That housing markets in the most beaten down areas are now experiencing widespread despair. Prices are so low that existing owners have little hope of recovery.

Irvine Home Address … 263 HUNTINGTON Irvine, CA 92620

Resale Home Price …… $300,000

They used to tell me

I was building a dream.

And so I followed the mob

I was always there

Right on the job.

They used to tell me

I was building a dream

With peace and glory ahead.

Why should I be standing in line

Just waiting for bread?

Brother, can you spare a dime?

Al Jolson — Brother, Can You Spare a Dime?

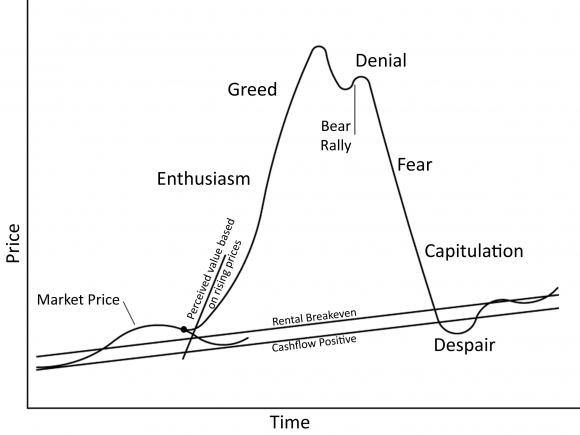

Financial markets all exhibit the same psychological stages during a bout of irrational exuberance. A precipitating factor such as lowered interest rates or financial innovation folly, causes prices to rise when valuations suggest they should fall. This changes the market's perception of value, and buyers eagerly buy and drive prices higher. Greed and delusion set in as prices are propelled ever higher.

Finally, the bubble bursts, and the market enters a phase of denial. Irvine and Orange County have been stuck in this phase due to the bear rally. Finally, fear begins to set in, and sellers reduce their prices in order to get out while they still can. This is currently happening at the high end in California. The market is slipping into fear, but it is far from capitulation or despair.

The subprime real estate markets were crushed first because their loans reset before the alt-a and prime markets. The subprime markets are much farther along the process. Las Vegas capitulated in late 2009, and most other subprime markets have given up since then. Despair now rules these markets. Is that an opportunity?

Homeowners face 'new normal' in housing bust

By Julie Schmit, USA TODAY

MERCED, Calif. — Life has changed in ways big and small in this central California county, which is still trapped in the wreckage of a housing boom that went bust five years ago.

The median home price, $116,000, is down 68% from its peak in 2006. Three of five homeowners with a mortgage here owe more on their loans than their houses are worth, compared with about one in five nationally.

Socked by a sharp loss of property and sales tax revenue, Merced County and its cities have slashed budgets, workers and services. The grass is being mowed less often in city parks. A senior center is open fewer hours.

Families have adjusted, too. Forget dreams of making big bucks on California real estate. Many here now count the years — guessing, really — until they'll no longer owe more on their homes than they're worth.

“We're in survival mode, waiting for recovery,” says Stephen Hammond, 42, pastor at Bethel Community Church in Los Banos, a Merced County town of 35,000 amid cotton and tomato fields.

More cuts are possible because of looming budget deficits, Merced government officials say. Dozens of other communities nationwide may face the same tough choices in the wake of huge drops in home values, which often lead to less property tax revenue. In Merced, the impacts have hit hard, and they hint at what may be to come for others.

For Merced County government, property taxes are the No. 1 source of general fund revenue, says Scott De Moss, deputy county executive officer. Property tax revenue has dropped 25% during the past three years. Almost 15% of the county's workforce has been slashed. Social and mental health service positions took the biggest hits, officials say.

In the city of Merced, sales tax revenue is down 24% and property tax collections, about 34%, from 2007 levels, city officials say. That's forced cuts in the police and fire departments. Police might not show up anymore to take fender bender reports and firetrucks may no longer always roll on the same calls as ambulances, says Merced City Manager John Bramble. The city's 80,000 trees now get pruned once every three years, instead of every two. The senior center is open 28, not 40, hours a week. Asphalt patches, not new concrete, are being used to repair sidewalks.

