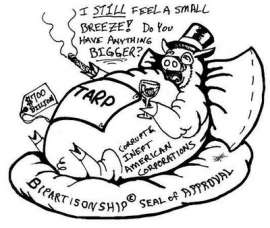

In what is erroneously being reported as a paid settlement, banks are offering to reduce mortgage principal if it helps them settle the lawsuits filed by attorneys general in all 50 states.

Irvine Home Address … 28 BUTTERFIELD 14 Irvine, CA 92604

Resale Home Price …… $390,000

The midnight rain follows the train

We all wear the same thorny crown

Soul to soul, our shadows roll

And I'll be with you when the deal goes down

Bob Dylan — When the Deal Goes Down

Attorneys general everywhere are trying to make a deal that makes them look good, allows banks to recognize losses on their hopeless loans, and provides additional false hope that keeps distressed borrowers hanging on.

U.S. Pushes Mortgage Deal

Obama Proposal Seeks Multibillion-Dollar Settlement of Loan-Servicing Cases

FEBRUARY 24, 2011 — By NICK TIMIRAOS, DAN FITZPATRICK and RUTH SIMON

The Obama administration is trying to push through a settlement over mortgage-servicing breakdowns that could force America's largest banks to pay for reductions in loan principal worth billions of dollars.

When they use the word “pay” it sounds like they are talking about real money being transferred between parties, but that isn't what's happening.

Terms of the administration's proposal include a commitment from mortgage servicers to reduce the loan balances of troubled borrowers who owe more than their homes are worth, people familiar with the matter said. The cost of those writedowns won't be borne by investors who purchased mortgage-backed securities, these people said.

If a unified settlement can be reached, some state attorneys general and federal agencies are pushing for banks to pay more than $20 billion in civil fines or to fund a comparable amount of loan modifications for distressed borrowers, these people said.

So the banks can pay real money, or they can write down their worthless securities they are holding on their books at face value — something that happens anyway when the borrower strategically defaults and the property goes through foreclosure.

The banks aren't being asked to part with anything of value. They have an illusion on their books that they are revealing as illusion. Whereas previously everyone agreed to pretend these loans were going to be repaid and the banks would recover their capital, now everyone is agreeing to see what is apparent. Banks will mark a few loans to market. In exchange for giving up billions in illusory assets, the banks get various lawsuits dismissed — the ones started by pandering attorneys general around the country to appease delinquent loan owners.

In the end we have a large and largely bogus robo-signer scandal being wrapped up and put out with the trash accompanying a few severely underwater loan owners who were going to default anyway.

But the banks gain something much more. The remaining loan owners who are not going to see any principal reductions — meaning 99.9% of them — are going to cling to the false hope of a principal reduction windfall to keep them making those oversized payments.

All government bailout programs are a deception. The only purpose of these programs is to find stealth methods of funning money to banks or protecting banks assets. If a few loan owners benefit in the governments efforts to prop up our banks, it is an incidental byproduct of the government's real purpose which was to give money to banks. By bailing out a few hapless home debtors, lenders can dangle the principal reduction carrot in front of the masses. The masses will dutifully comply in hopes of getting that big payout. Its this same psychology that makes keeps people gambling or playing the lottery.

But forging a comprehensive settlement may be difficult. A deal would have to win approval from federal regulators and state attorneys general, as well as some of the nation's largest mortgage servicers, including Bank of America Corp., Wells Fargo & Co, and J.P. Morgan Chase & Co. Those banks declined to comment.

A settlement could help lift a cloud of uncertainty that has stalled the foreclosure process since last fall. Economists have warned that foreclosures need to proceed for the housing market to continue on a path to recovery. It's unclear how many borrowers would benefit from a deal. Servicers have thus far had difficulty managing the volume of troubled loans.

It is very clear that far fewer will actually benefit than the total number that needs debt reduction.

So far, most loan modifications have focused on shrinking monthly payments by lowering interest rates and extending loan terms. Banks, as well as mortgage giants Fannie Mae and Freddie Mac, have been shy to embrace principal reductions, in part due to concerns that many borrowers who can afford their loans will stop paying in the hope of being rewarded with a smaller loan. But some economists warn that rising numbers of underwater borrowers will drag on housing markets and the economy for years unless more is done to help them.

The settlement terms remain fluid, people familiar with the matter cautioned, and haven't been presented to banks. Exact dollar amounts haven't been agreed on by U.S. regulators and state attorneys general. Regulators are looking at up to 14 servicers that could be a party to the settlement.

These servicers are motivated to get these lawsuits off their backs.

