Fannie May posted an $8.7 billion loss in the first quarter bringing total GSE losses to $164.4 billion so far. More losses are coming.

Irvine Home Address … 1 SOLANA #22 Irvine, CA 92612

Resale Home Price …… $550,000

Just look at all those hungry mouths we have to feed

Take a look at all the suffering we breed

So many lonely faces scattered all around

Searching for what they need

Is this the world we created?

we made it on our own

Is this the world we devastated

Right to the bone?

Queen — Is This the World We Created?

When the housing bubble became apparent to policy makers in Washington, they realized there was only one way to prevent a catastrophic collapse in house prices: they had to take over housing finance. To that end they took the GSEs into conservatorship, and the federal reserve began buying mortgage-backed securities at prices the free market was unwilling to pay. With both the delivery mechanism under direct government control and the ability to print money with through the federal reserve, aggregate loan balances were maintained al levels much higher than otherwise would have occurred. This is the world of mortgage finance we created. The taxpayer is paying the bills.

Today, we are gradually returning to a free market in housing finance, but the government still dominates with well over 90% market share. The federal reserve has stopped buying mortgage-backed securities with printed money, and the government is scaling back it's loan limits. However, when the government took over the GSEs, it assumed the liability for all their bad loans; past, present, and future. The bills keep mounting.

Fannie Mae 1Q loss $8.7 billion

by JON PRIOR — Friday, May 6th, 2011, 3:14 pm

Fannie Mae reported net loss of $8.7 billion in the first quarter, including a $2.2 billion dividend payment to the Treasury Department. The loss narrowed from $13 billion one year ago.

Fannie said still falling home prices drove losses during the quarter. The government-sponsored enterprise estimated home prices fell 1.8% during the quarter, even though some regions experienced gains.

The mortgage giant's regulator the Federal Housing Finance Agency requested $8.5 billion from the Treasury to eliminate Fannie's net worth deficit. Fannie now owes the Treasury $99.7 billion and so far paid $12.4 billion in dividends.

Its sibling company, Freddie Mac actually reported a profit in the first quarter and did not request funds. Together both Fannie and Freddie have pulled a total of $164.4 billion from the Treasury since entering conservatorship in 2008.

Despite the continued losses, Fannie Mae showed how vital its operations are to funding the housing market. It remained the largest issuer of mortgage-backed securities in the first quarter, purchasing or guaranteeing roughly $189 billion in loans. The company's market share dipped to 48.6% in the quarter from 49% in the previous period.

But Fannie said if the market shifts away from refinancing as is likely to occur as mortgage rates rise, market share will dip further.

A declining market share for the GSEs is exactly what we need. Eventually, their market share needs to fall to zero and the entities need to be eliminated. Realistically, that process won't begin in earnest until the housing market achieves a durable bottom, probably in 2012 or 2013.

While business could be declining, legacy issues are too. The serious delinquency rate on Fannie Mae loans dropped to 4.27% in the first quarter from 5.47% one year ago and 4.48% in the previous period. The company said modifications and other workouts, combined with foreclosures when other alternatives are exhausted, outnumbered new delinquent loans hitting its books.

That is a good sign. We can't bring down REO inventories until we stop adding to them. Of course, the vast majority of loan modifications will fail, and those properties will once again go delinquent, but by delaying the inevitable, it allows the GSEs to reverse the tide of delinquencies, but it also ensures the liquidation process will drag on far longer than anyone anticipates.

Fannie Mae CEO Michael Williams said “credit-related expenses” will remain high in 2011 as it remains exposed to falling home prices.

“As we move forward, we are building a strong new book of business that now accounts for 45% of the company’s overall single-family guaranty book of business,” Williams said. “We continue to be the leading provider of liquidity for single-family mortgages and affordable multifamily rental housing while we remain focused on our responsibility to find solutions for distressed homeowners and their families.”

The only solutions the GSEs are providing is to give free houses to delinquent mortgage squatters on the taxpayer's dime.

In other GSE news,,,

Freddie Mac sells record number of REO in 1Q

by JON PRIOR — Friday, May 6th, 2011, 5:36 pm

Freddie Mac sold roughly 31,000 previously foreclosed and repossessed homes in the first quarter, a new record for the company as both government-sponsored enterprises shed inventory from the end of last year.

Combined, both Fannie Mae and Freddie hold 218,000 REO properties as of the end of the first quarter, down from roughly 234,000 at the end of 2010, according to their filings.