“People are used to a higher level of service,” says Bill Spriggs, who serves as mayor for the city of 80,600. “But this is the new normal.“

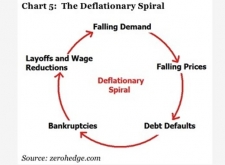

The old normal was an unsustainable Ponzi scheme. The new normal is an endless series of financial bailouts to prevent losses from the collapse of the unsustainable Ponzi schemes that come about because investors believe the federal reserve will bail them out. A self-reinforcing vicious circle.

Now the Ponzi scheme is collapsing into a deflationary spiral. The cuts in city services will cause further declines in local spending which will hurt a fragile economy.

In Los Banos, the grass is now cut in city parks every 15 days. It used to be cut weekly. Vacant houses dot nearly every neighborhood. New roads end in cul-de-sacs surrounded by vacant lots. A weather-beaten billboard announces a 35,000-square-foot retail center that is “coming soon” but never has.

“This was, right here, all going to be industry,” says Tommy Jones, Los Banos' former mayor, as he points to a goat pasture.

Nationwide, local governments typically get more than half of their revenue from local sources, the largest of which is property taxes, says economics professor John Anderson at the University of Nebraska. Because property tax collections can lag behind market values by 18 months to several years, they continued to rise for U.S. cities through 2009 — despite housing price declines in most areas. But city property tax collections fell 2% last year as reduced assessments started to kick in, according to survey data collected by the National League of Cities. More drops are expected this year and next as the decline continues.

The Merced city and county governments have softened the blow to services by eating through millions in financial reserves. But budget deficits are still the norm. This summer, Merced city plans to ask residents to approve a half-cent sales tax increase to cover a $5.2 million budget shortfall.

If the new tax doesn't pass, Bramble says, “The quality of city services will be severely changed.”

This tax revenue is not coming back because house prices are not coming back. Local governments are going to have to adjust to budgets based on current property values, not some fantasy of what properties were selling for in 2006. California's Ponzi Scheme economy has collapsed. Municipalities like Merced that are spending their financial reserves are being foolish and irresponsible, and it will hurt them in the end.

|

Deeply underwater

|

|||

|

|

|||

| At least half of homeowners with a mortgage owe more than their homes are worth in 17 of 386 U.S. counties. Counties with the highest percentage of mortgages under water as of Sept. 30. | |||

|

|

|||

| Rank | County | State |

Mortgages under water

|

|

|

|||

| 1 | Clark | Nev. |

71.1%

|

|

|

|||

| 2 | Osceola | Fla. |

66.5%

|

|

|

|||

| 3 | Merced | Calif. |

63.1%

|

|

|

|||

| 4 | St Lucie | Fla. |

62.4%

|

|

|

|||

| 5 | San Joaquin | Calif. |

59.6%

|

|

|

|||

| 6 | Stanislaus | Calif. |

57.5%

|

|

|

|||

| 7 | Clayton | Ga. |

56.1%

|

|

|

|||

| 8 | Orange | Fla. |

56.1%

|

|

|

|||

| 9 | Solano | Calif. |

55.6%

|

|

|

|||

| 10 | Maricopa | Ariz. |

54.4%

|

|

|

|||

| 11 | Washoe | Nev. |

53.3%

|

|

|

|||

| 12 | Pinal | Ariz. |

52.6%

|

|

|

|||

| 13 | Flagler | Fla. |

52.5%

|

|

|

|||

| 14 | Pasco | Fla. |

51.5%

|

|

|

|||

| 15 | Riverside | Calif. |

50.5%

|

|

|

|||

| 16 | Kern | Calif. |

50.2%

|

|

|

|||

| 17 | Broward | Fla. |

50.1%

|

|

|

|||

| 18 | Lee | Fla. |

49.5%

|

|

|

|||

| 19 | Canyon | Idaho |

49.0%

|

|

|

|||

| 20 | Henry | Ga. |

48.8%

|

|

|

|||

| 21 | Polk | Fla. |

48.5%

|

|

|

|||

| 22 | Hillsborough | Fla. |

48.5%

|

|

|

|||

| 23 | Dade | Fla. |

48.2%

|

|

|

|||

| 24 | Sacramento | Calif. |

47.9%

|

|

|

|||

| 25 | Paulding | Ga. |

47.5%

|

|

|

|||

| 26 | Prince William | Va. |

47.4%

|

|

|

|||

| 27 | San Bernardino | Calif. |

46.9%

|

|

|

|||

| 28 | Brevard | Fla. |

46.9%

|

|

|

|||

| 29 | Wayne | Mich. |

46.6%

|

|

|

|||

| 30 | Hernando | Fla. |

46.5%

|

|

|

|||

| Source: CoreLogic | |||

Underwater, with few options

The double whammy of the recession and the real estate crash has forced changes in how consumers spend, plan for their futures and view their neighbors. Businesses also have suffered, because homeowners have less equity in their homes or none at all. Overlaying everything is a local economy in which one of five workers is jobless, in part because of the collapse of the area's once-fast-growing home construction industry.