The deal wouldn't create any new government programs to reduce principal. Instead, it would allow banks to devise their own modifications or use existing government programs, people familiar with the matter said.

At least the banks are not directly transferring these losses to the US taxpayer.

Banks would also have to reduce second-lien mortgages when first mortgages are modified.

Does this apply to purchase money mortgages only? Are we giving all the HELOC abusers a pass?

Several federal agencies have been scrutinizing the nation's largest banks over breakdowns in foreclosure procedures that erupted last fall. Last week, the Office of the Comptroller of the Currency said only a small number of borrowers had been improperly foreclosed upon. But the regulator raised concerns over inadequate staffing and weak controls over certain foreclosure processes.

A settlement must satisfy an unwieldy mix of authorities, including state attorneys general and regulators such as the newly formed Bureau of Consumer Financial Protection, who support heftier fines. They must also appease banking regulators, such as the OCC, that are concerned penalties could be too stiff.

Regulators are concerned penalties could be too stiff? We wouldn't want banks to be penalized for their bad behavior, right?.png)

“Nothing has been finalized among the states, and it's our understanding that the federal agencies we are in discussions with have not finalized their positions,” said a spokesman for Iowa Attorney General Tom Miller, who is spearheading a 50-state investigation of mortgage-servicing practices.

Last autumn, units of the nation's largest banks were forced to suspend foreclosures amid allegations that bank employees routinely signed off on foreclosure documents without personally reviewing case details. In subsequent examinations, federal bank regulators said they found deficiencies and shortcomings in document procedures and other violations of state law.

At issue now is a debate over who has been harmed by improper foreclosure practices, and how much. The OCC's examination concluded only a “small number” of borrowers were improperly foreclosed upon, and banks have argued that any settlement should reflect that fact. Other federal agencies and state officials say banks exacerbated the woes of troubled borrowers by resisting the necessary investments in staff and technology to provide timely, effective help.

On this issue, the banks are right. The charges of improper foreclosure are mostly bullshit being used by political operatives to stoke populist fires. The actual number of improperly foreclosed properties is very small, particularly considering the millions of properties going through foreclosure.

Under the administration's proposed settlement, banks would have to bear the cost of all writedowns rather than passing them on to other investors. The settlement proposal focuses on pushing servicers who mishandled foreclosure procedures to eat losses, by writing down loans that they service on behalf of clients. Those clients include mortgage-finance giants Fannie Mae and Freddie Mac, as well as investors in loans that were securitized by Wall Street firms.

Bank executives say principal cuts don't necessarily improve payment patterns, and have told other parties involved in the talks that principal reductions could raise new complications. First, it will be difficult to determine who gets reductions and who doesn't. And even if banks agree to a $20 billion penalty, the number of mortgages that can be cured with that number is limited, one of these people said.

Let's ponder that one for a minute. Let's say you see your spendthrift neighbors HELOC their house, buy all the toys, take trips, and generally live a Ponzi. After pissing away several hundred thousand dollars, your neighbors are having a hard time paying their bloated mortgage. They apply for principal reduction and get it. They quickly start the Ponzi scheme all over again.

On the other hand, you have worked hard, saved your money and paid down your mortgage while the Ponzis were being Ponzis. Let's say you work in a real estate related field, and your income is down and you're having trouble making payments. Is the bank going to reduce your principal?

No way.

You have equity. Why would they simply give you more equity? You see, the first criteria for getting a principal reduction will be the need to be in a negative equity position. That eliminates most of the people worthy of debt relief and targets the benefit the most egregious Ponzi spenders and the most foolishly leveraged peak buyers. Indirectly through government bailouts and principal reductions, money was taken from your household and transferred to the Ponzis.

If a single settlement can't be reached, different federal agencies could seek smaller penalties through regular enforcement channels, and banks could face the prospect of separate civil actions from state attorneys general.

Any settlement could be one of the largest to hit the mortgage industry. In 2008, Bank of America agreed to a settlement valued at more than $8.6 billion related to alleged predatory lending practices by Countrywide Finance Corp., which it acquired that year.

—Robin Sidel contributed to this article.

Write to Nick Timiraos at nick.timiraos@wsj.com, Dan Fitzpatrick at dan.fitzpatrick@wsj.com and Ruth Simon at ruth.simon@wsj.com

The attorneys general will spin this moral hazard laden garbage as a victory for the people. What people?

Lenders will selectively reduce principal on a few deeply underwater borrowers in hopes they won't default anyway. It seems to me that lenders get the better end of that deal, and they can try to dodge the moral hazard issue by saying the government made us do it.