In the first quarter of 2011, Freddie holds roughly 65,000, compared to its larger sibling Fannie, which holds 153,000 REO in its inventory.

While both GSEs made progress in cutting down this portion of the nation's inventory of foreclosed homes, which continues to drag down home prices, inventory has elevated since one year ago.

Both Fannie and Freddie held 163,000 properties in the first quarter of 2010, almost what Fannie holds currently by itself.

Repossessions at Freddie increased by nearly 1,000 in the first quarter, and the holding period for these homes averaged 191 days before being resold. This varies significantly from state to state, especially as servicers restart foreclosure processes in different areas of the country. Servicers paused the process late last year to correct procedural problems.

The GSEs are delaying processing many of their delinquent loans because they already have too many REOs, and they are delaying releasing their REOs because if they don't they will pummel house prices.

“We expect the pace of our REO acquisitions to increase in the remainder of 2011, in part due to the resumption of foreclosure activity by servicers, as well as the transition of many seriously delinquent loans to REO,” Freddie said in its financial supplement.

Fannie, Freddie align servicing guidelines for delinquent mortgages

by JON PRIOR — Thursday, April 28th, 2011, 1:31 pm

The Federal Housing Finance Agency directed Fannie Mae and Freddie Mac Thursday to align their guidelines for servicing delinquent mortgages.

Previously, the government-sponsored enterprises maintained different requirements for how their mortgage servicers would treat these loans. But the FHFA forced an alignment to push servicers into engaging the borrower as soon as they become delinquent. The foreclosure process cannot begin if the borrower and servicer are working toward solving the delinquency in a good-faith effort, effectively prohibiting the practice of “dual tracking.”

The state of California blocked legislation that would have prohibited dual track foreclosure. The GSEs are merely adding time to the foreclosure process and enabling delinquent mortgage squatters to further game the system.

Under the new requirements, servicers must engage in a single track for considering foreclosure alternatives up to the 120th day of delinquency, according to the FHFA. Servicers must also perform a formal review of the case to confirm the borrower was considered before starting foreclosure. Even then, servicers are required to continue work with the homeowner on other alternatives.

Not only procedures, but incentives were aligned. Servicers for both GSEs will be rewarded and penalized the same under the new guidelines.

“FHFA's directive to align Enterprise policies for servicing delinquent mortgages should result in earlier servicer engagement to identify the best solution available for homeowners, given their individual circumstances,” said FHFA Acting Director Edward DeMarco.

The FHFA said the updated framework will expedite borrower outreach, align modification terms and establish “a consistent schedule of performance-based incentive payments and penalties.”

Now all the bad processes that encourage strategic default will be uniform. I don't see that as an improvement.

Fannie Mae CEO Michael Williams said the alignment is a major step toward an improved servicer process.

“This initiative will direct servicers to reach families earlier, communicate more frequently and clearly, and provide relief,” Williams said. “Fannie Mae fully supports this Initiative, and we remain committed to stabilizing communities and building a stronger foundation for housing.”

Freddie Mac CEO Ed Haldeman said the FHFA action will simplify the process for delinquent borrowers.

“Alignment of key servicing practices between our two companies will help servicers achieve these goals by enabling them to streamline their operations and more effectively target resources to distressed borrowers,” Haldeman said in a statement. “For example, it will simplify the process for seeking help by giving borrowers one application to fill out and servicers one application to review for all Freddie Mac loan modifications and foreclosure alternatives.”

The GSEs should be dismantled. They can no longer successfully function as a quasi governmental agency. Lenders would prefer to keep the GSEs around so lenders can continue with an origination model with no risk, but with the US taxpayer being on the hook for the foolishness of bankers everywhere, I doubt that model will survive much past the market bottom.

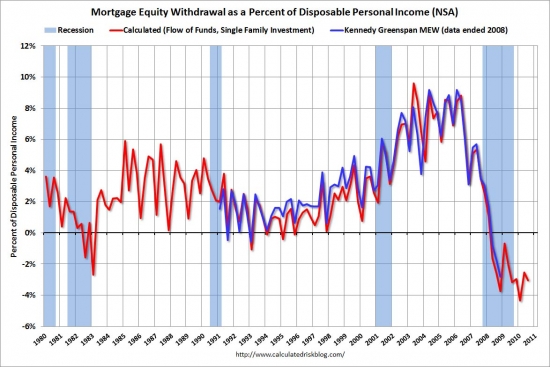

They went Ponzi too

Day after day, I see more loan owners and Ponzis than responsible owners who paid down their mortgage. Eventually, I will run out of these profiles because we haven't created any new ones in the last 4 years. With the credit crunch in August 2007, the mortgage equity withdrawal spigot was abruptly turned off.

