin: 4 days

——————————————————————————

Elegant home in gated Oak Creek featuring a spacious master suite, one and one-half baths, two-car attached garage, and sun-splashed deck! Sparkling kitchen features handsome cabinetry, built-in microwave, and dry-foods pantry. Upgrades include custome tile floors in kitchen and baths, designer carpet, and custom window treatments. Master suite features walk-in close as well as master bath with dual sinks and soaking tub. Enjoy resort-style pools, spas, tennis courts and award-winning Irvine schools!

——————————————————————————————————————————————-

Proprietary IHB commentary and analysis ![]()

Resale Home Price …… $250,000

House Purchase Price … $139,000

House Purchase Date …. 7/23/1999

Net Gain (Loss) ………. $96,000

Percent Change ………. 69.1%

Annual Appreciation … 4.8%

Cost of Home Ownership

————————————————-

$250,000 ………. Asking Price

$8,750 ………. 3.5% Down FHA Financing

4.18% …………… Mortgage Interest Rate

$241,250 ………. 30-Year Mortgage

$79,205 ………. Income Requirement

$1,177 ………. Monthly Mortgage Payment

$217 ………. Property Tax (@1.04%)

$100 ………. Special Taxes and Levies (Mello Roos)

$52 ………. Homeowners Insurance (@ 0.25%)

$277 ………. Private Mortgage Insurance

$223 ………. Homeowners Association Fees

============================================.jpg)

$2,046 ………. Monthly Cash Outlays

-$185 ………. Tax Savings (% of Interest and Property Tax)

-$337 ………. Equity Hidden in Payment (Amortization)

$13 ………. Lost Income to Down Payment (net of taxes)

$51 ………. Maintenance and Replacement Reserves

============================================

$1,589 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$2,500 ………. Furnishing and Move In @1%

$2,500 ………. Closing Costs @1%

$2,412 ………… Interest Points @1% of Loan

$8,750 ………. Down Payment

============================================

$16,162 ………. Total Cash Costs

$24,300 ………… Emergency Cash Reserves

============================================

$40,462 ………. Total Savings Needed

——————————————————————————————————————————————————-

Larry Roberts and Shevy Akason will host a first-time homebuyer workshop at 6:30 PM Wednesday, October 26, 2011, at the offices of Intercap Lending (9401 Jeronimo, Suite 200, Irvine, CA 92618). Register by clicking here or email us a sales@idealhomebrokers.com.

Larry Roberts will be hosting a Las Vegas Cashflow property workshop at 8:00 at the same location. Register by clicking here.

What if the current system was to be phased out? Jan.1 201X make all purchases/refis eligable for 15% mortgage interest tax credit, any home purchased prior to that is “grand fathered in” and still eligable under the current tax code. If someone refi’s, they’re no longer eligable. That way you don’t get a brunt of strategic defalters and we still give the new loan owners something to look forward to.

Some kind of grandfather clause or slow transition (i.e. lower the limit $100,000 a year for five years) would certainly help. The problem for most would come when they go to sell. Since the future buyer won’t have the same tax benefits, they likely won’t pay as much, so it will depress resale values.

If you want to avoid mass strategic default by well-to-do borrowers, you have to phase the MID out gradually. I have considered strategic default, but haven’t because my wife is completely disinterested in the thought and because I knew the deal I was getting into. However, if you eliminate the MID the terms of my deal change dramatically (~$1,700 monthly) and therefore my interest in completing my end of the bargain change dramatically too.

e.g. We would go from paying ~$500-$750 above rental parity each month to ~$2,200-$2,450 above it! And, the value of our home would take another huge plunge.

Having said that, the MID and most other housing tax policy is terrible and needs to change. That’s why it should be eliminated, but do it along with a serious revision of the tax code eliminating nearly every other deduction and credit while lowering rates across the spectrum.

…I would prefer if we eliminated all tax subsidies on home ownership…

Exactly! Keep government out of the real estate markets! Let the free markets work!