The Irvine HELOC abuse lifestyle

When i looked through the mortgage records for today's featured property, I saw the same pattern of living off home equity. These people were renters who were paid to stay in their apartment for several years. Now that they are leaving, their credit is trashed, but its a small price to pay to live free for several years.

- Today's featured property was purchased for $350,000 on 5/6/2003. The owners used a $280,000 first mortgage, a $70,000 second mortgage, and a $0 down payment.

- On 6/3/2004 they extracted their first $10,000 by refinancing with a $360,000 first mortgage.

- On 7/9/2004 they opened a $50,000 HELOC.

- On 7/21/2005 the revisited the ATM with a $75,000 HELOC.

- On 12/19/2006 they obtained a $118,298 HELOC.

- Total property debt is $478,298.

- Total mortgage equity withdrawal is $128,298.

- They haven't made a payment since 2009.

Foreclosure Record

Recording Date: 02/26/2010

Document Type: Notice of Default

A generation learned during the 00s they could live with essentially no housing cost, and in good years, the house actually paid them to live in it. Why would anyone rent?

This is the surreal life of California real estate. And endless cycle of boom and bust that creates dependency and sloth.

Today's owners put nothing down and extracted $120K in three years. Do you want to forgive their principal so they can do it again?

Irvine Home Address … 28 BUTTERFIELD 14 Irvine, CA 92604 ![]()

Resale Home Price … $390,000

Home Purchase Price … $350,000

Home Purchase Date …. 5/6/03

Net Gain (Loss) ………. $16,600

Percent Change ………. 4.7%

Annual Appreciation … 1.4%

Cost of Ownership

————————————————-

$390,000 ………. Asking Price

$13,650 ………. 3.5% Down FHA Financing

4.86% …………… Mortgage Interest Rate

$376,350 ………. 30-Year Mortgage

$79,471 ………. Income Requirement

$1,988 ………. Monthly Mortgage Payment

$338 ………. Property Tax

$0 ………. Special Taxes and Levies (Mello Roos)

$65 ………. Homeowners Insurance

$300 ………. Homeowners Association Fees

============================================

$2,691 ………. Monthly Cash Outlays

-$326 ………. Tax Savings (% of Interest and Property Tax)

-$464 ………. Equity Hidden in Payment

$25 ………. Lost Income to Down Payment (net of taxes)

$49 ………. Maintenance and Replacement Reserves

============================================

$1,976 ………. Monthly Cost of Ownership

Cash Acquisition Demands

——————————————————————————

$3,900 ………. Furnishing and Move In @1%

$3,900 ………. Closing Costs @1%

$3,764 ………… Interest Points @1% of Loan

$13,650 ………. Down Payment

============================================

$25,214 ………. Total Cash Costs

$30,200 ………… Emergency Cash Reserves

============================================

$55,414 ………. Total Savings Needed

Property Details for 28 BUTTERFIELD 14 Irvine, CA 92604

——————————————————————————

Beds: 3

Baths: 2

Sq. Ft.: 1460

$267/SF

Lot Size: –

Property Type: Residential, Condominium, Townhouse

Style: Two Level

Year Built: 1974

Community: El Camino Real

County: Orange

MLS#: P762360

Source: SoCalMLS

Status: ActiveThis listing is for sale and the sellers are accepting offers.

On Redfin: 81 days

——————————————————————————

Cozy townhome in Irvine. Desirable community, close to shopping, parks & accessible freeways. Needs a little touch of tlc to make this Home yours. .. .. .. .. .. .. .. .. .. . come see!

I would not get to bent out of shape over the prospect of these “principal reductions” as it almost 100% guaranteed that it is just another Red herring. I would imagine these ruthless bankers will make sure that the rules are so hard to comply with that virtually nobody will qualify. Most likely they will set the forgiveness date to something far off into the future like 5 or 10 years and part of the deal will be that they struggling house debtors immediately catch up on their mortgage and keep it current the whole time. This will lure back in some of the strategic defaulters who can still afford to pay while making sure that those who do not have the means get no help whatsoever. There will be plenty of opportunity to get the others to trip up over the next few years and void the agreement. That’s how these guys work – I have no doubt the devil will be in the details on this one.

Total red herring.

It’ll be a setup to turn California Non-Recourse high $ purchase loans into debt slavery recourse loans.

Mish already crunched the numbers.

http://globaleconomicanalysis.blogspot.com/2011/02/obama-seeks-20-billion-in-civil-fines.html

Looks like approximately $4,000 per debtor and that doesn’t include the people who haven’t received NOD’s yet haven’t made a payment in years.

