Despite the best house price payment affordability on record, housing demand and mortgage demand is near record lows.

Irvine Home Address … 2 SOLANA Irvine, CA 92612

Resale Home Price …… $465,000

Get on up when you're down

Baby, take a good look around

I know it's not much, but it's okay

Keep on moving anyway

Five — Keep on Movin'

Despite gargantuan efforts by government policy makers and the federal reserve to prop up the US housing market, low prices in many markets, and low interest rates, buyer demand is still very low. The reason is simple, the buyer pool is depleted, and many who would ordinarily be in the market for housing are unable to qualify for the loan necessary for them to purchase.

Tighter lending standards are often blamed, but it is both a combination of higher lending standards and fewer people who meet those standards because they have credit or savings problems due to unemployment, short sale, or foreclosure. The only fix to this problem is time. People need to go back to work, pay their bills, save money, and wait for their credit score to improve. Until all of those things happen, mortgage demand will remain low, and sales will suffer.

House Affordability in U.S. Rises to Record Levels, Tight Financing Still Constrains Sales

Posted by Michael Gerrity 05/25/11 10:27 AM EST

According to the National Association of Home Builders/Wells Fargo Housing Opportunity Index (HOI) report released this week, nationwide housing affordability during the first quarter of 2011 rose to its highest level in the more than 20 years it has been measured.

The HOI indicated that 74.6 percent of all new and existing homes sold in the first quarter of 2011 were affordable to families earning the national median income of $64,400. This eclipsed the previous high of 73.9 percent set during the fourth quarter of 2010 and marked the ninth consecutive quarter that the index has been above 70 percent. Until 2009, the HOI rarely topped 65 percent and never reached 70 percent.

Low interest rates are making houses in most markets in the US very affordable on a payment basis. Of course, prices in many markets are still too high, but the ability to obtain extremely cheap debt is making the large mortgage balances manageable.

Despite how inexpensive it is to borrow money right now, nobody seems to be doing it.

Mortgage originations down 35% in first quarter

by KERRI PANCHUK — Tuesday, May 31st, 2011, 3:08 pm

Mortgage originations in the first quarter fell 35% to $325 billion, breaking three consecutive periods of growth and threatening to plunge the market back to 2000 levels, according to a report from Inside Mortgage Finance.

The first-quarter drop is the worst experienced since the onset of the recession when mortgage originations plummeted 31.5%, according to a new research report from Federal Reserve Bank of Cleveland researchers Yuliya Demyanyk and Matthew Koepke.

The same report cites Mortgage Bankers Association projections which estimates mortgage originations could fall to $1.05 trillion in 2011, the lowest level in 11 years.

The report blames a decline in refinancings for the dip in originations. Since refinancings generally contribute to higher origination activity, a drop-off in that segment negatively impacts originations as a whole.

The Cleveland Fed Bank report concludes that the only way around declining activity in the refinance segment would be to generate more activity in new home originations—a development the report doesn't foresee when considering the current lull in home starts and the state of the overall housing market.

Write to Kerri Panchuk.

With a long and deep recession at the conclusion of a massive borrowing binge my US consumers, very few people qualify for mortgages. Since interest rates have been low for a long time now, everyone who can refinance already has. As the Cleveland Fed noted, the prospects for increasing new home originations isn't very promising.

Americans Shun Cheapest Homes in 40 Years as Ownership Fades

By Kathleen M. Howley — April 19, 2011, 9:12 AM EDT

April 19 (Bloomberg) — Victoria Pauli signed a one-year lease last week to stay in her rental home in Fair Oaks, California. She had considered buying in the area, where property prices have slumped 57 percent since a 2005 peak.

In the end, she decided it wasn’t worth it.

“I know people who have watched their home values get cut in half, and I know people who are losing their homes,” said Pauli, 31, who works as a property manager for a real estate company. “It’s part of the American dream to want to own your own home, and I used to feel that way, but now I tell myself: Be careful what you wish for.”

Those are the kind of statements that bring out my contrarian instincts. In markets down more than 50% from the peak, prices are generally much lower than rental parity. People in those markets are paying a premium to rent to avoid what they fear is downside risk. Most of the decline has already occurred, and saving money versus renting is a strong inducement to purchase a home. People in beaten down markets are reacting in fear when they should be seizing opportunity.

In markets like Irvine where prices are off by about 25% and most properties are still trading above rental parity, renters still save money, and the likelihood of further declines is higher. An attitude of wait-and-see is appropriate particularly since the financial incentive favors renting rather than owning.

The most affordable real estate in a generation is failing to lure buyers as Americans like Pauli sour on the idea of home ownership. At the end of 2010, the fourth year of the housing collapse, the share of people who said a home was a safe investment dropped to 64 percent from 70 percent in the first quarter. The December figure was the lowest in a survey that goes back to 2003, when it was 83 percent.

After five years of falling prices, I am amazed that 64% of respondents still perceive a house as a safe investment. What would it take for those people to say it's unsafe?