The “last good year” was 2008, says Greg Parle, owner of the Branding Iron Restaurant in Merced. Business is off at least 20% since then, he says. He's adding lower-priced items to the menu.

The region's ability to foster such small businesses will suffer because of so much lost home equity. Almost one-quarter of small-business owners borrow against their homes or use them as collateral to fuel businesses, according to a 2009 Gallup survey of small-business owners. That'll likely be less now in Merced and other places with so many underwater homeowners. Start-ups will feel the greatest impact, says Mark Schweitzer, director of research for the Federal Reserve Bank of Cleveland.

Loreina Childress, 39, a county environmental health worker, has felt the impact of the new normal at home and work.

The previous work of 26 in her department is now done by 21. At home, a lot remains vacant, and there are more renters in her neighborhood than before the real estate bust.

Childress bought her Merced County home in 2006, when the market was still hot. She owes $241,000 on the 1,500-square-foot home that might sell for $140,000.

These people are so screwed. Typically, it takes 15 to 20 years for prices to double. People who have houses worth half their mortgage will spend the rest of their working lives paying a bloated debt and waiting for prices to come back.

Her husband, Gary, 38, switched careers a year ago, from forklift driver to emergency medical technician. He can't find full-time work. That's placed new stress on the family's finances, along with the reality of being so far underwater on the house.

Loreina now pours milk in her coffee, not cream. She eats TV dinners at her desk for lunch, rather than fresh sandwiches at a deli. She can recite, down to the penny, the cost of South Beach Diet bars at three retailers. Plans to landscape the yard have been scrapped.

Gary might have more luck pursuing work in other states. That would mean selling the house at a big loss or doing what the couple say they won't do: Give the house back to the bank and walk away.

“We made an agreement,” Loreina says. “We can't go anywhere until we can break even on the house.“

I hope they don't have anywhere to go any time soon. They are trapped in their debtors prison. I hope it is a gilded cage.

Los Banos Unified School District Superintendent Steve Tietjen, 55, is underwater on his home, too. He bought his Los Banos home in 2007. If a job change appears, “I'll have a dilemma,” he says. “I never would've conceived that somebody who's a superintendent would have that dilemma.”

Like Tietjen, many people here know someone who lost their house — either because of a job loss or a decision not to stick it out. Some former homeowners now rent. Some bought other homes at distressed prices, then walked away from underwater ones.

Buy-and-bail was a lot more common in the last housing bust. Lenders caught on early, and since 2007, most borrowers have been required to demonstrate the ability to make both house payments. That requirement prevented most buy-and-bail problems.

John Betham, 58, and his wife, Sandra, 55, are staying put. They owe $375,000 on their Los Banos home. They estimate it would sell now for $150,000.

The Bethams both teach in Los Banos. They can make the house payments and will delay their retirements if needed. They love their house and feel an obligation to pay the debt. “A lot of these people bailed. But we did everything right, and we're stuck,” John says. “It's a bit of a bitter pill.”

Not much relief in sight

Little relief is expected anytime soon here, despite signs of a strengthening U.S. economy.

Nationwide, home prices are down 30% from their 2006 peak. Moody's Analytics economist Celia Chen says national home prices will regain that ground by 2021.

Some areas will take far longer. In 22 U.S. metropolitan regions, most in California and Florida, home prices won't return to their 2006 peaks before 2030, Chen estimates. That includes such cities as Miami, Detroit, Phoenix, Las Vegas and Riverside, Calif.

Merced is so far off its peak that it'll take “many decades” for home prices to return to their 2006 peaks, Chen says.

People will have forgotten about the peak in these markets long before prices ever get there.