Another benefit of no HMID is the elimination of all the useless make work for tax accountants.

Those cost saving alone have just got to be substantial.

A couple points on taxes. In California, households start itemizing more quickly than in other states because incomes are higher and the state income tax is high. Therefore, a household making $75K+ may start to itemize because their state income tax exceeds the Standard Deduction.

Also, the AMT starts “taking back” what the Standard Deduction gives at higher income/taxation levels.

Every year I do our taxes in TurboTax, I run an alternative scenario without itemizing mortgage interest and property taxes. Then I know exactly how much benefit the tax code provided us in that year for home “ownership.” In 2010, that figure was ~$1,700 monthly.

Why not just start by eliminating the second home mortgage deduction? This seems like such a no-brainer and surely has political backing by the vast majority. There really is no rational justification for such a deduction and is obviously a handout to the wealthy.

Well, what if you’re earning the CA median household income ($76K?), you’re in your fifties and have no other debt, but you bought and financed a second home for your mom to live in? Is that person wealthy?

Don’t care.

Is there something about median earners, or about mothers, that taxpayers should be funding second homes for the former, or free housing for the latter?

Nope, but I just like to call-out the many instances where people assume others who earn a certain amount or have certain things, are “rich.”

What does your scenario have to do with anything? Of course there are exceptions (like your median income home buyer for mom) but the fast majority of the benefits go to high wage earners.

It’s like saying the Bush tax cuts weren’t a handout to the wealthy. Sure, I got a $400 reduction in my taxes but people making a lot more than me got thousands upon thousands. Same kind of deal.

Regardless of the semantics of the term “wealthy,” there is no public policy rationale for a second home mortgage deduction. This tax incentive policy, for the most part, motivates those with means (and who have already purchased a home) to buy an extra house; thereby artificially driving up housing prices.

according to some blogger comment, if your household makes more than US$40,000/year, you are in the top 1% in the world.

US$11,000/year gets you in 10% richest.

So yeah there’s that.

For the US: What percentage are you calculator

http://blogs.wsj.com/economics/2011/10/19/what-percent-are-you/

Everyone I know who itemizes basically commits tax fraud every year. They itemize car gas for their “work,” office space that they have at home for personal uses, major appliance purchases, sometimes even groceries. They even brag about it but of course with fingers crossed that they never get an audit. And they probably never will. I think it all stems from our national culture of “everybody’s doing it so why shouldn’t I?” MID is a ridiculous handout to the rich but middle class pretenders will do whatever they can to take advantage of it, even though most of them should legally just be taking the standard deduction. The risk of getting busted by the IRS is real and has nasty consequences.

I know many people taking the home office deduction who don’t qualify for it. The requirements are strict, and most people don’t qualify for it. But like you said, they’re gambling and the risks are huge.

Yes the home office rules are insanely strict, too strict in my opinion. Basically you can’t use that space for anything BUT official business. Another common tax dodge is people renting extra rooms for cash and not declaring the rental income. All it takes is a tenant or neighbor to report them and they’re paying tax on market value rent. In those cases it’s actually better to have a paper trail as without one the IRS will gleefully assume you received high market rent for a long time. It’s pretty crazy how much people are willing to gamble for a few extra grand here and there.

That seems like the easy factor to control – you just keep one room as an office/library. The difficult one is the “principal place of business” rule. e.g. My wife works from home 10-20 hours per week in the evenings and on the weekends in a room that is solely used as an office. However, because she has an office provided by her employer, we cannot take the Home Office Deduction.

http://www.irs.gov/businesses/small/article/0,,id=204169,00.html

The home office deduction is one of those “red flags” to the IRS, take it very long and you are sure to get a little black and white envelope in the evening mail.

Cry me a river …

Swiss Banks May Pay Billions, Disclose Names

http://www.bloomberg.com/news/2011-10-24/swiss-banks-said-ready-to-pay-billions-disclose-customer-names.html

Attorney Robert Katzberg, who represents clients in criminal tax cases, said U.S. taxpayers with Swiss accounts don’t understand that the IRS and Justice Department will get a trove of new data on secret accounts.