“The magnitude of the housing crash caused permanent changes in the way some people view home ownership,” said Michael Lea, a finance professor at San Diego State University. “Even as the economy improves, there are some who will never buy a home because their confidence in real estate is gone.”

Worse Than Depression

Historically, homes have been a safer investment than equities. During 2008, the worst year of the housing crisis, the median U.S. home price declined 15 percent, compared with a more than 38 percent plunge in the Standard & Poor’s 500 Index.

Americans stay in their homes for a median of eight years, according to the National Association of Realtors in Chicago. Someone who bought a home in 2002 and sold in 2010 saw a 4.8 percent increase in value, based on the annualized median price measured by the group. The average annual gain in the past 20 years was 4.2 percent.

There is another NAr statistic that serves their purposes now, but in years to come, it will not. Wait until we have the 2006 to 2014 comparison. That one will be brutal.

Falling prices have made real estate the best buy in at least four decades. Housing affordability reached a record in December, according to National Association of Realtors data that go back to 1970. The group bases its gauge on property prices, mortgage rates and the median U.S. income.

Despite the fact that much of the NAr data is manipulated bullshit, housing affordability is near its record high, particularly in markets like Las Vegas where you have the unique combination of prices from 15 years ago and very low interest rates.

The median U.S. home price tumbled 32 percent from a 2006 peak to a nine-year low in February, data from the Realtors show. The retreat surpassed the 27 percent drop seen in the first five years of the Great Depression, according to Stan Humphries, chief economist of Zillow Inc., a Seattle-based real estate information company.

For real historical accuracy, the big plunge in real estate prices occurred prior to the Great Depression during the severe recession of the 1910s. They fell again during the mid 20s when the Florida land boom went bust. And during the Great Depression, many people lost their homes in foreclosure, but prices were already beaten down from the turmoil of the two decades preceding. The Robert Shiller chart shows the decline of the 1910's clearly.

Ironically, it was financial innovation of a sort that propelled prices back to their historic trendlines after World War II. What was that innovation? The widespread use of the 30-year fixed rate mortgage with a 20% down payment. Prior to that most loans were interest-only with a 50% down payment requirement. If the real estate community is complaining about 5% down payments, imagine what would happen to the housing market if 50% down became the norm.

Not Risk-Free

“If we’ve learned anything from this mess, it’s that housing is not a risk-free investment,” said Michelle Meyer, a senior economist at Bank of America Merrill Lynch Global Research in New York. “Everyone knows someone underwater in their mortgage or struggling to sell a home.”

About 11 million U.S. homes were worth less than their mortgages at the end of 2010, according to CoreLogic Inc., a Santa Ana, California-based real estate information company. An additional 2.4 million borrowers had less than five percent equity, meaning they’ll be underwater with even slight price declines, according to the March 8 report. The two categories add up to 28 percent of residences with mortgages.

Nearly one in three. It reminds me of the speech they give incoming freshmen in college. Look at the person sitting to your left and to your right. One of those people will not graduate. Well, any homeowner who isn't underwater need only look at his neighbor to the left or neighbor to the right to see someone who is underwater.

… Improving Employment

“We expect that purchase activity will pick up slowly as the improvement in the job market eventually leads to greater willingness to buy,” the mortgage bankers group said.

Willingness isn't the problem: meeting the qualification standards is. The unemployed must find work, then they must maintain it for two years before someone will give them a loan. And that assumes they didn't wipe out their reserves while they were unemployed and damage their credit.

Borrowing costs are at historic lows. The average U.S. rate for a 30-year fixed mortgage was 4.69 percent last year, the lowest in annual data going back to 1972, according to mortgage financier Freddie Mac, based in McLean, Virginia. The rate in March was 4.84 percent, the company said.

By 2012’s fourth quarter, the average fixed rate may rise to 6 percent, according to the Mortgage Bankers Association.

I've been predicting higher interest rates for quite some time, but the lack of demand and ongoing mortgage debt deflation is forcing rates downward.

I have been contemplating the meaning of the chart above. As long as mortgage debt levels are elevated about collateral value, banks have two options: (1) write off the debt to reduce it to the value of the housing stock, or (2) make debt so inexpensive that people can afford to keep their bad debt alive. Obviously lenders are choosing the latter. It's the approach the Japanese took since the early 90s, and housing has been deflating there ever since.

Since lenders are trying to minimize their losses on paper, they are offering debt at super low prices. They can underwrite loans at low rates as long as the federal government guarantees it all and investors don't find a better place to park their money. Right now, competing investments with more risk are not attractive to investors, so they are putting their money into 4.5% loans. Investors will probably stop doing that once there are more economic opportunities. I thought the October 2010 selloff was a sign that the economy was mending and interest rates would keep rising. So far, that has not been the case.