Like other central California communities, Merced's housing boom was fueled by San Francisco Bay Area commuters looking for cheaper housing. The opening of a University of California campus in Merced in 2005 attracted builders and investors who saw a big future for rentals.

In 2005, almost 3,500 single-family-home building permits were issued in Merced County, Moody's data show. That was up from an average of 1,053 a year in the 1990s. Merced's unemployment rate dropped below 10% in 2006 as home construction soared.

But Merced's fall was just as steep. Since 2006, the county has lost more than 2,500 construction jobs, state employment data indicate. In the past three years, just 415 single-family building permits have been issued countywide. Last year, one of 14 Merced homes received foreclosure filings vs. one of 45 nationwide, says researcher RealtyTrac.

Newcomers to Merced are winning in the hard-times economy. Home prices are so low that sales are made “as fast as we can stick a (for sale) sign in the ground,” says Loren Gonella, owner of Gonella Realty in Merced. In December, median prices were up 5% from a year ago, he adds.

He says home prices will recover. The UC campus is expanding, as is a relatively new hospital. Wal-Mart plans to open a distribution center here in the next few years, which would eventually employ up to 900. The San Francisco Bay Area has funneled home buyers to the Central Valley for decades. That will continue, he says.

The feared mass exodus from the county has not occurred. In Los Banos, student enrollment dipped in 2008 and 2009 but has returned to 2006 levels, Tietjen says. In many cases, multiple families inhabit homes that used to contain one, he says.

Ray Ortiz, 40, bought his Los Banos home in 2009 for $150,000. At the peak, it would have cost more than $400,000.

Ortiz commutes 90 minutes to his job in San Jose as a maintenance supervisor for a garbage company. He pays $50 more a month to own in Los Banos than he would to rent in San Jose.

Even if home prices drop more before they go up, Ortiz is confident he made a good buy.

“I feel like I won the lottery,” he says.

Buyers feel that way because they still believe prices will skyrocket and they will make a fortune. Kool aid will never die.

What was the bank doing for the last two years?

Today's featured property is the best example of seasoned shadow inventory I have found to date. This property has been bank owned since April of 2008. The owner, a buyer from 1991, managed to HELOC himself into oblivion with a $378,000 first mortgage in 2004.

The Notice of Default was issued on 12/5/2007, but it is safe to assume the loan was delinqent long before then.

I don't know if this has been empty or occupied. I presume it has sat empty as lenders continue to withhold inventory like this from the market.

When will the rest of this inventory be released? How the lending cartel releases its shadow inventory will determine the housing market's fate.

Irvine Home Address … 263 HUNTINGTON Irvine, CA 92620 ![]()

Resale Home Price … $300,000

Home Purchase Price … $410,666

Home Purchase Date …. 4/8/2008

Net Gain (Loss) ………. $(128,666)

Percent Change ………. -31.3%

Annual Appreciation … -10.7%

Cost of Ownership

————————————————-

$300,000 ………. Asking Price

$10,500 ………. 3.5% Down FHA Financing

4.99% …………… Mortgage Interest Rate

$289,500 ………. 30-Year Mortgage

$62,047 ………. Income Requirement

$1,552 ………. Monthly Mortgage Payment

$260 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$50 ………. Homeowners Insurance

$250 ………. Homeowners Association Fees

============================================

$2,112 ………. Monthly Cash Outlays

-$146 ………. Tax Savings (% of Interest and Property Tax)

-$348 ………. Equity Hidden in Payment

$20 ………. Lost Income to Down Payment (net of taxes)

$38 ………. Maintenance and Replacement Reserves

============================================

$1,675 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$3,000 ………. Furnishing and Move In @1%

$3,000 ………. Closing Costs @1%

$2,895 ………… Interest Points @1% of Loan

$10,500 ………. Down Payment

============================================

$19,395 ………. Total Cash Costs

$25,600 ………… Emergency Cash Reserves

============================================

$44,995 ………. Total Savings Needed

Property Details for 263 HUNTINGTON Irvine, CA 92620

——————————————————————————

Beds: 2

Baths: 3

Sq. Ft.: 1058

$284/SF

Lot Size: –

Property Type: Residential, Condominium, Townhouse

Style: Two Level, Traditional

Year Built: 1986

Community: Northwood

County: Orange

MLS#: P767933

Source: SoCalMLS

Status: ActiveThis listing is for sale and the sellers are accepting offers.