Contrary to popular belief, the free money of mortgage equity withdrawal will not be coming back soon. In a rising interest rate environment, money is no longer free. Adding to debt adds to monthly bills. Only the steadily falling interest rates of the Greenspan era allowed refinancing of larger and larger amounts with the same payments. It also permitted borrowers to Ponzi themselves into unsustainable lifestyles which they now have to abandon.

Unfortunately, the general public knows none of this. Most buyers who overpaid for Orange County real estate over the last 4 years did so because they fully expect house prices to go up and lenders to resume handing out free money. Despite the crash, most wouldbe buyers consider California real estate to be a bottomless pit of gold.

Shevy and I have been advising people to look at a house as an expense not an investment. A mortgage is to be paid off, not added to or otherwise “managed.” I harp on this day after day because I keep seeing people who lost their homes because they fell victim to the kool aid thinking in California. These people all had a choice, and they made the wrong one — often multiple times with varying degrees of stupidity. Nothing can be done for these loan owners, but we can all learn something from their mistakes.

- The owner's of today's featured property paid $377,000 on 12/14/2001. My records are incomplete, but it looks as if they used a $301,600 first mortgage (80% LTV), a $75,000 second mortgage, and a $400 down payment.

These people were very regular about their visits to the housing ATM. In April for four consecutive years, they extracted a little cash — well, actually a lot of cash. Many people become accustomed to an April “windfall” when they get their tax refund. The forced savings of tax withholdings is the only savings many people have. These borrowers must have felt their tax returns were not big enough, so they borrowed themselves into oblivion.

- On 4/16/2003 they refinanced with a $436,500 first mortgage.

- On 4/29/2004 they obtained a $420,000 first mortgage and a $78,750 stand-alone second.

- On 4/7/2005 they opened a $130,525 HELOC.

- On 4/10/2006 they obtained a stand-alone second for $254,260.

- Total property debt is $674,260.

- Total mortgage equity withdrawal is $297,660. Not bad for a $400 investment.

Given that such a windfall has proven possible, it's not surprising that California real estate is so highly prized.

Irvine House Address … 1 SOLANA #22 Irvine, CA 92612 ![]()

Resale House Price …… $550,000

House Purchase Price … $377,000

House Purchase Date …. 12/14/2001

Net Gain (Loss) ………. $140,000

Percent Change ………. 37.1%

Annual Appreciation … 4.0%

Cost of House Ownership

————————————————-

$550,000 ………. Asking Price

$110,000 ………. 20% Down Conventional

4.62% …………… Mortgage Interest Rate

$440,000 ………. 30-Year Mortgage

$96,896 ………. Income Requirement

$2,261 ………. Monthly Mortgage Payment

$477 ………. Property Tax (@1.04%)

$0 ………. Special Taxes and Levies (Mello Roos)

$115 ………. Homeowners Insurance (@ 0.25%)

$0 ………. Private Mortgage Insurance

$384 ………. Homeowners Association Fees

============================================.jpg)

$3,236 ………. Monthly Cash Outlays

-$380 ………. Tax Savings (% of Interest and Property Tax)

-$567 ………. Equity Hidden in Payment (Amortization)

$191 ………. Lost Income to Down Payment (net of taxes)

$89 ………. Maintenance and Replacement Reserves

============================================

$2,569 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$5,500 ………. Furnishing and Move In @1%

$5,500 ………. Closing Costs @1%

$4,400 ………… Interest Points @1% of Loan

$110,000 ………. Down Payment

============================================

$125,400 ………. Total Cash Costs

$39,300 ………… Emergency Cash Reserves

============================================

$164,700 ………. Total Savings Needed

Property Details for 1 SOLANA #22 Irvine, CA 92612

——————————————————————————

Beds: 3

Baths: 2

Sq. Ft.: 2000

$275/SF

Property Type: Residential, Condominium

Style: Two Level

View: Park/Green Belt

Year Built: 1975

Community: Rancho San Joaquin

County: Orange

MLS#: S657444

Source: SoCalMLS

Status: Active

——————————————————————————

A superb opportunity to acquire this stunning and spacious Two-Story Townhome with Just One Common Wall for a great price. This home boasts an elegant front yard leading to the tastefully upgraded interior. The gourmet kitchen with granite countertops and matching appliances is a delight for every Chef. The crownmolding complements the high quality tile floors and the newer carpet throughout this bright and spacious home. Schedule a showing today to appreciate the charm of this welcoming home in a very desirable neighborhood.

