A combination of him prices and a depleted buyer pool push home sales to 13-year low. The recovery is expected to be sluggish.

Irvine Home Address … 195 GROVELAND Irvine, CA 92620

Resale Home Price …… $469,000

Don't you want to see it come soon,

Floating in a big white balloon

Come give her your own silver spoon

But you never looked hard enough,

It's never gonna give itself up

All you ever wanted to be,

Living in perfect symmetry,

Nothing is as down or as up

Don't you want to see it come down?

There for throwing your arms around

And say “You're not a moment too soon.”

Coldplay — Low

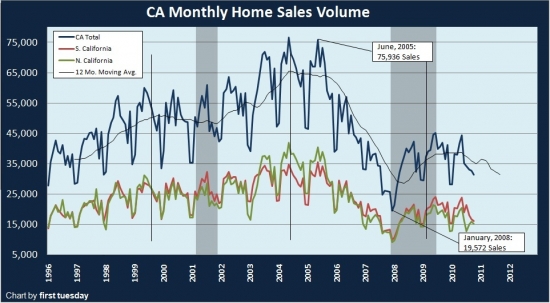

Last August I noted that Existing-Home Sales Sink to Lowest Level Ever Recorded. I'm not talking about some minor slowdown in sales or softening in prices. The current sales rates are very low no matter how it is spun.

Before the Irvine Company cheerleaders claim I am crazy, let me point out they did stop building homes for two years followed by a very slow market testing year before building a modest production run this year. I'm glad they sold them. I hope they build more. I'm delighted to see people in the building industry go back to work. As an Irvine resident, I appreciate the product the Irvine Company builds and the communities they leave behind.

Some contend I am anti-Irvine or some such rubbish because I point out the house prices are too high by historic measures. The results can be seen daily here with the cost of ownership of the individual properties that I profile. Some are at or near rental parity, but the nicer properties are still prices far above. That is the state of the market.

I report current market conditions and analyze how these may impact prices moving forward. I don't set out to be bearish, but the facts are what they are, and beyond faith in the California real estate market gods, there isn't much reason to be bullish on appreciation, and with prices still high in coastal markets, there isn't much reason to be bullish about rental income either.

Home sales hit 13-year low; slow recovery ahead

Source: Associated Press/AP Online

Publication date: January 20, 2011

By MARTIN CRUTSINGER

WASHINGTON – The number of people who bought previously owned homes last year fell to the lowest level in 13 years, and economists say it will be years before the housing market fully recovers.

High unemployment and a record number of foreclosures are deterring potential buyers who fear home prices haven't reached the bottom. Job growth is expected to pick up this year, but not enough to raise home sales to healthier levels.

“We built too many houses during the boom, and now after the crash, it will take us a long time to get back to normal,” said David Wyss, chief economist at Standard & Poor's in New York.

The National Association of Realtors reported Thursday that sales dropped 4.8 percent to 4.91 million units in 2010. That was slightly fewer than in 2008, which had been the weakest year since 1997.

Those are national statistics, but what about California?

California is a big state. Is Southern California having better sales? No, looks about the same.

Irvine is different, right?

The poor year for sales did end on a stronger note. Buyers snapped up homes at a seasonally adjusted annual rate of 5.28 million units in December, the best sales pace since May and the 12.8 percent rise from November was the biggest one-month surge in 11 years.

Gains in mortgage rates may have spurred some fence-sitters to buy homes in December before rates moved higher, analysts noted.

What analysts noted that? Some urgency analyst working for the National Association of realtors? That statement reads like NAr copy.

The increase was an encouraging sign after a dismal year for home sales, said Mark Zandi, chief economist at Moody's Analytics. But he cautioned against raising expectations for a rapid recovery in housing.

“The job market is still very weak, and unemployment is very high. Until we get more jobs, people will be reticent about buying homes,” he said.

The housing market cannot recover until the economy does. People without jobs don't buy houses… anymore. With NINJA loans dead, the housing market will not see a new influx of buyers until people get stable incomes. Realistically, even then, it is two years before a new hire qualifies for a loan.

Zandi said home prices would fall another 5 percent this year. Sales of previously occupied homes would likely exceed 5 million. That's a slight improvement from last year, he said, but it will probably take until 2013 or 2014 for sales to reach a healthy level of 6 million units a year.

Home sales will benefit from an improved hiring market. Many economists predict employers will double the number of jobs added this year compared with 2010. A reason for more optimism is a decline in the number of people applying for unemployment benefits over the past four months.

A reason for more optimism? I thought I was reading a news story, but I was really visiting my therapist. I guess internet news is the therapy of the unemployed.

Last week, applications fell to a seasonally adjusted 404,000, the Labor Department said. That followed a spike in applications in the previous week, which is typical after the holidays end and employers let temporary workers go. Even with the holiday bump and this past week's decline, the latest figures were only slightly higher than the 391,000 level reached last month – the lowest in more than two years.