“If you can jump through the hoops to get a mortgage, and there will be hoops, then this is an amazing time to purchase real estate,” said Robert Stein, a senior economist at First Trust Portfolios LP in Wheaton, Illinois, and the former head of the Treasury Department’s Office of Economic Policy. “There are going to be a lot of people kicking themselves a few years from now because they didn’t take advantage of the low prices and the low mortgage rates.”

Tighter Lending

Cheap financing hasn’t done enough to boost home sales in part because lenders are being more selective with applicants, according to Federal Reserve Chairman Ben Bernanke. Fed policy makers have described the housing market as “depressed” in statements following their last eight meetings.

More selective with applicants! LOL! You mean banks aren't loaning home to anyone with a pulse? Shocking!

“Although mortgage rates are low and house prices have reached more affordable levels, many potential homebuyers are still finding mortgages difficult to obtain and remain concerned about possible further declines in home values,” Bernanke said in Congressional testimony last month.

The share of banks reporting tighter mortgage standards in the first quarter rose to 16 percent, the highest since 1991, according to the Fed’s Senior Loan Officer Survey.

Standards are tightening and will continue to tighten until houses are affordable under conservative lending metrics. Bankers don't become aggressive until they stop losing money. The credit cycle exacerbates the economic cycle by making booms larger and busts worse.

Federal regulators are proposing rules that may make lending even more stringent, including a requirement that banks and bond issuers keep a stake in home loans they securitize if the mortgage borrowers have imperfect credit and down payments of less than 20 percent. Borrowers who don’t meet the criteria would pay higher rates to compensate lenders for risk.

Fannie Phase-Out

As mortgage requirements rise, rates could follow as Congress and the Obama administration consider phasing out government-controlled Fannie Mae and Freddie Mac. The companies hold federal charters mandating they increase the availability of mortgages through securitization. In Fannie Mae’s case, that order goes back to the Great Depression, when it was created as part of President Franklin D. Roosevelt’s New Deal.

“There are a lot of unsettled policy issues on the table right now that, if they’re not handled right, could further set back the housing market,” said Richard DeKaser, an economist at Parthenon Group in Boston. “Fannie and Freddie have historically lowered interest rates, and eliminating them will increase the cost of home ownership.”

I'm not sure if that is an argument to keep them or eliminate them. I think he was trying to make the case for keeping them around, but providing artificial props to the housing market with risk to the US taxpayer is a bad idea, and the GSEs should go away.

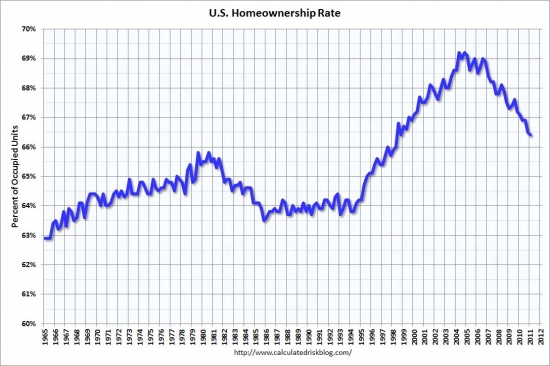

Lowest in Decade

The U.S. home ownership rate dropped to 66.5 percent in the fourth quarter, the lowest in more than a decade, according to the Census Department. The rate probably will retreat another percentage point by 2013, according to Meyer, of Bank of America Merrill Lynch, and Lea, the finance professor. That would put it back to a 1997 level.

“People will still aspire to own their own homes,” Lea said. “They’ll just be a lot more practical about it.”

Pauli, the California renter, said she has no such aspirations, at least for now. She pays $1,500 a month for her three-bedroom, single-family home with a two-car garage, granite kitchen countertops and stainless-steel appliances. Her neighbors who bought before the housing crash typically have mortgage payments of about $2,800 a month, Pauli said.

“I don’t see myself purchasing, even with all the great prices I see,” Pauli said. “Going to bed every night worrying about your home value doesn’t sound like a good time to me.”

And Pauli will continue to feel that way until owning becomes less expensive than renting. Rental parity is a tipping point, and once prices fall below that level, fence sitters get off the fence and buy properties. The specter of price declines is less powerful than the desire to lower monthly housing costs, except for those people with a short ownership tenure.

Not a short sale… yet

A property owned for the last 15 years by one family would not ordinarily be a short sale candidate. With the $169,000 sales price and a $152,100 first mortgage, it is reasonable to believe their mortgage balance should be less than $100,000.

Of course, this is Irvine, California, so their loan balance is over $100,000; in fact, the last mortgage on the property was for $399,000. Instead of having $300,000+ in equity, these owners have limited ability to lower their price before they will be a short sale statistic.

When a HELOC abuser makes a sale for a $268,100 profit and only gets a $26,810 check at closing, how do they feel? Does it cross their mind that they pissed away a quarter million dollars? Any regrets?