Today we are gradually returning to a free market

I don’t see any evidence that supports this conclusion. There is some chirping about putting these bloodsuckers out of business at some point in the future but I see nothing that suggests that the Government has any intention of extricating itself from housing.

The camel is not just going to leave the tent. There is way too much money to be made by those who carry the most political influence. Too Big To Fail is still official Government policy – that is all you need to know in order to realize that a free market in housing is a pipe dream in this life.

No, what we are going to see is a “transition” to some new scheme that the bankers come up with to “help” people get taxpayer guaranteed lines of credit. Likely, it is going to have a free-market sleight-of-hand to it but we all know whatever they come up with will carry another “implicit” guarantee from the Federal Government only the next time “things will be different”.

I hope you are wrong.

You are likely correct.

There never was a free market in America and there never will be a free market. The goal has always been the same in America’s version of capitalism: Inflation disguised as growth with an economic roller coaster that impacts the upper and lower half differently. The game continues to work exceptionally well as our greatest problems are things like: too many large empty houses, to many calories in our diets, too expensive to live in premium areas with the best schools. We must find a way to overcome these exceptional tragedies.

Nice list of problems, PR. Don’t forget things like:

1 in 7 on Food Stamps

Unemployment Rises 9% Despite Job Growth

Stagnant Wages

Wealth Inequality

But none of that matters because we have plenty of food. All problems cease to exist on Planet Realtor when society has an abundance of food. Don’t start complaining to PR until the food rioting begins.

I think you are missing the point. The REALITY is, there will be no riots or major change unless the FOOD is cut off. Take a good long look around your country….I’m assuming you have David by your posts. The scene is one of imbalance caused by plutocracy. The people eat up all the B.S. from either party, while voting against their own best interests (socialized medicine, making corporate giants pay their fair share of taxes, protesting wars for the few individuals to get rich, etc etc).

PR is right, whatever the machine is doing is working, but it’s not working as well as it once did, so wars and evil men are created to keep the focus off the hamster wheel of slavery.

The big boys pulled the wool over americans eyes, transferred all the hate and blame to the “homeowners”, and left with a boatload of cash. Now, nothing has changed, and the crooks will be back to pump another bubble, cash out, then run. I see the healthcare industry next.

Either you’ve accidentally contradicted yourself or you’re an idiot. I’m going to go with both. You’re right that the economic roller coaster impacts the upper and lower half differently; your list of our greatest problems couldn’t be stupider. Have you ever stepped outside of Irvine? Are you aware that upwards of 10% of the nation’s residents are unemployed, and a much larger number are underemployed with either no or insufficient health insurance?

Get your head out of the Irvine desert sand (or your ass, which is the more likely location).

“you’re an idiot”

Careful. We don’t call names here.

Yeah, you’re barking up the wrong tree. Or squawking up the wrong tree. Though, since only birds really squawk, and they are usually in trees, rather than at the bases of them, then you’re squawking down the wrong tree.

Cuz that tree lives in AZ. And is a cactus. And appears to be cognizant and/or have directly addressed the problems which apparently are weighing down your soul with sorrow. Also the tree-squawk in general was a sudden, massive, unnecessary (as this response is) extension of an already tangential tangent. Chillax mon ami.

Your mixed up posts, Frak. You’re an idiot.

Be nice!

Ok.

Total mortgage equity withdrawal is $297,660. Not bad for a $400 investment

ROI = over 700x with no liability, but they might not be off the hook for the seconds.

Without skin in the game from the loan originators, packagers and personal liability, the game will be renamed, repackaged, respun and started again once the dust settles. Now it FHA loans at 3.5% down with govt holding all the liability or should I say taxpayers. The banks are still getting their origination fee, servicing fee, and foreclourse fee from the transactions. Not bad with no skin in the game.

Lower house price will hurt in the short run, but will be healthy for Main Street.

Any comments about the latest Zillion report on 128 out of 130 housing markets having steep Y2Y declines?

Agreed. FHA is a great example. Not hearing a whole lot of people calling to FHA to be dismantled. It seems almost certain that they will be picking up a significant amount of slack in the future. In other words, FHA might as well be renamed to the ‘Ministry of First Time House Buyers’.