“There are thousands of Americans, who are the functional equivalent of residents of New Orleans on the eve of Hurricane Katrina, who have no idea that Katrina is about to happen,” said Katzberg, of Kaplan & Katzberg in New York.

You might just have dishonest friends. I itemized my taxes and I have never, ever deducted anything that wasn’t clearly deductable. I think most people are the same way. It isn’t worth losing my self-respect for a couple of thousand dollars.

So, when you deduct your property taxes, do you solely deduct the amount attributable to 1% of the Assessed Value of the home, or do you include all of the other charges including Mello Roos?

When you deduct your auto registration, do you solely deduct the amount attributable to the rate/percentage of the car’s value, or do you include all of the other charges?

When you purchase a product on Amazon and pay no sales tax, do you claim this on your income tax return?

When you sell something that has appreciated (a rare skateboard you’d had for 20 years you sold on eBay for $100), do you claim the income?

Yes to all of above. I’d like to see MID phased out and the only deduction I’d like to keep is the charitable giving deductions…since you are giving the money away anyway, the gov should not also tax it. It is basically reserving some “Ron Paul” type freedom to say where I want the money I don’t keep to go where I want it…not where the gov decides it should go.

I disagree about the Chartible Contributions deductions. I figure if I,or you, or anyone wants to give some money to an organization, it should be their business. Why should the IRS be allowed to determine what constitutes a worthy (read 501-c3) orginization and what does not. If I want to give, and I do, without the behefit of the itemized deduction since my house has long been paid for, that is no ones business, or financial responsibility but my own.

Same with substantially all itemized deductions, personal exemptions and tax credits. Get rid of them. The primary problem with the IRcode, particularly as it relates to personal taxes, is it is as much a tool of social engineering as it is a source of revenue.

The only itemized deduction that makes sense to me is for the cost of uninsured medical care. And the income phase in for that is so high it is practically unusable. It would be better to phase out the deduction for health insurance premiums for business, or make it taxable to the employee and eliminate even the vestage of medical expense deduction.

I guess I could never get elected.

You’re correct, of course but in most cases, doesn’t the IRS simply give a “soft audit”?

So if you receive a refund of 8K and suddenly the IRS wants back 3K, don’t most people just write the check for the 3K and spend the 5?

Hehe to ripcord – not so much friends as acquaintances and co-workers. As far as I know the “soft notice” is usually reserved for under-reported income that’s different from info the IRS receives from employers. Any time you itemize suspiciously that’s a red flag that could lead to an audit. Of course it’s not worth the risk but many people intentionally over-itemize so they can cross above the standard deduction. The IRS is more than happy to charge back taxes with interest plus heavy penalties, and if your tax preparer signed off on those taxes they could lose their license.

Seems unlikely MID would be eliminated. That is like touching social security or medicare – makes the politicans responsible unelectable. Much more likely that the debt will just keep growing, and money will keep being printed (aka a default of sorts via printing).

Fed’s Dudley: Break the ‘Vicious Cycle’ in Housing

http://www.bloomberg.com/news/2011-10-24/fed-s-dudley-calls-for-breaking-vicious-cycle-of-housing-price-declines.html

I don’t believe the MID can be compared to SS or medicare, mainly because most people really don’t stand to benefit from the MID.

The only people who really benefit from the MID are affluent borrowers with large mortgages. Renters obviously do not benefit, but neither do cash buyers, people who have paid off their houses, or those with small mortgages relative to their incomes. Your mortgage must be fairly large before the deduction you get equals or exceeds your standard deductions.

SS and medicare, on the other hand, are life-or-death stopgaps for the majority who have lost their pensions or retirement savings, or who have been unable to save enough to fund even the bare essentials in retirement.

Therefore, I feel that the MID is a safe target politically, and so are other home owner and home buyer assistance programs, most of which are of assistance to no one.