BTW…did you see Calculated Risk shilling for the NAR?

62% of homes over $5,000,000 purchased in January were CASH purchases. Definitely something for PlanetRealty and TinMagnet to stroke themselves over.

Too bad there were only about 15 (or less) homes that month…out of over 800 listed.

Speaking of tenmagnet — ten, did you see this?

http://www.redfin.com/CA/Irvine/24-Vernal-Spg-92603/home/5899655

Shady Canyon breaks below $2M. Check out that July 2006 sales price.

Shady Canyon. Not immune.

Nice find and good to see you post again.

The listing looks legit.

A few weeks back, I ripped Lee in Irvine when he made his apocalypse now prediction for Shady Canyon.

We’ll see if it’s real or some low-ball tactic disguised to spark a bidding war.

That’s a property profile in the IHB’s future. Thanks.

24 Vernal Springs went pending.

No matter what form these “principal reductions” take, they won’t ammount to a hill of beans. What’s really needed is bankruptcy cram-down of primary residence mortgages.

While some may think this is a giveaway to “bad” debtors, actually it helps preserve real estate values for everyone. It costs banks real money to evict a debtor, fix a property and to sell the property. When the property is sold, the bank only gets the present value of the property. However, the bank is also out all of the costs. Furthermore, bank forslosures flood the market and destroy home values.

If the mortgage holder could get his or her principle reduced to the present value of the property via bankruptcy cramdown, the bank does not have to pay the costs associated with eviction and resale. The local propety market does not take a huge hit caused by a flood of REO properties on the market. And the homeowner is able to keep the property if they can afford to pay a mortgage based upon the present value of the property.

Everyone wins. Bankruptcy cramdown happens with every other secured loan, including mortgages on jets, vacation homes, and yachts. The reason it is not allowed on primary residences is to scew over homeowners and favor banks. The prohibition against primary mortgage cramdown has to go.

“…Let’s say you see your spendthrift neighbors HELOC their house, buy all the toys, take trips, and generally live a Ponzi…”

Your spendthrift neighbors can already do this through bankruptcy. It’s a little more difficult if they’re higher-earners, but still the same concept.

Also, I will indirectly benefit from loan modifications and principal reductions on my spendthrift neighbors’ homes because that’s one less house on the market in my neighborhood. If it holds-up the value of my home a bit, that might make refinancing for me (the non-spendthrifter) easier.

I’m not advocating for principal reductions – just sharing the idea that they can benefit more than just the spendthrift deadbeat…

“I will indirectly benefit from loan modifications and principal reductions on my spendthrift neighbors’ homes because that’s one less house on the market in my neighborhood. If it holds-up the value of my home a bit, that might make refinancing for me (the non-spendthrifter) easier.”

The benefit you describe works against a renter or prospective home buyer who must pay a higher price.

The housing bubble has created a form of class warfare between homeowners trying to preserve values and buyers trying to get as good a deal as homeowners got years ago.

Exactly right. And with 60-something percent of the population claiming the title of “homeowner” – it absolutely no surprise which group is making most of the noise and demanding that the Government and banks “do something”.

I am still not hearing of any renters demanding government programs to help subsidize rental expenses. Homeowners should recognize the societal benefits to renters having a roof over their heads which produces low levels of homelessness, crime, etc.

While not drastically overstated, 60%+ sounds too high. I read that the highest the homeownership rate got during the housing bubble was 57%, and I’ve read more recent articles saying that that rate has fallen as low as 52%. So, we’re about evenly split between homeowners and renters now.

Of course, homeowners as a group do tend to have higher personal net wealth and vote more consistently, so it’s still no question who the politicians are going to favor.

-Darth

52% sounds way low to me. I was going off of the Wikipedia:

http://en.wikipedia.org/wiki/Homeownership_in_the_United_States

The homeownership rate in the United States[1][2] in 2009 remained similar to that in other post-industrial nations[3] with 67.4% of all occupied housing units being occupied by the unit’s owner.

I can’t seem to find the articles that I read before, and the official stats all agree with you. Guess I was wrong. In any case, no matter the rate, homeowners will always have more political power, due to higher incomes and more consistent voting patterns.

-Darth

I think Darth’s numbers may be CA specific

Here’s a real life example. One of my clients in escrow now has a couple of other properties. Two of the homes were financed with WAMU loan products. What stands out is that these clients are NOT upside down. They are NOT behind on their payments. They are NOT in a distressed position.