Fewer than 425,000 people applying for benefits is considered a signal of modest job growth. Economists say applications must fall consistently to 375,000 or fewer to substantially reduce the unemployment rate.

Still, the unemployment rate is not expected to fall much below 9 percent this year. And the housing market cannot fully recover until the glut of foreclosed homes is cleared.

Those are the two issues overhanging the housing market. There is (1) a great deal of pent up supply in the form of foreclosures and shadow inventory, and (2) a lack of buyers available to absorb the known supply. The supply and demand imbalance will be problematic until the demand picks up and the supply is absorbed. That will take years, perhaps decades in some markets. If you look at the sales rates and inventories at the high end, the disaster in the making is clear.

Last year, a record 1 million homes were lost to foreclosures, and foreclosure tracker RealtyTrac Inc. predicts 1.2 million more will be lost this year.

Foreclosures or distressed sales such as short sales – when lenders let homeowners sell for less than they owe on their mortgages – are forcing home prices down in many markets. That has made it difficult for some potential buyers looking to upgrade, because they would have to accept less money to sell their current home.

Even historically low mortgage rates have done little to boost the sales.

Low Interest Rates Are Not Clearing the Market Inventory. Low Interest Rates Will Not Create Demand.

The average rate on a 30-year fixed mortgage rose to 4.74 percent this week, Freddie Mac said Thursday. That's up from a 40-year low of 4.17 percent in November. The average rate on the 15-year loan, a popular refinance option, slipped to 4.05 percent last week. That's nearly half a point higher than the 3.57 percent rate in November – a 20-year low.

For December, sales rose in all parts of the country, with the strongest gain a 16.7 percent increase in the West. Sales rose 13 percent in the Northeast, 10.1 percent in the South and 11 percent in the Midwest.

The median price for a home sold in December was $168,800, down 1 percent from a year ago.

Double dip.

The banking cartel members are all in agreement that pushing REO through the system right now would be a bad idea because there is not enough volume to make a difference, and the effect on pricing is devastating. However, each of them will have a different opinion as to when the market has turned and it is safe to process their REO. We will not see that phase of the cartel collapse until volume picks up enough that buyers are available for the lenders to fight for.

Peak buyer gives up after five years

How low do you wait for the market to come back? For many the real question is “how long can they sacrifice and continue making payments while they are underwater?” Perhaps it was an adjusting ARM, or perhaps he simply lost faith in appreciation of Irvine real estate, but for whatever reason, this loan owner is selling short after owning a little over five years.

He paid $643,500 back on 10/20/2005. He used a $514,550 first mortgage, a $64,300 HELOC, and a $64,550 down payment. His asking price wipes out his down payment, the HELOC and part of the first mortgage.

If this property could transact at this price, it would be at or below rental parity. In all likelihood, this property will get bid up higher as the short sale process limps along.

Irvine Home Address … 195 GROVELAND Irvine, CA 92620 ![]()

Resale Home Price … $469,000

Home Purchase Price … $643,500

Home Purchase Date …. 10/20/05

Net Gain (Loss) ………. $(202,640)

Percent Change ………. -31.5%

Annual Appreciation … -5.7%

Cost of Ownership

————————————————-

$469,000 ………. Asking Price

$16,415 ………. 3.5% Down FHA Financing

4.78% …………… Mortgage Interest Rate

$452,585 ………. 30-Year Mortgage

$94,693 ………. Income Requirement

$2,369 ………. Monthly Mortgage Payment

$406 ………. Property Tax

$307 ………. Special Taxes and Levies (Mello Roos)

$78 ………. Homeowners Insurance

$274 ………. Homeowners Association Fees

============================================

$3,435 ………. Monthly Cash Outlays

-$387 ………. Tax Savings (% of Interest and Property Tax)

-$566 ………. Equity Hidden in Payment

$30 ………. Lost Income to Down Payment (net of taxes)

$59 ………. Maintenance and Replacement Reserves

============================================

$2,570 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$4,690 ………. Furnishing and Move In @1%

$4,690 ………. Closing Costs @1%

$4,526 ………… Interest Points @1% of Loan

$16,415 ………. Down Payment

============================================

$30,321 ………. Total Cash Costs

$39,400 ………… Emergency Cash Reserves

============================================

$69,721 ………. Total Savings Needed

Property Details for 195 GROVELAND Irvine, CA 92620

——————————————————————————

Beds:: 3

Baths:: 3

Sq. Ft.:: 1950

$0,241

Lot Size:: –

Property Type:: Residential, Condominium

Style:: 3+ Levels, Contemporary

Year Built:: 2006

Community:: Woodbury

County:: Orange

MLS#:: P765561

Source:: CARETS

——————————————————————————

This gem of an end unit has a bright open floor plan with beautiful Cherrywood floors and cabinets and Tile flooring in the kitchen. The bedrooms have upgraded wall to wall carpet. Crown molding and window Shutters add their own elegance. Woodbury is one of the nations finest communities with seven pools, sport fields, tennis and basketball courts, many parks and award winning schools. Walk to the mall with both nationl chain stores and boutique shopping.