I’m a homedebtor.

That out of the way, my thoughts are:

1.) I agree that the deduction has inflated housing prices unnecessarily, esp. in Orange County. I also think, rightly or wrongly, the deduction has played a major factor in the home buying process for many Americans. I probably would still be renting today if there were no such deduction. (I’d be pissed off though, since I really hated paying my landlord with his shoddy upkeep efforts, all of his pedantic annual 5% rent hikes, constant bargaining for basic repairs, and threats of moving ever year, etc.)

2.) If the deduction were removed from the US tax code, then perhaps its best for a growing % of Americans to simply rent a nice house or apartment forever. I mean, that way you’re not taking on too much debt, there’s no ball and chain on you, so you have financial liberty to borrow for things “your really need” like starting a business, etc., and you have freedom to move around for new employment opportunities, etc.

3.) They should remove the tax exemptions surrounding property taxes too while they’re at it. I mean, seriously, why should loan-owners be protected from that when the renter of a SFH is basically paying these property taxes on the loanowners’ behalf anyway (via rent) and get no such “tax benefit”?

4.) I know it would not be the end of the world.

France, Canada and I think the UK do not allow such mortgage interest deductions either. I could be wrong, but believe more people rent in those societies.

5.) What about the capital gains exemptions when a house (primary residence) is sold? Should that benefit be rescinded too? If so, I think the financial benefit of renting would overwhelm that of loanowning. Of course, prices would decline, so actual rental parity in a place like Irvine, California would finally enter the “really interesting” territory.

“you have financial liberty to borrow for things “your really need” like starting a business, etc.”

Have you ever tried to borrow for a business without owning a property the bank can put a lien on? It can be done, but you may find it is more difficult then you think.

Will this increase the rents for private rentals?

Does anyone think this will lower home prices proportionately?

Sounds like that “high interest/automatic lower prices” theory again.

Not going to happen, you won’t win the elections by putting further pressure on house prices, since 65% of households or so own real estate. People think about their own benefits first before they consider others and eliminating the deduction would most likely add dwonward pressure to the current prices.

65% may own houses, but only 40% have mortgages, and of that 40%, not all take the HMID. The HMID clearly benefits a small minority.

Us minorities deserve protection too!

The US is completely broke and the spending/borrowing continues, so I don’t think anyone can say it will never happen.

The articles I’ve read state an estimated savings of US$100 billion per year if the MID were eliminated.

http://www.bloomberg.com/news/2011-10-17/a-taxing-debate-the-mortgage-interest-deduction.html

Looking at either the 2010 or 2011 US budget, $100 billion of extra revenue could theoretically almost halve our dedicated budget spent on net interest on US debt (currently $251 billion):

http://www.nytimes.com/interactive/2010/02/01/us/budget.html

If this were implemented, then they should put the money to good use, pay down the national debt and strengthen the US dollar.

Quoting Larry;

“Anyone out there who believes it is a good idea to spend $1 to receive $0.25 in return, please send me as much money as you wish, and I promise to send back 25% of it.”

Ii would like to publicly state that I am more generous than Larry. I will make the same offer, only I will send back 30% of any money sent to me.

Please contact me as soonb as possible to start our wonderful new relationship.

Eliminate the MID?

Over (the hands of) my cold, dead body.

House prices would plummet another 25%… We just bought a home a would lose $400+ in interest deduction per MoNth! Thats a lot of money for a family of 4 earning $100k… In los angeles! You would have to lower sales tax, property taxes, ect… It would cause a hige increase in rent prices cause i would sell my home and rent… Rental market would become saturated… The economy would take a huge hit… That would be $5000-6000 year my family wouldnt spend.

I make $56k per year, own a small farm and itemize my taxes. It is not factual to state or imply that only X group of people making over X amount, itemize.

The need to get rid of the deduction and add in a National Property and Asset Tax. This would then allow us to reduce taxes based on income and sales.