On one loan Chase is offering to turn their ARM loan in the low 3’s into a 30 fixed loan at 4.0%. No fees, no application, no appraisal, no underwriting. Sign here, and you’ve got a 4.0% rate. Based on the property type and other factors, a new Chase retail loan would come in at about 5.75%. This refinance is being called in the documentation a “Loan Modification”. Remember this was unsolicited by my client. On a second property Chase suggested if the borrower paid off their 2nd TD, Chase would “forgive” a bit over $20,000. Did Chase suddenly have a “Grinch Moment” listening to all the little Who’s in Whoville and decide with their hearts growing two sizes too big and start writing below market loans and forgiving principal?

No. Since these are called “modified loans” (for AAA paper home owners) Chase now can claim another successful private modification made, perhaps to keep the Gubmint from coming after them for poor servicing and modification performance.

My financial recommendation for the next 6 months: Go long pitchforks and torches. Perhaps you’re rate / principal reduction will be granted.

Soylent Green Is People.

SGIP, your dose of reality is difficult for many here to swallow. Principal reductions and loan modifications can’t happen because they don’t want them to happen. I prefer the cold hard reality, hey it sucks it’s happening and will continue to happen. The lesson learned? Next time don’t forget to join the party.

Ahh for a DeLorean and a Flux Capacitor… We’d all lever up with 100% LTV Cash Out Option ARM’s, waiting for Uncle Sugar and the rest of the unwashed to take care of the mistakes we made.

Playing devil’s advocate, upping the rate from 3 to 4 does increase interest income, but absorbing the interest rate risk. JPM probably assumes that short term rates that set the ARM will stay low for a while.

As for the 20k to clear a 2nd, that may be an incentive to help reduce their overall exposure to 2nds in general. A good portion of the 2nds, especially in 80-20’s are worthless, so even though this 2nd is not, it is seen as though it were by investors/regulators.

Is the loan in escrow going to JPM too? I’d be pissed if I were JPM, helping this person, only to have them take other business elsewhere.

JPM wants to show how great their modification program is progressing, while at the same time flipping the loan to FNMA – a recourse loan now since it’s a refinance!

Don’t get me wrong. This is a great deal for the home owner. It’s just being presented as a help up for a borrower who didn’t ask for it while those really in need get the finger.

The loan in escrow is going through our company. We are not a broker. Besides, our rates are often better than Chase’s.

Except for the 4% sweetie they got. I doubt they’re just passing it to FNMA, as FNMA’s rates would have been > 4%. Maybe they are sacrificing their spread.

They may be looking for no-cost modifications to boost their numbers, but we should not be surprised. Asking a business like JPM to help out, when they are successful by crushing competition, and laying off large numbers of workers after acquisitions, and developing the most opaque ‘financial wmd’s’, is a bad idea. We should not be surprised when they are not as helpful as we want.

A friend of mine bought an $800K house with a $600K loan and made major improvements to the house. At one point (close to the peak, perhaps?) it was worth almost $2M and he had a very large line of credit for his business. Now the credit line is “due” and the bank wants all of the money back unless he signs a new, “bend over” line of credit because the house has dropped so much. They’re threatening to foreclose on him if he doesn’t pay or sign. So they’re modifying the people that they can’t squeeze, and they are going after the people with money with a vengeance.

Not sure I understand – A typical HELOC’s “line” could be reduced or eliminated, but that only means you won’t be able to draw on it again. Other than that, the HELOC agreement sets the adjustable rate and payment schedule. That can’t be changed due to the value of the security.

That actually happened to me a few years ago when Ditech pulled out of the HELOC market. They froze my line (I’d only used about 20% of it) and I just had to continue paying off my balance until it matured.

When I went to BofA to get a new line and pay off my Ditech line, BofA would only give it to me if I opened the same amount of HELOC. When I told them that I only needed 1/2 that amount “open”, they said they’d only approve the full amount. (!)

My friend has neared the end of his HELOC term, so the bank is negotiating the new terms for the new HELOC.

“So they’re modifying the people that they can’t squeeze, and they are going after the people with money with a vengeance.”

Just as I always suspected they would

I do not have a prediction on principle reductions, but …

I do know that the mortgage debt market can not clear without another 27% reduction in home prices in inflation adjusted dollars as time progresses. Whether that reduction is accomplished by increasing the money supply or whether is accomplished through principle reductions, I dunno, but it will happen.

High-profile agent’s headquarters in default

http://lansner.ocregister.com/2011/03/01/high-profile-agents-headquarters-in-default/101423/