Look at what they are doing – allowing people to buy houses with 3.5% (nothing) down. How long until 3.5% is too burdensome for the common man? Is the plan to gradualy work our way toward 0% over a couple decades? Why is 3.5% so magical? Why not 3%? Or 2.5%? Certainly it shall be presented at some point that 3% or 2.5% are no more risky than 3.5%.

In the future – want to buy a house? Nah, don’t save a dime. Just head on down to the Ministry of First Time House Buyers (MFTHB) with your hat-in-hand and be sure to bring a DNA sample and fingerprint card.

With the prior tax credits, some people even got money out of the deal!

There was talk about lowering the FHA down requirement. Usually it’s talk, opposition, talk, talk and passing the law or regulation in the dead of night.

…“things will be different.” Sounds like the battered wife or husband montra.

Yes, totally; people using the 8K tax credit AS their down payment because they could not scrounge up a penny.

I am actually surprised that the 8K tax credit has not been extended again. I figured it was going to become one of those new perma entitlements alongside the mortgage interest deduction. Probably because the number of existing house debtors would then demand to be grandfathered in and demand their own piece of the cheese.

Maybe something similar will show up again when the Ministry of First Time House Buyers is implemented.

I’m fearful of the default rates on the tsunami of FHA loans made since 2007, but at least those loans had real PMI backstops unlike the zero-down, liar loans. Recall too that people have to pay some PMI upfront when doing an FHA loan. So from the taxpayers’ POV, there is at least some upfront cost recovery.

Most of these loans will hold up (unless job losses worsen which is a possibility), since many of these FHA borrowers were the more responsible types. But clearly the risk has moved from irresponsible private lenders to slightly more responsible GSE/taxpayer programs.

At least the size of that risk has been reduced (the price declines mean that many of the loans are at lower levels than the outrageous 05-07 days) including the absence of any housing ATM outrages.

Really, the pols and the Fed/Treasury had no choice but to go this route. If you were in there shoes, you would have done much the same. Mass economic calamity serves no one. Which is why a guy like Bill McBride at CR, whose anger is evident, takes such a moderate tone. The time to fix this problem was to avoid it altogether. Humpty-Dumpty can’t be put back together again and all we can do is try and make an egg-shell littered omelette out of what remains so it does not go completely to waste.

“Really, the pols and the Fed/Treasury had no choice but to go this route. If you were in there shoes, you would have done much the same.”

A sad truth.

The only problem with a more moderate tone is that people forget how outrageous the behavior was, and if enough times goes by, it will be repeated, and nobody will raise a fuss. Only an uncomfortable reminder of just how wrong lenders were can work to create change.

I don’t buy the argument that mass economic calamity was averted by keeping the TBTF banks in business.

I am with AZD on this one. Giving a fix to an addict averts nothing, only prolongs the agony, and adds difficulty and pain to the cure.

“Total mortgage equity withdrawal is $297,660. Not bad for a $400 investment

ROI = over 700x with no liability, but they might not be off the hook for the seconds.”

Actually, I’m still hopeful that isn’t true. The refi’s are recourse, and I still hope that the banks are selling them to debt collectors.

The only way that this whole tragedy doesn’t repeat itself in the next 10 years is if there is a whole class of people who are harassed for their lifetimes to make good on their bad debts. Then the lesson will endure in society for 50 years, maybe…

Is there even a lesson in any of this?

Ask an F’d House Debtor and they are mad the bank.

Ask the bank and they are mad at the F’d house debtor.

Ask a renter and they are mad at everybody including the Government.

Ask the Government and they have no comment.

Ask the Fed and they say there are no problems.

Moral Hazard is a hell of a drug.

I ain’t mad at anybody and just what to figure how to make money off other’s foolishness.

Which probably is the lesson in all of this. Be ready to buy up as much property as you can get your hands on when the Government blows the next bubble and sell quick.

It’s good to see you made some progress. Now here is the real trick to it, when you and everyone else starts screaming bubble wait 2 more years and sell closer to the peak.

Give me 100% financing with cash back and I’m game.

There were 2 segments about real estate in the local Bay Area news.

1) Interview with a female realtor. When asked about declining home prices, she blamed “fickle buyers.”

2) Another segment on rentals said San Jose and SF are red-hot again like 2000, and rent now before you’re priced out forever. 🙂