Irvine House Address … 2 SOLANA Irvine, CA 92612 ![]()

Resale House Price …… $465,000

House Purchase Price … $169,000

House Purchase Date …. 10/1/1996

Net Gain (Loss) ………. $268,100

Percent Change ………. 158.6%

Annual Appreciation … 6.9%

Cost of House Ownership

————————————————-

$465,000 ………. Asking Price

$16,275 ………. 3.5% Down FHA Financing

4.54% …………… Mortgage Interest Rate

$448,725 ………. 30-Year Mortgage

$97,899 ………. Income Requirement

$2,284 ………. Monthly Mortgage Payment

$403 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$97 ………. Homeowners Insurance (@ 0.25%)

$516 ………. Private Mortgage Insurance

$384 ………. Homeowners Association Fees

============================================

$3,684 ………. Monthly Cash Outlays

-$368 ………. Tax Savings (% of Interest and Property Tax)

-$587 ………. Equity Hidden in Payment (Amortization)

$27 ………. Lost Income to Down Payment (net of taxes)

$78 ………. Maintenance and Replacement Reserves

============================================

$2,836 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$4,650 ………. Furnishing and Move In @1%

$4,650 ………. Closing Costs @1%

$4,487 ………… Interest Points @1% of Loan

$16,275 ………. Down Payment

============================================

$30,062 ………. Total Cash Costs

$43,400 ………… Emergency Cash Reserves

============================================

$73,462 ………. Total Savings Needed

Property Details for 2 SOLANA Irvine, CA 92612

——————————————————————————

Beds: 2

Baths: 2

Sq. Ft.: 1404

$331/SF

Property Type: Residential, Condominium

Style: One Level

View: City Lights, Park/Green Belt, Trees/Woods

Year Built: 1975

Community: Rancho San Joaquin

County: Orange

MLS#: S659422

Source: SoCalMLS

Status: Active

——————————————————————————

Location!Location! Enjoy warm southern sun exposure, amazing golf course views, magnificent large old trees and endless golf course lawns. Charming home in the prestigious golf course community of Rancho San Joaquin. Premium private corner, ground location on the Green Belt single story home boasting amazing views and a very light spacious open floor plan. Two spacious Master Bedroom Suites. Two patios to enjoy while entertaining and relaxing. Enjoy a quiet Community Pool and Spa, inside washer and dryer and detached two car garage. Close to Mason Park, Shops, Restaurants, UCI, University High and much much more. Award Winning School District! Washer, Dryer and Refrigerator included. STANDARD SALE! A MUST SEE!

Is it really surprising that housing demand is at a low when affordability is at its best? We had housing demand at its peak when affordability was worst. Maybe people are not just using affordability and making rational decisions.

Willingness to buy is a huge factor. Think about the bubble. It took a willingness to believe that house prices would continue to rise, and devote an outsized portion of your income and/or take on a mortgage with unconventional payment terms.

At bubble’s peak, nearly 50% of transactions were for non owner-occupied homes. At that point, affordability is not really a significant point. That transaction volume has not returned, and requires a shift in sentiment on housing.

You also have the idea of whether people are willing to put a majority of their nest egg into one investment that has recently done poorly. Willingness and sentiment are important.

While your observation about 50% of transactions were for non-owner-occupied homes may be correct, you need to factor in WHERE that was occurring and who was making those RE loans.

Take metro Phoenix, please, as an example. Bcuz a “rental home” is taxed with a property/sales tax differently than a “residential home” which is not; almost all of those non-owner-occupied homes were listed for property/sales tax purposes as “occupied”. The GD lying tax cheats!

So, in the sand states – Cal, Nev, AZ & Fla; all of those very bad ARMs & subprime RE loans were made during the dead year – 2003-2007; by Countrywide, WAMU, Wichovia & New Century. And, at the same time “low-down-no-down” investors were buying anything and everything – everybody assuming that the prices would go up, they would pay out little or no money AND make their fortune.

While some of that may have occurred where you and the rest of U.S. live, most of it was in those four states, plus Georgia and Texas.

That was then, this is now. That was there, most of it is now gone. The rest of U.S. were different, now we are not.

But, you cannot – as in economically and morally should not – mix up apples from Eastern Washington with the oranges and other citrus “fruits” from Cal, Az and Fla.

See, what happenes in Nevada did NOT stay in Nevada.

I agree with you, and the other stat that I remember was 85% of Miami condos being non owner-occupied. I tried to convey to others in NC the madness of the sand-state RE markets during the bubble, but because things were not too overheated here, it was difficult to understand. I also tried to convey the size of the problem. CA & FL are quite large markets. You can still see the geographical dependence. The county I grew up in has 18% of loans >90 days past due. The neighboring county (Dade) has 22% 90+ days late.

One thing I thought of is geographically dependent mortgage rates. If home prices are going up 10%/yr, you will tolerate a higher interest rate than someone whose home price is flat. Then, banks are compensated for risk to collateral, and it serves as a natural dampening mechanism for prices.