On Redfin: 9 days

——————————————————————————

Northwood's Horizon premium interior location, close to pool and amenities, no one above or below. Dual master bedrooms, over 1,000 square feet, and bonus half bath down stairs. Must see! Irvine Unified School District, Close to Parks, Shopping, Irvine Spectrum, Tustin Market Place and much more. Easy Freeway access: 5, 405, 133, Toll Road 73, 44, 57 and 22. Turn-key condition , submit offer today!

Oh the hardship of eating a TV Dinner at your desk instead of a fresh sandwich at a deli. I just about broke into tears after reading that and then remembered how you can make a fresh sandwich at your house for about the cost of a TV Dinner.

I am not understanding the milk in the coffee rather than cream. You can buy the generic cream for not much more than milk.

It sounds like these people just need to learn how to grocery shop.

Haha, I had the very same thoughts. I guess the next step’ll be black coffee (generic store brand only) 🙁 Poor lady

home depot and some banks (chase) have free coffee, free sugar, free powdered creamer. I don’t even bank there and stop by for a free cup now and then.

The coffee at chase belongs to any tax paying citizen anyhow.

when people perceive themselves as rich (relatively), resourcefulness goes out the window. The opposite is also true.

LOL. Brilliant!

This is, sadly, what we now refer to as “making big sacrifices” or “struggling to get by”. In the OC, it is driving a 4 year old Mercedes or lowering the pool/jacuzzi temp 1 degree. Our parents generation should be slapping us upside the head – They understood struggle. People during the depression waiting in lines for food, etc. It really makes us look pathetic and materialistic. What if..gasp… someone actually could no longer afford that 4th plasma TV or worse yet, what if they had to drop their HBO subscription. AAAAAgh, won’t somebody save us?

remember, this is a long way from over. the long overdue decline in standard of living will surface thanks to the magnitude of the RE bubble and resulting fiscal and monetary policy.

I dunno. I think the overall standard of living dropped very little during the recent recession, after climbing for a long time. There are statistical ways to measure this (square footage of housing space per person would be one input, for example).

The standard dropped very little because subsidy has delayed correction.

Mortgage brokers, realtors, construction industry workers have seen very little decline in standard of living? Most would find that hard to believe regardless of statistics.

In areas like Merced healthy banks would be better off doing cram downs on everyone. These areas were hyper inflated, and that money flew over east bay into the wallets in SF and other wealthy markets.

Areas like Merced are screwed. Banks would be smart to write off their losses and convert the debt into government backed debt providing the home owners equity to do so. Merced is never coming back. I can only assume banks are not healthy enough to do so. Extend and pretend makes sense in some markets. In areas like Merced it only makes sense if the bank can not eat the balance sheet losses.

Merced is the armpit of California. And I love how a state union worker is complaining about having to cut back on cream and sandwiches while the county tries to approve tax increases from the sheeple to pay for all the public sector pigs. I’ll shed a tear for these folks when hell freezes over. LOL

No doubt.

Every time I hear one of the stories about people supposedly “cutting back” and crying about having to give up Starbucks, dinners out 2-3x a week, and the like, I look at the picture above of the couple sitting on the couch.

I could just imagine trying to talk sense into them back in 2005. Dopey husband would just sit there drooling with the same glazed over look and the ever smiling wife would look at you with her big ass grin, nod her head and when you were done, she’d say…

“You know what? Let’s bake some cookies! Yeah…cookies!”

Since my parents’ county is in despair, I thought I’d check the online foreclosure auctions. Saw one, googled address. Local blockshopper site shows sales from AD -> WI, then WI -> EM, EM -> AI (AI & WI have the same last name, assuming relation), AI -> WI. WI’s final purchase was $150k or about 50% above his initial purchase. The last sale was 90% financed. I don’t want to throw mortgage fraud accusations out in these comments, but it smells fishy to me. And it was the first property I googled!

One NYTimes article I saw had mortgage fraud hotspots, and my parents’ county was one of them. Aside from everything else, fraud was widespread & for the most part ignored. Not enough people are going to jail, from the non-arms-length transactions to the lying securities packers at Bear Stearns.

I think if you listed the top 20 counties for mortgage fraud, they’d be the same as the 20 counties in despair.