That house will probably get as low as $250K. Maybe lower. Irvine/Orange prices way off balance. Worse still nobody wants them except the Chinese.

So, you think this home’s rental value is ~$1k monthly?

These comments were frequent on IHB years ago – “This isn’t worth $___ because I wouldn’t buy it for anything more.”

I agree that there’s no way this falls to $250K. But 250/1 is still a pretty bubalicious price/rent ratio. The ratio will go a lot lower than that.

Rental value as an occupant or as a landlord? For a landlord to own this, they would want to pay not much more than 100 times monthly rent, which would give it a rental value of $2,500 a month at a purchase price of $250k. And, yes, very few Irvine properties are that cheap compared to rent. Being a landlord in Irvine is a losing proposition (unless you own an entire apartment building as opposed to just a single condo, or bought the property when Reagan was president).

Of course, this is worth a lot more than $250k. aaron is simply living on another planet.

Look at these sold comps (note how close they are-the first two appear to be in a building directly across the street):

Nearby Similar SalesMore Info

Closest homes similar to 195 GROVELAND, which sold within the past six months:

$525,000

132 CHANTILLY

Sold on Oct 28, 2010 0 miles

3 bd / 2.5 ba

1,740 Sq. Ft.

$530,000

120 CHANTILLY

Sold on Aug 27, 2010 0 miles

3 bd / 2.5 ba

1,740 Sq. Ft.

$520,000

93 CANAL

Sold on Dec 06, 2010 0.12 miles

4 bd / 2.5 ba

1,500 Sq. Ft.

$645,000

177 SANCTUARY

Sold on Jul 30, 2010 0.15 miles

4 bd / 3 ba

2,104 Sq. Ft.

$700,000

89 LAMPLIGHTER

Sold on Jan 14, 2011 0.15 miles

4 bd / 3 ba

2,104 Sq. Ft.

$700,000

161 RHAPSODY

Sold on Nov 12, 2010 0.17 miles

4 bd / 2.75 ba

2,000 Sq. Ft.

$625,000

185 SANCTUARY

Sold on Aug 24, 2010 0.17 miles

3 bd / 2.5 ba

1,580 Sq. Ft.

$700,000

187 SANCTUARY

Sold on Jan 14, 2011 0.17 miles

4 bd / 2.5 ba

1,959 Sq. Ft.

$590,000

160 VINTAGE

Sold on Nov 10, 2010 0.17 miles

3 bd / 2.5 ba

1,640 Sq. Ft.

$625,000

189 RHAPSODY

Sold on Jan 21, 2011 0.19 miles

3 bd / 2.5 ba

1,640 Sq. Ft.

Range: $520,000 – $700,000

Average: $344/Sq. Ft.

This home at $344/Sq. Ft.: $670,020

Note that the two in the building across the street are 210 sq ft smaller than this place yet sold above the current asking price (more that double what aaron thinks it’s worth).

Which begs the question..

Why would anyone in their right mind pay $500K for a property they could rent for $2500/month.

This is a wild guess:

It could be due to the fact that the monthly cost of ownership with a $400K mortgage is about the same as renting.

Again, a total wild guess. Some people may like the fact that the mortgage payments of around $2000 a month are fixed and the interest is deductible. I’m going out on a limb here though, and pondering other wild reasons why someone would consider it.

The $400/month property tax is sort of fixed also (goes up 2% per year)…

Maintenace costs are never fixed… Hey Mr plumber, I hear you need another boat payment… come on over…

HOA fees… Hey guys, sorry we didn’t access enough to cover some needed repairs, how’s about a $2000 special assessment

Sorry dude, there’s a lot more to owning a home then just paying a mortgage. In my experience, $2500 rent vs $500K for property… RENT

There are a ton of reasons to BUY rather than RENT. Children would be the top on that list. Most parents want their children to have a great education, in Irvine they get that.

Buying with the SUBSIDIZED mortgage deduction, makes it very close to renting, gives you long term stability for the children to grow up in the same neighborhood, and gasp…believe it or not, eventually, you WILL pay off the mortgage if you do not use it as an ATM machine.

And Alan, when you own your own home you either LEARN to fix/build things yourself, or you pay dearly. I learned quite a bit, how to do basic electrical, plumbing (including sweating copper), masonry, and a host of other skills that you will never ever learn renting. Some people would prefer to never learn those skills, but then again, some people love renting, not owning.