I’m trying to sell two houses in rural Oregon within 25 miles of a Pac 10 University. One is on about 2 acres and one on abut 3/4 acre. We got them on the market in April, and we’ve gotten nada in the way of interest. We’ve priced them based on appraisals, but we’re not getting any traffic. My Wife thinks people are leery of living too far from town because of the surge in gas prices, but I think it’s bigger than that. There just isn’t a lot of confidence in the economy. And people aren’t chucking it all, cashing in their savings, dropping out and moving to the woods, either. But if any of you want to do that, just reply to this post.

Fortunately, I’m not indebted on either property. I have an old 78 rpm disc by Hattie Noel called “If I Can’t Sell It I’ll Keep Settin’ On It”. Maybe that’s what I’ll have to do.

Joe

Never mind “willingness” to buy. What people lack now is the ABILITY to buy.

Had credit standards been maintained for the past 20 years, most homebuyers in that period would have had to sit it out because they lack down payments. Most people in this country have lived paycheck to paycheck for years as middle and lower-middle incomes stagnated, and personal debt levels rose since 1980.

We are now in a deflationary climate, one of eroding asset values. The stock market remains levitated by the offices of the Fed, by pushing interest rates to absurd lows and destroying savers and fixed-income investors, and forcing them to take elevated levels of risk just to get a small return on their savings. But look out below- there has never been so much insider selling as in the past years and the equities markets look very, very fragile, at least to me.

Deflation results in lower asset prices but even lower incomes, which means that even though the price of housing may drop even more, homes could be even LESS affordable, not more; because incomes are dropping even more, and credit is tighter. We might be coming upon such a time.

You obviously have no experience or understanding of the upper crust of society. Maybe Chicago is pockmarked by the broad-backed under-educated masses, but here in Irvine, life is different. Unlike your swarthy destitute immigrants, in Irvine there is an infinite line of wealthy FCB’s clamoring for a slice of the good life: a home in Turtle Rock, and enrollment of their violin-virtuoso children in the unparalleled, world-renowned public school system.

Perhaps you might consider leaving your sinking, rat-infested ship along the “Great” Lake Michigan and move out west, but I hesitate to suggest this considering you are likely far from becoming Irvine material. If you don’t have a medical or engineering degree, and are too old/unintelligent to start that track, you might have luck marrying a Chinese engineer and beginning the slow process of moving up toward the upper echelon of Irvine living. No guarantees, mind you, but even the glimmer of hope of someday living in Irvine–deluded a hope as it may be for folks like you–may be enough to get you through a slightly less dismal life.

Failing that, feel free to come visit the IRVINE SPECTRUM CENTER anytime, where every day is like Christmas and Halloween, and the professional classes clink glasses brimming with delicious extravagance at world-class restaurants like P.F. Chang’s and Rubio’s Fresh Mexican Grill.

Cheers!

Hilarious!

Indeed, the feet of the Irvine classes never touch the ground – the hot asphalt would just burn their tootsies anyway. Husband, wife, and high-achieving Asian children – such are adopted if the couple is unable to produce Asian children naturally – enter the attached garage each morning, gliding past the doctoral, engineering, and medical diplomas lining the end of the hallway. SUVs float them through the streets of the Divine City, to their high-six-figure engineering jobs or schools of high achievement.

Whether on the weekdays or the weekend, the doors of said SUVs never open until the concrete parking garage or the Spectrum is attained. The windows? Only to take in the collations offered by that exclusive Irvine institution, Starbucks, or other products offered in such drive-through emporia as can be found only in the City Where the Real Estate Market is Different Here This Time.

I had the pleasure of meeting P.F. Chang himself. A rare man of much discernment, he made no secret of his desire to keep his creations exclusive to Irvine. Only those of high moral fiber and worldly achievement unheard of elsewhere will ever enjoy such repasts.

Between the astute observations of Planet Surreality and HydroCabron, I can’t stop laughing….

California house prices are still insanely high in absolute terms.

I know the spendthrift American Way is to only look at monthly payment amount (same with cars), but when it takes dual incomes and 30 years to pay off a mortgage, prices just don’t make sense.

Bank lending officers are being complete pricks with mortgage applications in the Bay Area, so expect dwindling transaction volume.

BTW, love the flames pic above.

You need to open your eyes outside of the premium bay area.

90% of America does not require dual incomes or a 30 year mortgage.

Also open your eyes to what is around you. Plenty of stay at home moms in Pal Alto with their VC working husbands.

Your generalizations are completely ridiculous. When you get the chance can you let everyone know the optimal square footage and San jose apt complex everyone should set their sights on so they don’t live seeking to quench their vanity?

“Your generalizations are completely ridiculous.”

and

“90% of America does not require dual incomes or a 30 year mortgage.”

http://www.prb.org/Articles/2003/TraditionalFamiliesAccountforOnly7PercentofUSHouseholds.aspx

http://www.mybudget360.com/the-middle-class-two-income-trap-–-two-breadwinners-plus-extra-money-to-support-the-banking-industry-how-middle-class-americans-are-losing-ground-by-supporting-the-financial-sector/

http://www.doctorhousingbubble.com/the-fallacy-of-cheap-home-prices-dual-income-trap-home-prices-over-valued-by-25-percent/

Cry me a river with that blogging analysis. My household is not dual income is yours? housing expense is 15% of my income. I’m not special.