This type of property is very unusual. It is extremely atypical for a bank to own a foreclosed property for two and a half years without selling it. This was actually shadow inventory, as opposed to the much more common “shadow shadow inventory” of the bank just taking forever to foreclose. I wonder if there was a lawsuit involved or some other reason that delayed the sale.

Wow! 50.5% of homes in Riverside County had underwater mortgage? Looks like prices in Riverside have a long ways to go, … on the downside.

Basically anybody who purchased or refied between 2003 and 2007 or so in Riverside County is underwater today (unless they put down a huge downpayment). I can easily believe that 50.5% of those houses that have mortgages (IE, excluding those who own their house free and clear) in Riverside County fall into that category.

I guess you can believe whatever you want, including the tooth fairy, but they appear to have data that says 50.5% of ALL homes in Riverside are underwater.

I wonder what has more credibility, Core Logic data or Geotph’s beliefs?

I believe the heading of the chart was as follows:

At least half of homeowners with a mortgage owe more than their homes are worth in 17 of 386 U.S. counties. Counties with the highest percentage of mortgages under water as of Sept. 30.

I also believe you didn’t bother to read this.

Speaking of despair, I’ve been wondering how this 500+ days of squatting is affecting property tax revenues. I’ve been searching for info on how much the California budget is getting hit by non-payment. Anyone know?

“Ortiz commutes 90 minutes to his job in San Jose as a maintenance supervisor for a garbage company. He pays $50 more a month to own in Los Banos than he would to rent in San Jose….I feel like I won the lottery,”

Wow…seriously, the stupidity of people never ceases to amaze me. One bad decision begets another and then another until a person is no longer capable of making any good decision. Do people HAVE to own so badly that they would willingly subject themselves to commuting 15Hrs/week? Apparently, yes.

I doubt those are comparable properties. Owning a 2000 sqft detached home vs. 750 sqft apartment does feel different.

The guy is probably spending 10% of his income on gas alone. These super long-distance commutes usually don’t end well.

You’re probably right. It is 80 miles from San Jose to Los Banos. That’s 160 miles a day. Assuming 20 miles per gallon, that’s 8 gallons a day. Assuming gas averages $3.75 a gallon for the foreseeable future, that’s $30 a day spent just on gas. There are roughly 20 working days a month so he’s looking at $600 a month spent on commuting.

This doesn’t include depreciation on his car and doesn’t include his time.

If you figure he makes $10 an hour and spends 3 hours commuting, that’s 30 dollars a day. 20 working days a month mean that he’s spending $600 of his time commuting a month.

Add in the depreciation on the car of another $100 or $200 a month, you’re looking at $1300-1400 a month spent on commuting costs alone.

So his savings of $50 on his mortgage/insurance over rent costs him around $1300 a month so he’s costing himself more than $1000 in opportunity costs and expenses.

That’s a bad deal. Where have we seen this before? Oooooh right – it went something like this: “You want to borrow as much as you can to maximize your tax deduction!!”

Morons. Every last one of them.

Forget power lines…nothing can persuade me to live in a town called “The Bathrooms”.

some people’s time isn’t worth anything which is why they can commute 15 hours/week.

Boy! I better not let my wife and kids read this blog. They might think our normal life is improvied. We eat out less, have less TV, less cars, older cars, than they do.

Who needs a South Beach Diet Bar when oakmeal and nuts are cheaper and healthier alternatives.

The percentage of housing under water only tells part of the story. It’s the percentage under water that really counts. The likelyhood of a walk away with 100% of the houses 3% under water is lower than the 1% of the house that are 99% under water. Just buying a house makes most buyers 8% under water.

IR:

Lansner on RE has an article up re Peggy Tanous of Irvine, one of the Real Housewives of OC.

Apparently “her” house is in Default and it appears she’s been squatting since 2008.

Would you be able to do an analysis for us on this particular property?

http://lansner.ocregister.com/2011/02/08/newest-housewife-defaults-on-irvine-home-loan/98648

Pic of Irvine house:

http://stoopidhousewives.com/2011/02/08/real-housewives-of-orange-county-under-water

~Misstrial

It looks like a Columbus Grove house.

:hides from AZDave’s ForTheChildren trolling:

Did someone say “the children“?!

Oh another OC pretender? Pray tell!