1. Are you saying renters’ children don’t get a good education?

2. Having happy parents that don’t stress over a mortgage loan may actually result in more stability for the children.

3. What if instead of fixing the next broken thing in the house, I prefer to spending time playing with my children in my rented house?

aaron forgot to mention in his post that he’s also looking to purchase Apple stock for $40 a share.

@aaron:

“That house will probably get as low as $250k. Maybe lower.”

Care to wager on that? The last time a 3b/3ba ~2000sft home in Irvine went for less than $300k was in the 90s.

While I hope that would happen (because that would mean 5/3s are are less than $400k) I am pretty sure it is close to impossible.

That would be an ELE.

Based on current incomes, rents, and interest rates, $450,000 would be a good price. It would take 9% interest rates without rising incomes to see $250K on this property.

I don’t even think 9% interest rates will do it even if income doesn’t rise.

Even in the 90s bubble, prices in Irvine didn’t go too far below their base prices and there were 9% rates then too.

I don’t even think 9% interest rates will do it even if income doesn’t rise.

Of course you don’t think that.

Even in the 90s bubble, prices in Irvine didn’t go too far below their base prices and there were 9% rates then too.

I can only hope (and pray) that we get a chance to see if your correct in the near future.

JMO ~ 9% mortgages at today’s prices would kill affordability in Irvine.

That assumes an FHA loan.

Meanwhile in the real world the cash down payment on this home is almost $100K, current price is then below rental parity.

Exactly PR, heavy cash down payments are the norm rather than the exception.

It’s an interesting definition of “rental parity” that ignores the oportunity cost of $100K down payment.

You are wrong, opportunity cost are included.

But not all of us are investing in cutting edge big money investments in the Salsa industry. Your oppotunity cost are understandably exorbitant.

There exist ways of defining “rental parity” such that this property meets the definition at the current asking price. As such, I conceed that someone can call this price “rental parity” without necessarily being disingenuous. I’d contend that such definitions of rental parity aren’t normal or sustainable.

And I don’t know how things are on planet Reality, but on planet Earth making fun of an anonymous internet poster’s handle doesn’t constitute a very good argument.

But, if that is the only argument you got ….

yikes…! IR, you just hit the nail on the head. I believe we are more likely to have 9+% rates a decade from now than 6 or 7. You could literally own this or any OC RE for a decade only to loose money when you have to sell to someone buying with 9% money!

We are likely in for a very long slow grind lower as long as we have a stagnant economy with high unemployment and rising commodity costs.

BTW, all of you believing in the tax deductions etc. The feds are likely to eliminate this for any debt above $500K. The debt and deficit commision for Obama just said eliminate it completely…..

My .02

Aaron,

Stay in the inland empire.

Thank you,

All of Orange County.

Interesting graph of OC home prices at

http://lansner.ocregister.com/2011/01/26/price-cuts-grow-by-sellers-of-high-end-homes/96988/

Yeah, asking prices are dropping. One hopes this tracks some kind of downward trend in final sales price as well, but I wonder what the exact correlation is.

For all I know this just means 75th percentile listers are marking things more realistically without a big drop in the actual sales price (e.g. homes destined to be sold at $600K are now finally being listed at just above that, instead of $800K). But I hope that it is an indication that sales prices are also continuing their downward dribble.

Yeah, aaron forgot to mention in his post that wants to buy Apple stock at $40 a share as well.

aaron forgot to mention in his post that he wants to buy Apple stock at $40 a share as well.

sorry, I got trigger happy

there’s something going on here nobody is talking about.

yeah, jobs matter. as do prices. and even rates.

but how about history and learning something after touching a hot stove.

(i think ) there’s a whole slew of pretty smart (once) potential buyers who having witnessed the post bubble carnage in the housing market will NEVER buy (my hand is raised). the recent level of devastation (i.e., prices) is pretty new territory, isn’t it? ; especially in “new” sunny markets like Fla., Phoenix and Vegas once thought immune because of, well, i forget. oh yeah, the sun.

houses turned out to be nooses. and having escaped the hangman once, who wants to give him another shot.

ps u can RENT houses in nice neighborhoods, NOT have to pay property taxes and send ur kids to the (potentially) good schools there right?

Definitely seems to be the bandwagon of late, rent rent rent, and who’s to disagree? We have no idea if home prices are even near their actual valuation. I don’t think we’ve cleared ourselves of the bubble yet but we’ll see how well 2011 stabilizes and where our economy goes this next year.. It’s the American dream to own your own property.

I think I’m with Aaron on this one. And here’s why:

1. the median income for a family in Irvine is 111,455

2. 4 times earnings (the Irvine premium) is only $445,820.

3. I don’t believe this condo is equivalent to or worth $450,000 because it’s not a median home.

For this area, I believe $150 a square foot is more reasonable valuation. That puts this home at about $292,500.

4. That is, it’s a small condo.

At $275-3K