I understand that you are more comfortable with exaggerations, “Cry me a river”, than facts, but …

The facts are that the average US houshold spends 34% of their annual income before taxes on their paycheck and most of them are two income households.

http://www.usnews.com/opinion/articles/2009/07/13/the-average-american-consumer-over-30-percent-of-income-spent-on-housing

Check out the NYTimes Interactive census map. This link is to Irvine mortgages consuming > 30% of income. Lots of tracts where more than half of households spend > 30% on housing.

I’d guarantee you’re not the only one-income household spending 15% of your income towards housing, but that does not mean that you are closer to the norm than a two-income household paying 30% of their income.

Analysis by anecdote is not real analysis.

Once again, all we get from Planet Realty is conjectures. Please show us the stats for:

– “90% of America does not require dual incomes or a 30 year mortgage”

– “Plenty of stay at home moms in Pal Alto with their VC working husbands”

You continue to make these and other statements that are counter to any actual statistical data without ever providing any real data that supports your claims. Maybe if you actually provided some data that support your claims, you’d actually have some converts. This – and the fact that you continue to degrade and attack the respondents rather than just stating your objections – is the reason you are taken here as nothing more than a troll.

There are ‘plenty’ of sahms in my neighborhood, and my neighborhood also has 27 homes under construction (out of 286 total lots, with roughly 150 homes completed).

However, I’m smart enough not to extrapolate from that limited data to the conclusions: most mom’s don’t have to work, and there’s a construction boom going on.

“Your generalizations are completely ridiculous. When you get the chance can you let everyone know the optimal square footage and San Jose apt complex everyone should set their sights on so they don’t live seeking to quench their vanity?”

I never imagined I would be accused of being vain for buying in Foothill Ranch. I can only imagine what I would be called if I moved back to Newport Beach!

PR:

1) This blog (IHB) is not about 90% of America … it’s about Irvine. The Bay Area has comparable prices and is in the same state, so I don’t mind comparing the two.

2) Palo Alto is a very small town in the Bay Area with especially high prices in a flood plain. Not sure why people keep referring to it as representative of the Bay Area.

3) Don’t confuse my objection to loanowner excuses (claiming rental parity when it’s silly to do so) with jealousy … I wouldn’t move to Irvine even if you gave me a free house there.

I like this reply because its opinion without attacking someone else.

@ Walter – YES, without a doubt it was vanity buying in Foothill Ranch. You could have purchased in Santana or Garbage Grove, or Mission Pendejo(accomplished).

F.R. does have access to the Whiting Ranch and other areas to hike, bike, etc. I make it a habit a few times a week to go up on those hills and piss in the direction of all the homes (I do change the direction I’m pointed to be equal opportunity). Ahhhhh… gotta luv the outdoors 🙂

Hello SJR! I am not sure the two areas are that comparable; surely Palo Alto has the incomes to support the prices, in many cases. I agree that the house prices are ridiculous, but I don’t think that PA is the same epicenter of sub-prime and Alt-A loans that Irvine is.

Let’s see who can pay the incomes needed for these prices:

Irvine: UCI, Broadcom, TIC, Hyundai and others I don’t know about.

Palo Alto: Stanford, Oracle, Intel, Apple Google Nvidia etc etc etc.

Do we have any statistics on HELOCs in the Bay Area? That would be interesting.

I’ve lived in both areas, so would find direct comparisons of apples to apples interesting.

The sweet spot up here for FCBs in trophy school districts (Palo Alto/Cupertino/Saratoga/Los Altos/Menlo Atherton) is $2M-$3M. sub $1M is a bloodbath of HELOCs and foreclosures – just take a spin through FR or Trulia to see what I mean.

I kind of like this SanJoseRenter vs. Planet Reality match up. This could develop into to a NoCal, SoCal rivalry.

Some of their points make sense, some are just unsubstantiated blah, blah, blah.

OK, I will get back to being vain in my Foothill Ranch track house.

. It reminds me of the speech they give incoming freshmen in college. Look at the person sitting to your left and to your right. One of those people will not graduate.

Can I just say that I remember this pitch word for word. I was 17 at the time and felt incredibly deflated. You didn’t happen to be at Cal Poly SLO did you? They gave this speech everywhere???

Yep, they did. I am not really sure why they do this (what it is supposed to achieve), but it’s completely boilerplate.

LOL. At my spouse’s law school they told each incoming class at orientation: “Look at the person sitting to your left. Look at the person sitting on your right. At least one of you is looking at your future spouse.”

Oops. The last sentence at SLO was…”two of you won’t be here at the end of your freshman year.”