IR & Zovall – What do you call that “Submit the word you see below:” prompt? I wanna see if I can put on of those on the comments section of my blog, but I do not know what to look up.

Captcha:

http://en.wikipedia.org/wiki/CAPTCHA

Yup, it is a CAPTCHA. There should be some good WordPress plugins for it. Another WordPress plugin that works great to help reduce spam is ‘Akismet’

Can you explain why people complain so much that their homes are underwater, they earn less, etc?

They signed a contract which clearly indicates how much money they would pay each month for the next 30 years, rain or shine. So, they could afford to pay.

My understanding of the house buying process:

* You buy a $700,000 house today.

* You must set aside at least $4,000 for the monthly payments, taxes, repairs, etc

* You must keep in bank $50,000 (12 * $4,000), so you’ll be able to survive and pay for the house for a year or more if you lose your job.

You nailed it.

These people clearly thought it was a fair deal back when they bought the house and indebted themselves for 30 years.

So the house has now lost half its value. So what? What does that have to do with what you bought it for? Where was your ability to afford the house dependent on the current market value of the house? You paid the premium to be a house owner at a time when many others had to go rent because they could not afford it. Isn’t that worth something?

It’s not like many of these folks would have changed their minds had someone tried to talk them out of buying.

It is odd that somehow the perceived value of a house goes down when the market value goes down. It’s almost as if people were buying homes during the 00s purely to capture the magic appreciation.

No matter what you said, you couldn’t talk them out of it. If you showed them it was a bad deal using math, they would call you a bitter renter. If you told them they won’t keep going up, they would say something like “something is worth whatever someone will pay for it” (never mind the fact that, in the aggregate, people _weren’t_ paying for houses they were borrowing. What they should have been saying is that something is worth whatever someone can borrow for it.)

No matter. Here we are half a decade later and people are finally waking up to the fact that home ownership costs money. The people locked into these homes will be nickel and dimed for the rest of their lives and stand little chance at accumulating any sort of net worth. Their only chance is bankruptcy and then rebuilding but the powers that be are fooling them into thinking that staying in the house is the best course of action for them. In this way, the banks will take all that they earn.

So, what’s the moral of the story? Rent, don’t buy and watch the great unwashed masses (yes this is you, Irvine) eat shit because of their past bad decisions.

>The people locked into these homes will be nickel and dimed for the rest of their lives and stand little chance at accumulating any sort of net worth.

In 30 years, their houses will be worth much more than now. So, if they keep paying, they will eventually accumulate some wealth.

Mr. James Irvine was able to buy the whole Irvine area for $25,000, it was only 150 years ago.

Thank you for proving my point, Vincenzo. It is no wonder people like yourself are so easily manipulated.

These houses will not be ‘worth more.’ They will deteriorate as time passes and become worth less. This decrease in value will be compounded by a declining population. However, the absolute value of the dollar amount attached to them will be greater, but they will not be more valuable in nominal terms. In all likelihood, they will not return to the nominal value witnessed in the past decade ever in our lifetimes.

By your logic, its only a matter of time before tulip bulbs are as valuable as they were at the peak of tulipmania. How likely do you believe that to be? I’ll remind you that at the height of tulip mania, tulip bulbs were selling for roughly 10-15 times what a skilled craftsman made at the time. In today’s dollars that’s a single bulb for around $750k. Seem like a likely scenario to you? It is about as likely as home prices coming back to the same nominal value.

I don’t argue about it.

House prices will certainly go up if measured in green bills.

House prices will decline if measured in hours “you have to spend in office listening to your grumpy boss”.

I wish people measured value this way. Unfortunately people just think “its only $xx which I can put on my credit card and worry about it later.”

I like to put the value on something I buy in the same line as “how many hours a day did I have to work (relative meaning) to pay for this.” And that determines how badly I want that item. If I NEED that item, I just bitch and moan about having to pay for it, but if I NEED it, it does not matter the cost (medicine, car maintenance, etc).

There is no almost about it. In bubble areas, during the period from 05-07, people bought because of appreciation. If you didn’t believe the appreciation story (there were more than just IR), you rented. IR, I know others in FL who took a similar tack to you and are still renting.

The ‘budget shortfall’ could be construed as the additional amount needed to pay for public workers’ retirement plans, perks, etc.

http://www.pensiontsunami.com/