Holy financial clusterFark, Batman!!!

PMI = $516

correct me if I am wrong, but my understanding is that the PMI associated with FHA financing requires that it be paid for a minimum of 5 years. Also, you cannot make extra payments to build equity in order to shorten the lifespan of the PMI. Add to that $516/mo the HOAs and you could easily spend $750+/mo on nothing! Well, at least with the HOAs you get a little….pool, amenities, structure maintainence, etc. The total PMI after 5 years is almost 31K. Young families will have a very difficult time coming up with that kind of monthly expense when they have to pay the mortgage/rent and daycare.

I’ll offer $179,000 for the home pictured. They can take it or leave it.

The PMI on FHA loans is now 1.15%. It’s higher than property taxes in many places including California. It pushes a 4.5% interest rate to an APR of 6%. FHA is the replacement for subprime, and the risk is being prices appropriately.

IR, how do you assess rental parity for Irvine? Based on the properties I’ve looked at, there is rental parity if you assume that the buyer puts 20% down and the opportunity cost for the downpayment for a buyer on the sidelines is the equivalent of putting money into a bank CD i.e. 1%.

You can use the same Monthly Cost of Ownership formula as IR, just recalculate for 20% and leave off the PMI.

+ Monthly Mortgage Payment

+ Property Tax (@1.04%)

+ Special Taxes and Levies (Mello Roos)

+ Homeowners Insurance (@ 0.25%)

+ Homeowners Association Fees

+ Lost Income to Down Payment (net of taxes)

+ Maintenance and Replacement Reserves

– Tax Savings (% of Interest and Property Tax)

– Equity Hidden in Payment (Amortization)

Not sure I’d agree with using a rock-bottom risk free investment return as the op cost of down payment though. Very tiny percentage of americans are debt free; think credit card balances and auto loans. Plus I imagine a lot of those saving for a down payment are forgoing investments like 401K, etc that would average better than risk-free.

Actually, I did use the monthly cost of ownership formula as IR in my comparisons. BTW, this might be an opportunity to thank IR for that calculator, which I’ve used many times. The reason I used a 1% investment return is from the perspective of a prospective buyer today – who would like the flexibility of being able to buy within a year, but cannot put it into riskier investments that run the risk of return of principal rather than the return on principal. Personally, my opportunity cost is higher than the 1% since I’ve been moving the down-payment in and out of bonds. Whether people have other debt is not important in comparing rent vs buy. Also, those who are saving for a downpayment are not going to put that money into 401K anyway since it’s not like they can suddenly decide to divert it for a downpayment and expect to have sufficient funds. Therefore, I don’t believe that equation should affect the opportunity cost.

BTW, I agree that things look more tenuous if you assume 10% downpayment and PMI and/or Mello-Roos, which is why I asked IR what his assumptions were. And whether that has been an appropriate metric to use for previous cycles.

In the formula I developed for assessing opportunity costs, I make the assumption that the interest rate of liquid assets someone would use for a down payment is earning less than mortgage debt. Intuitively this makes sense because the same bank that pays interest on deposits is loaning that money out in mortgages, and there needs to be a spread for the bank to make money. My current opportunity cost is low because interest rates are so low.

For people who are savvy investors who can make better returns, the opportunity cost is much higher. For those who can consistently outperform the cost of mortgage debt, they should actually minimize their down payments and tie up as little of their investment capital as possible. Of course, to consistently outperform mortgage interest rates without significantly higher risk is easier said than done.

IR, the mythical banking titan you imagine has some other characteristics. If they’ve been outperforming mortgage rates, then they probably have a lot of cash or liquid assets to use for a DP. Also, they know that you can’t outperform risk-free assets (GSE mortgages are default-risk free no matter what people tell you) without taking on additional risk. It might be hidden and not pop up for a while, but the risk is there. The idea of can’t miss investments should have died with the ‘home prices only go up’ myth.

” … they should actually minimize their down payments and tie up as little of their investment capital as possible.”

I dunno. Maybe they should, maybe they shouldn’t. I have a difficult time telling those who are good with money what they should or shouldn’t do.

Personally, the purchase of a home will be an expenditure, not an investment and the idea of borrowing money for an expense is not appealing. So, we will probably use a 100% down payment.

IR,

Thanks – I in fact assumed an even lower return on downpayment (1%) than you did in your calculator. The assumption was indeed that was for a prospective buyer, the risk is high to achieve higher returns than bank CDs in a low-interest market period -I’m doing modestly better but that’s as much risk as I’m willing to take with the downpayment.

“Personally, the purchase of a home will be an expenditure, not an investment and the idea of borrowing money for an expense is not appealing. So, we will probably use a 100% down payment.”

Personally, I will pay down my mortgage even if I can get a better return than the mortgage interest rate in a competing investment. There is a peace of mind that comes from owning real estate without a mortgage that has benefits that outweigh any small difference in financial return I may otherwise achieve.

Personally, I think the opportunity cost is huge. It is literally the ONLY reason we have not purchased a home yet.

I agree that if you were to assume that house prices were to continue to fall, your opportunity cost is certainly high and the above is moot. However, I imagine prospective buyers are making the kind of calculations I mentioned above in rent vs buy decisions. One would think that the market would find a floor somewhere in the vicinity of that region of parity. Rate increases can quickly change this equation for Irvine, though the national market has enough leeway for rates to rise and still maintain a price momentum once things turn around.

Uh-uh. Even if house prices stabilize or even appreciate a bit, the opportunity cost for us is huge. That is why I said personally.

No one seems to believe me, but when we buy a home, I doubt that I will care what home prices do. We will buy a home to live in and we will not find it less livable if home prices decline.

Opportunity cost = price housing in gold and silver.

Transfer most of PMs to real estate when DOW : Oz of Gold ratio is 1 : 1, depending on foreign sentiment regarding US sovereign default and the effects on faith in the Dollar.

I do think getting one of these 3% down Gov loans will be effectively reduced by continued debasement of US currency.

Better to have both or better to stick with PMs?

I hear ya.

I have an investment bankroll which earns enough to cover most of my rent. If I dipped into it for a down payment, I would no longer be paying rent, but I would lose much of the earning power of my liquid assets.

Even if I didn’t see the gloomy specter of shadow inventory which darkens every neighborhood I like, I see my down payment cash not as the amount which it is, but as what it earns. Only when the pile is 3x a down payment will I feel comfortable cutting out a slice of it.

Good discussion. I think that “rental parity” is a actually a pretty complicated subject. There’s a lot of wiggle room in deciding what to include, what not to, and how to calculate various factors. Personally I feel that we should examine rental parity inductively, not deductively. In other words, we should ask what has been the typical historical relationship between rental payments and monthly ownership costs during non bubble times for like properties. Is buying more expensive now relative to renting than the historical norm, even taking into account today’s low interest rates? If there is a big deviation from the historical norm, how sustainable is that?

All that being said, your typical would-be buyer when comparing rent vs own is probably doing a rough “monthly nut” comparison that leaves out down payment opportunity cost, maintainence, and principal amortization.

Excellent point, rental parity in Irvine is not a myth.

Check it out, it’s called The Groves

No FCB action here.

One would expect these much older (built in ’75) and secondary (non-premium) areas of Irvine to be priced significantly lower than $331/ft.

Mortgage rates drop for 7th straight week,

http://finance.yahoo.com/news/Fixed-mortgage-rates-drops-apf-3862609979.html

Interesting first chart there in today’s blog. Though I’m not sure I can recall what each line represents, it doesn’t look promising for sellers this year.

Seeking help from real estate sales-people here:

Must a short sale be listed as a “Short Sale”?

e.g. Redfin provides info on some listings identifying the property as a short sale. A listing just went on the market in our neighborhood for 10% below two other comps on the market for ~30 days, but it isn’t identified as a short sale.

I am not a real estate sales person, but I want to show off and see if I am correct.

If the intention is to sell short, then it must be listed as such. BUT, if the seller tells his/her agent that even though they owe more than the asking price, the seller will be paying the difference to make the loan whole, then the agent is not required to say it is a short sale, because it isn’t.

BTW, just cuz a listing is less than others does not mean it is a short sale. It may just mean that the seller is in touch with reality.

Interesting statistic that explains where the HELOC money really went:

“In 1985, 12% of personal disposable income came from savings, while just 1% came from home-equity lines, according to the Federal Reserve and Congressional Budget Office.

By 2007, 10% of personal disposable income came from housing credit: second mortgages, home-equity lines and so on. Less than 1% came from savings.”

When the Value of Housing Ruins the Home

I’m not sure these folks will be eating the bitter bread of HELOC foolishness. Obviously some of that money went into a parquet floor in their kitchen.

And you know, it’s always possible that they took that $250K in HELOC and bought Apple or Google stock with it. For their sakes I hope so, although such prescience would be unusual.

IR presents 1 HELOC abuse case per day, and I haven’t seen a lot of upgrades.

There have been some anecdotes about HELOCs being used (and lost) to start or shore up personal businesses, but again few stories about big stock buys.

(I do know 1 guy who bought his million-dollar house from speculating on YHOO in the 90s, but that wasn’t using HELOC money.)

dont you know? Everyone read the bear astute posters and found out the end was coming but they weren’t 100% sure because PR and tenmagnet kinda sound like they sort of might have maybe had some points. So they took the Heloc, bought gold with it.

If shit hit the fan, then they make out with gold. They make their gains money and squat for 24 months and then in 5 years, they can buy again for 50% off. If shit didn’t happen, then they simply sold gold and deducted interest on their Heloc.

It was a goldman sachs kind of all bets covered no way to lose smart way to play the foresight of the “been calling since 2005 crowd”.

You mean you didn’t do that? Jeez.